Greenhouse Grower’s 2026 Top 100 survey asked growers three useful questions about technology. One asked what they want to learn more about and how it might fit into their operations. Another asked what technology they still believe needs to be developed for the industry. The third asked whether they are already using artificial intelligence (AI) systems in their greenhouses. The answers do not point to an industry chasing technology for the sake of looking modern. They point to growers trying to solve real operational problems and looking for tools that are practical enough to trust.

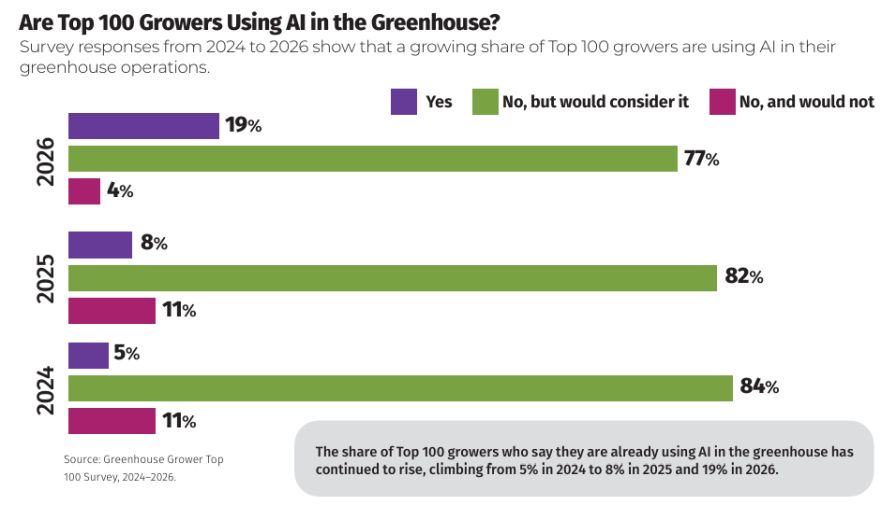

AI is the easiest place to start because it gives the clearest reading of where adoption stands right now. Only 19% of respondents said they are currently using AI in their greenhouse operations. More than three-quarters said they are not using AI but would consider it, while only 4% said they would not consider it. So, while growers may not be adopting AI at scale yet, most do not appear to be dismissing it outright.

That hesitation looks a lot less like resistance once the open-ended responses come into view. When growers were asked what kinds of technology they wanted to learn more about, AI and robotics showed up often, but they were hardly the only answers. Respondents also mentioned drones, automation, transplant technology, material handling, lighting, crop management tools, heating and controls, water treatment systems, scannable systems that could eliminate labor steps, and logistics or replenishment software. That is not the language of an industry mesmerized by one trend. It is the language of growers scanning for anything that they can do to save time, reduce labor friction, improve control, or tighten execution.

The survey shows that growers want help with the recurring pressure points inside a greenhouse operation. Labor is one of them. Workflow is another. So are environmental management, crop tracking, and the constant need for better information at the right time. Technology gets attention when it looks like it can make one of those jobs easier, faster, or more accurate.

Survey responses from 2024 to 2026 show that a growing share of Top 100 growers are using AI in their greenhouse operations.

When responding about what still needs to be developed, growers again mentioned AI, robotics, and automation, but they asked for better ERP systems and stronger software platforms. They mentioned environmental controls that can more effectively respond to weather, transpiration, and watering needs. They called out quality-control cameras, sorting technologies, harvesting automation for potted plants, GPS cart-moving equipment, predictive analytics, water-efficient irrigation systems, and robotics that can do more than one job well. That list shows where frustration is. In many cases, the issue is not a lack of ideas. It is a lack of tools that feel complete, connected, and durable enough for real production use.

That is a more useful takeaway than simply saying growers are interested in AI. Of course they are. So is everyone else. What stands out here is that growers are still asking basic questions about fit. Can the system handle greenhouse conditions? Can it reduce labor rather than add another layer of management? Can it connect to the software already in place? Can it solve more than one narrow task? Can it deliver enough value to justify the cost and learning curve? The survey responses keep coming back to those practical tests.

Among respondents investing in technology, the top reasons were improved efficiency at 80%, cost of labor at 72%, availability of labor at 49%, and better uniformity and efficacy of production at 47%. Those are not vanity reasons. They reflect daily operational pressure. They also explain why technological interest can be high even when adoption of newer tools remains limited. Growers are interested because the need is real. They are cautious because the wrong investment can create just as many problems as it solves.

Planned investment for 2026 points in the same direction. Production automation and planting equipment ranked highest at 54%, followed by irrigation equipment and controls at 52%, greenhouse structures and coverings at 48%, and computer software at 44%. Lighting came in at 36%, functional automation at 28%, and growing media equipment at 26%. Emerging technology, such as drones, UAVs, and AI, was much lower at 12%, with robotics at 16%. That spread says growers are still putting money first into systems that can improve output, labor efficiency, and environmental control now. The more experimental or less proven categories may be drawing attention, but they are not yet winning the same share of actual investment.

What the survey suggests is that curiosity is running ahead of adoption. Growers can see where AI, robotics, software, and automation might make a difference, but they also believe much of the market still needs work. The distance between “I want to learn more about this” and “I am using this now” is not just about cost or conservatism. In many cases, it is about confidence. The technology has to prove that it belongs in greenhouse production, not just in a demo, a pitch deck, or a trade show conversation.

What the survey suggests is that curiosity is running ahead of adoption. Growers can see where AI, robotics, software, and automation might make a difference, but they also believe much of the market still needs work. The distance between “I want to learn more about this” and “I am using this now” is not just about cost or conservatism. In many cases, it is about confidence. The technology has to prove that it belongs in greenhouse production, not just in a demo, a pitch deck, or a trade show conversation.