Europe has ‘maybe 6 weeks of jet fuel left,’ energy agency head warns

The head of the International Energy Agency has warned that Europe has about six weeks of jet fuel left.

In an interview with Associated Press published today, IEA executive director Fatih Birol warned that flight cancellations could begin “soon” if oil supplies remain blocked by the Iran war.

Birol said Europe has “maybe 6 weeks or so (of) jet fuel left,” after the effective closure of the strait of Hormuz led to “the largest energy crisis we have ever faced.”

He told AP that the impact will be “higher petrol (gasoline) prices, higher gas prices, high electricity prices,” adding that some parts of the world will be hit worse than others.

“The front line is the Asian countries” that rely on energy from the Middle East, he said, naming Japan, Korea, India, China, Pakistan and Bangladesh, adding:

“Then it will come to Europe and the Americas.”

And if the strait of Hormuz isn’t reopened, Birol said that for Europe:

“I can tell you soon we will hear the news that some of the flights from city A to city B might be canceled as a result of lack of jet fuel.”

The US is currently blockading Iranian ports, whiel Tehran has laid mines in the vital waterway to restrict traffic through the strait.

Yesterday, IMF chief Kristalina Georgieva warned that the disruption from the Middle East conflict would continue even after the war stops, explaining:

“We need to recognise disruptions are not going to evaporate overnight even if the war ends tomorrow. Why? Because a tanker is a slow-moving vessel. It would take 40 days to get all the way to Fiji.”

Key events

Here’s our news story on the IEA’s warning that Europe is running low on jet fuel:

The European Union is drafting plans to tackle a looming jet fuel supply crunch and maximise refinery output, officials have said.

From next month, the European Commission will introduce EU-wide mapping of refining capacity for oil products and introduce measures “to ensure that existing refining capacity is fully utilised and maintained”, a draft proposal seen by Reuters said.

Thomas Pugh, chief economist at audit, tax and consulting firm RSM UK, says:

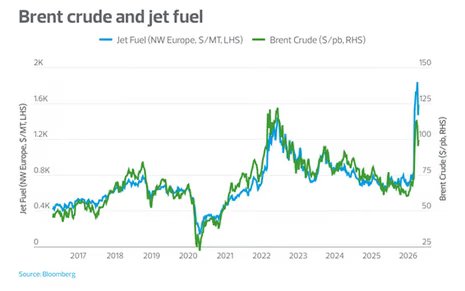

“Oil prices might have fallen back, but it’s refined product prices that matter for business and inflation. Jet fuel prices are still above their 2022 peaks and diesel prices aren’t far off.

“The last tanker of jet fuel to pass through the Strait of Hormuz docked in Europe on Saturday. The UK is importing more from the US, but not enough to fill the gap. With jet fuel prices close to record highs, it’s not surprising we are seeing airlines increase fuel surcharges, as well as smaller airlines cancelling routes and it won’t be long before larger ones follow suit, as they have in Asia. That’s demand destruction in action.

Jet fuel prices have already been rising sharply, hitting airlines’ profitability.

The budget airline easyJet warned this morning that the impact of the Iran war on bookings and oil prices will hit its profits, having driven up fuel costs by £25m in the last month alone.

It said it expected to report an increased pre-tax loss of £540-£560m for the six months to March, up from £394m in the first half of 2024-25. The carrier typically makes its money in the second half of the year which includes the peak summer period.

The airline said it remained confident in its fuel supply. While it has hedged 70% of its needs for the rest of the financial year to September, it said that each $100 (£74) movement in the spot price jet of fuel per metric tonne was adding £40m in costs for its unhedged supply – and currently the price is about $800 higher than before the conflict started.

More here:

Europe has ‘maybe 6 weeks of jet fuel left,’ energy agency head warns

The head of the International Energy Agency has warned that Europe has about six weeks of jet fuel left.

In an interview with Associated Press published today, IEA executive director Fatih Birol warned that flight cancellations could begin “soon” if oil supplies remain blocked by the Iran war.

Birol said Europe has “maybe 6 weeks or so (of) jet fuel left,” after the effective closure of the strait of Hormuz led to “the largest energy crisis we have ever faced.”

He told AP that the impact will be “higher petrol (gasoline) prices, higher gas prices, high electricity prices,” adding that some parts of the world will be hit worse than others.

“The front line is the Asian countries” that rely on energy from the Middle East, he said, naming Japan, Korea, India, China, Pakistan and Bangladesh, adding:

“Then it will come to Europe and the Americas.”

And if the strait of Hormuz isn’t reopened, Birol said that for Europe:

“I can tell you soon we will hear the news that some of the flights from city A to city B might be canceled as a result of lack of jet fuel.”

The US is currently blockading Iranian ports, whiel Tehran has laid mines in the vital waterway to restrict traffic through the strait.

Yesterday, IMF chief Kristalina Georgieva warned that the disruption from the Middle East conflict would continue even after the war stops, explaining:

“We need to recognise disruptions are not going to evaporate overnight even if the war ends tomorrow. Why? Because a tanker is a slow-moving vessel. It would take 40 days to get all the way to Fiji.”

Aluminium hits four-year high on Middle East supply worries

Ouch! Aluminium prices have hit a four-year high today, adding to the inflationary pressures on companies.

Benchmark three-month aluminium on the London Metal Exchange rose as high as $3,672 a metric ton this morning, its highest level since March 24, 2022.

Reuters reports that the global aluminium market is facing a supply deficit this year due to the Iran war.

One Gulf producer warned earlier this month that fully restoring production at one of its UAE smelters hit by an Iranian attack in late March could take up to a year.

The Middle East accounts for about 9% of global production of aluminium, and Chinese aluminium exports are expected to rise as buyers look for other sources of the metal.

Eurozone inflation revised up to 2.6% in March

Over in the eurozone, inflation was faster than initially reported in March,as the Iran war drove up costs.

Statistics body Eurostat has calculated that consumer prices rose by 2.6% in the year to March across the single currency block, up from an initial estimate of 2.5%.

It says:

The lowest annual rates were registered in Denmark (1.0%), Czechia, Cyprus and Sweden (all 1.5%). The highest annual rates were recorded in Romania (9.0%), Croatia (4.6%) and Lithuania (4.4%). Compared with February 2026, annual inflation fell in three Member States, remained stable in one and rose in twenty-three.

Energy prices were 5.1% higher than a year ago, while services inflation came in at 3.2%, and unprocessed food inflation was 4.2%.

UK GDP: More expert reaction

Today’s GDP report suggsts the UK economy began to turn a corner after the Autumn Statement and before the latest developments in the Middle East, says Barret Kupelian, chief economist at PwC:

The UK economy looked to be finding its feet, but geopolitics may yet kick the chair away. Output grew by 0.5% in the three months to February, with both production and services expanding together.

More importantly, this was growth powered by the private sector rather than the public sector-dominated parts of the economy that had propped up much of the post-2023 picture. That suggested the recovery was becoming broader and more durable.

But the question now is whether that recovery can withstand the fresh external shock from the Middle East.

Chris Beauchamp, chief market analyst uk at investing and trading platform IG, says Rachel Reeves and Kier Starmer need to be careful about doing a victory lap:

A look back at last year shows that April 2025 was also good, but then things took a decidedly poor turn. Companies across the UK are warning about the outlook for earnings and consumer spending, and with energy costs hitting consumers hard, today’s good news could turn to dust all too quickly.”

Andrew Wishart, senior UK economist at Berenberg, warns that the Iran war will snuff out the UK’s early 2026 momentum, adding:

Even before the war, we doubted that the economy could enjoy a sustained acceleration. Flat employment, decelerating pay growth and a rising personal tax burden were set to reduce real household spending power.

Now we can add higher energy prices and mortgage interest rates to the list of headwinds. Businesses, meanwhile, face another input cost shock just as they were overcoming the last one (minimum wage and payroll tax hikes). Amid limited pricing power, the squeeze on profitability will probably weigh on output and employment as much as it generates cost-push inflation.

Pre-war, a slowdown in inflation to an acceptable pace should have provided a silver lining to our below-consensus 2026 growth forecast. The new energy price shock means the UK must now endure both weaker growth and higher inflation, postponing bank rate cuts but not derailing them.

The UK economy’s 0.5% growth in February looks to be the fastest monthly expansion since January 2024 (when GDP also rose by 0.5%).

However, the key point is that this strength is likely backward-looking rather than trend-defining, warns Daniela Hathorn, senior market analyst at Capital.com:

The UK economy had been running at a very subdued pace heading into the year, with growth hovering around zero in previous months. This makes February’s jump more of a rebound from weakness than the start of a sustained upswing. In other words, the economy is still fragile, and a single strong print does little to change that broader narrative.

Taiwan overtakes UK in stock market value as AI chip boom continues

Taiwan’s stock market has overtaken the UK, after a surge in the value of its technology sector.

Bloomberg data shows that Taiwan’s market capitalization rose to $4.14trn yesterday, making it the world’s seventh largest, ahead of the UK’s market which was was valued at around $4.09trn.

The landmark came before Taiwan’s benchmark stock index hit a record high today, lifted by Taiwan Semiconductor Manufacturing Co. which reported a 35% increase in quarterly revenue, indicating demand for AI systems remains robust,

“Taiwan continues to be treated as an AI hardware proxy,” said Yoon Ng, head of APAC asset management growth solutions at Broadridge Financial Solutions. “As long as AI capex momentum holds, flows should remain supportive.”

Investec: It’s not all good news….

There is some disappoinment in today’s generally uplifting UK GDP report.

It shows that the economy actually stagnated in the second half of 2025, rather than growing by 0.1% in July-September and October-December.

Sandra Horsfield, economist at Investec, explains:

Not all was good news: revisions to back data mean that Q3 and Q4 GDP growth is now reported as zero, whereas it was +0.1% previously for both quarters.

With that, it is quite possible that full-year 2025 GDP growth is revised down in the next quarterly national accounts release: monthly GDP figures point to a growth rate of 1.2%, whereas the latest quarterly national accounts figures had put GDP growth at 1.4%.

(From today, the ONS has changed its revision policy so monthly GDP can now be revised more frequently than before.) So some of the strong February numbers need to be viewed as bounceback from a lower base.

Here’s Susannah Streeter, chief investment strategist at Wealth Club, on the pick-up on the London stock market this morning:

‘‘The Footsie is off on the front foot in early trade, boosted by hopes of a ceasefire being extended in the Middle East and a surprise boost in the UK’s growth story.

There are much better marks on the UK’s economic report card after the surprise acceleration in activity in February. The 0.5% increase was much stronger than the 0.1% growth figure forecast. This is heartening news, given it shows there is more resilience to deal with the repercussions of the Iran war. Earlier snapshots indicated that the activity had been flatlining, but growth for January has also been revised upwards.

Banks, retailers and housebuilders are among the gainers in early trade as the UK’s fortunes turn a little more positive.

Hopes of an end to the Iran war are pushing up stock markets again today.

In London, the FTSE 100 share index has gained 0.24%, up 25 points to 10,585 points (it was over 10,900 before the conflict began, but fell below 10,000 during March).

Germany’s DAX and France’s CAC share indices are also up around 0.2%.

This follows gains on Wall Street last night, where the S&P 500 index hit a new record high.

News that the US and Iran have been in indirect talks aimed at extending their current two-week ceasefire are lifting stocks.

Michael Brown, senior research strategist at brokerage Pepperstone,says:

By and large, participants continue to focus on the potential light at the end of the tunnel when it comes to conflict in the Middle East, not only as the US-Iran ceasefire continues to hold, but also as the ‘mood music’ more broadly remains relatively positive.

On that note, reporting (via AP) yesterday indicated that the US and Iran had achieved an ‘in principle agreement’ to extend the ceasefire for another fortnight, and that further talks between the two would take place ‘soon’. At risk of repetition, this serves to again underscore that the ‘direction of travel’ is still leading towards de-escalation, as well as reaffirming that both sides are still seeking a deal.

Tesco warns profits could fall amid Iran war uncertainty

Sarah Butler

Tesco has warned that profits could fall back in the year ahead amid “increased uncertainty caused by the conflict in the Middle East”.

The warning came after the UK’s biggest supermarket hit its highest share of the market in a decade.

It revealed profits had risen 8.5% to £2.4bn in the year to 28 February as sales rose by 4.3% to £66.6bn, including strong growth in the UK.

The retailer paid shop floor, distribution workers and other frontline staff a £65m “special performance award” in light of the results, while shareholders have received £937m in dividends during the year.

However, the company said it had “widened” its guidance on profits for the year ahead to £3bn to £3.3bn, adding:

“Much will depend upon the duration of the conflict and in particular, the potential implications for UK households and the economy more broadly.”

Capital Economics: growth my now slow to a crawl

The UK’s “bumper growth in February” has probably already been largely extinguished by the Middle East crisis, warns Capital Economics.

Ruth Gregory, deputy chief UK economist at Capital Economics, says:

GDP rose by a bumper 0.5% m/m in February but March’s activity PMIs suggest the war in Iran has already all-but extinguished growth. And in our baseline scenario we think GDP growth will slow from 1.4% in 2025, perhaps to just 0.7% this year.

Gregory fears growth will “slow to a crawl in the coming quarters”, saying:

The stronger February outturn than we expected probably meant that GDP grew by 0.6% q/q or so in Q1, rather than 0.3% q/q as we previously thought. But the leap in energy prices means there is unlikely to be much growth after that.

[PMIs are a survey of purchasing managers, which showed the biggest jump in costs since 1992 last month]

Anna Leach, chief economist at the Institute of Directors, warns that the UK is ‘uniquely vulnerable’ to the energy shock:

“Revisions to GDP show that, ahead of the conflict in the Middle East, the economy was picking up from a dip in activity last summer. However, as the conflict drags on, reports continue to grow of escalating energy costs, paused decision making and concerns over potential shortages of critical inputs.

The UK’s tight financing conditions, high initial starting point for inflation, uncompetitive energy costs and low fiscal space, make us uniquely vulnerable to the situation.

JP Morgan: oil price spike could mean the UK economy’s return to growth is short-lived

Scott Gardner, investment strategist at J.P. Morgan Personal Investing fears the UK’s growth pick-up may not last, due to the Iran war.

“The UK economy beat expectations in February, showing strong growth during the month before the war with Iran broke out. While this is a positive reading, the uncertain situation in the Middle East and resulting spike in oil prices could mean this return to growth is short-lived.

“In February, industrial production and services rose sharply. The rise was partly offset by manufacturing activity contracting. Retail sales fell after a stronger than expected January while the property market remains subdued.

“Looking ahead, the conflict in the Middle East and escalation in the Strait of Hormuz has dented the growth outlook for the UK economy. Oil prices had already been rising in recent months, but the latest spike could be especially painful for businesses and consumers through higher costs and elevated interest rates.

The extent to which the conflict hits UK growth this year will hinge on the duration of the disruption in the Strait of Hormuz and persistence of the oil price shock, Gardner adds.

February’s growth shows UK probably on “a stronger footing” than expected before energy shock

February’s GDP report shows “the calm before the storm” that is now hitting the UK economy from the Middle East, reports Sanjay Raja, Deutsche Bank’s chief economist.

Raja says February GDP “smashed expectations” by coming in with “a thumping 0.5%” growth month-on-month this morning.

He says it shows forecasters were too pessimistic about UK growth at the start of the year, and predicts we’ll see decent growth of up to 0.6% in the first quarter of this year.

Our nowcast models now show Q1-26 GDP growth returning back to our original forecast from the start of the year: 0.5-0.6% q/q, reflecting some positive payback after a very sluggish second half in 2025. Given today’s data, spending looks stronger than anticipated. And firms may also be investing more than we thought heading into the Iran conflict.

But the impact of higher energy prices, and weaker business investment, will hurt growth this year, he adds:

The good news is that the UK likely entered the energy shock on a stronger footing than many expected. Q1-26 GDP growth will likely hit more than double the quarterly rate many forecasters expected, also lifting annual GDP growth projections. The bad news is that upward GDP momentum won’t last. This will likely be the growth before the energy squeeze.

Households will have already started to feel the impact of the Iran energy shock, impacting disposable incomes and discretionary spending. Pump prices are up over 20% since the oil shock occurred. And dual fuel bills are due to rise by a similar amount over the summer. Businesses will also likely be pulling back investment plans, hiring plans, and lowering wage growth as a result. As such, expect more sluggish growth into Q2-26 (and beyond).”