Funtay

Looking for alternative income for your portfolio?

Energy royalty trusts often offer high-yield income on crude oil, natural gas and natural gas liquids.

While Dorchester Minerals, L.P. (NASDAQ:DMLP) is not a trust, it operates on a similar principle as most energy trusts. It collects royalties, has very limited expenses, and pays out 100% of its net income to unit holders.

Company Profile:

Dorchester Minerals, L.P. (the “Partnership”) is a publicly traded Delaware limited partnership that commenced operations on January 31, 2003. Our business may be described as the acquisition, ownership and administration of Royalty Properties (which consists of producing and nonproducing mineral, royalty, overriding royalty, net profits, and leasehold interests located in 594 counties and parishes in 28 states (“Royalty Properties”)) and net profits overriding royalty interests (referred to as the Net Profits Interest, or “NPI”). (DMLP 10Q)

Holdings:

Oil dominates revenues at 77%, vs. 14% for natural gas and 8% for natural gas liquids. Royalties comprise 72% of revenues, followed by Net Profit Interests, NPI, at 26%, and other sources, at 2%.

DMLP site

The Permian Basin remains the largest source of revenues, at 60%, followed by the Bakken, at 38%. DMLP also has some minor holdings in the Fayetteville and other basins:

DMLP site

Reserves:

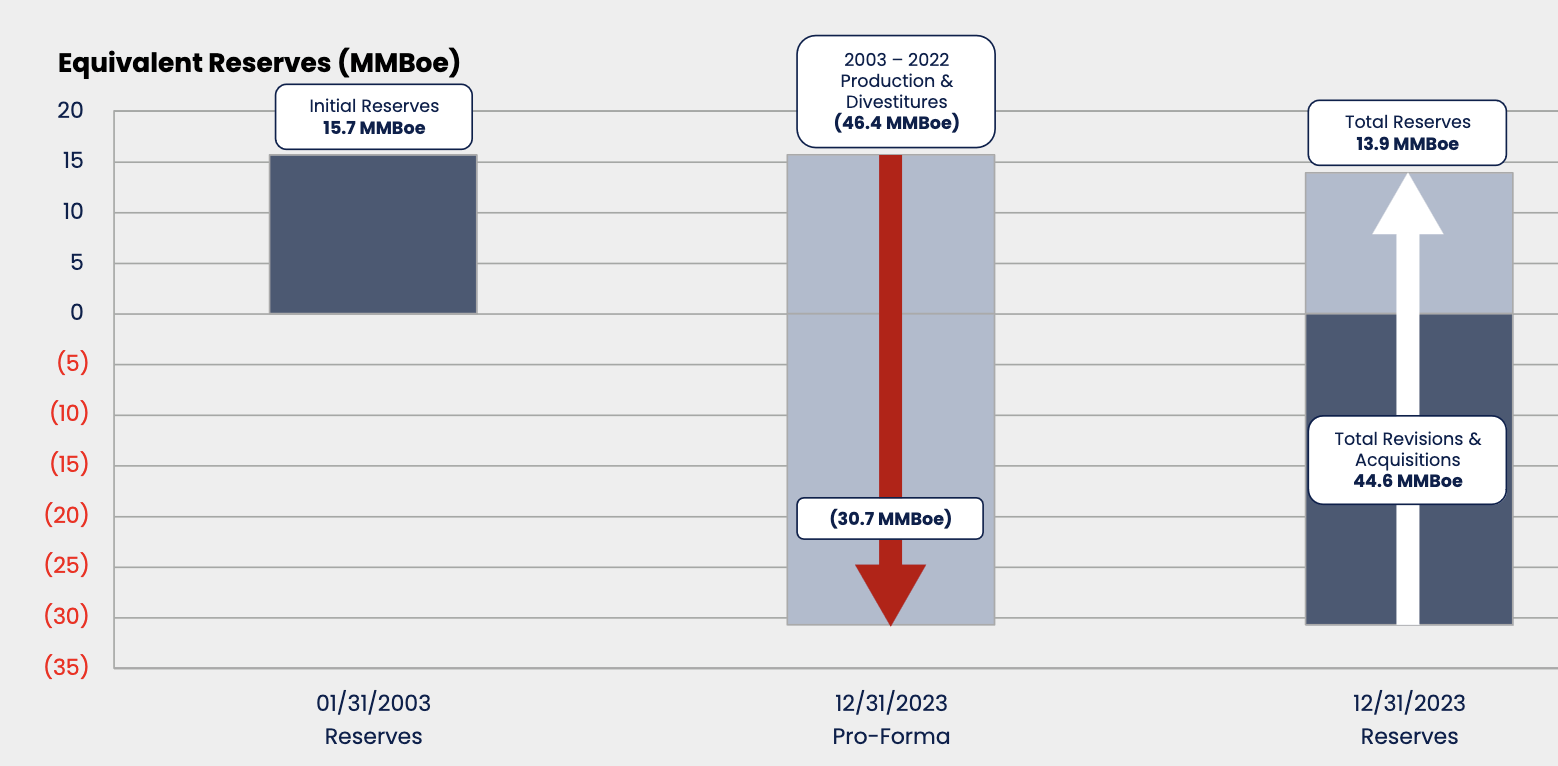

A big advantage for DMLP vs. similar firms is that it’s allowed to acquire more acreage in order to bolster its reserves. Some energy trusts, such as MVO, have a fixed amount of energy reserves, which, when they reach a certain point, will trigger the termination of the trust.

DMLP’s initial reserves, as of 1/31/03, were estimated at 15.7 MMBoe. Around 20 years later, they were still 13.9MMBoe, even though it had used 46.4MMBoe in Production and Divestitures as its cumulative reserve revisions and acquisitions have exceeded 100% of Current Reserves:

DMLP site

Earnings:

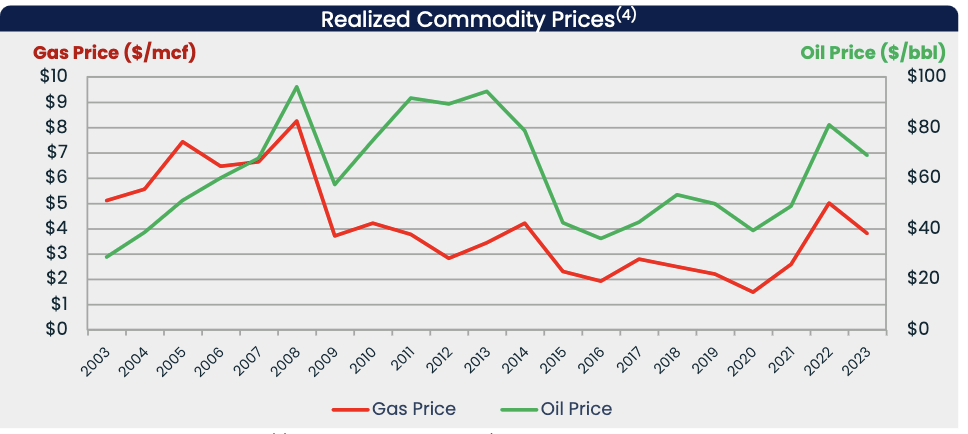

As you would expect, DMLP’s earnings are tied to the prices of oil, natural gas, and LNG. Prices hit a long trough in ~2015 to 2020, but made a sharp recovery beginning in ~2021, and peaked in mid-2022, but are still much higher than during the trough years:

DMLP site

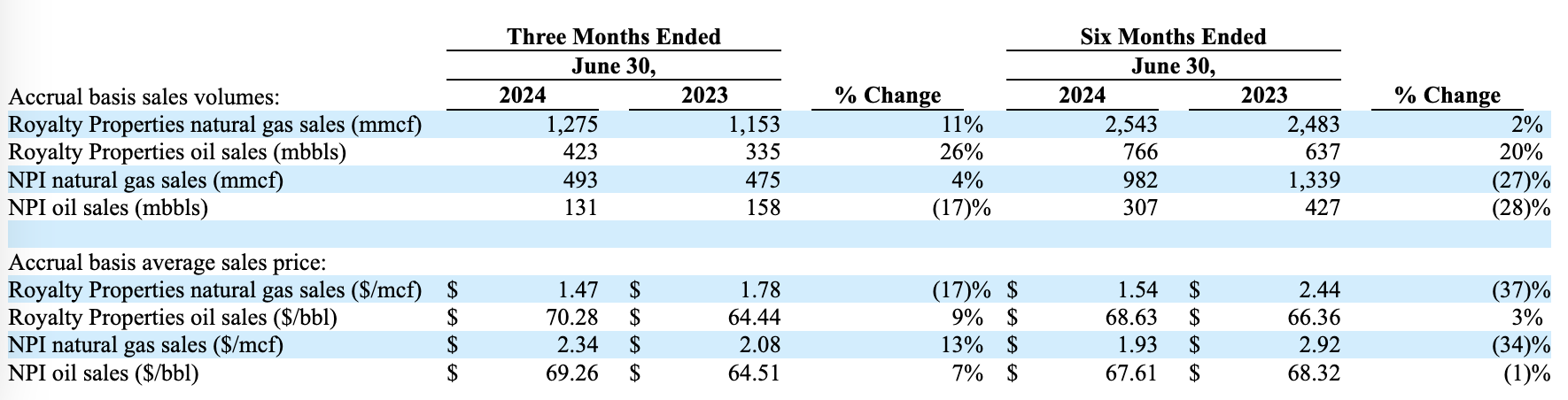

DMLP’s oil and natural gas royalties sales volumes increased 11% and 26% in Q2 ’24, respectively. NPI natural gas sales also rose 4%, but NPI oil sales fell 17% vs. Q2 ’23.

The average sales price for natural gas royalties fell 17%, while the average sales price for oil rose 9%. NPI natural gas prices rose 13%, to $2.08, while NPI oil’s sales price rose 7%, to $69.26.

Q2 ’24 was an improvement over Q1 ’24, as seen in the lower gains and higher declines in year-over-year volume and sales prices for the six-month period ending 6/30/24:

DMLP site

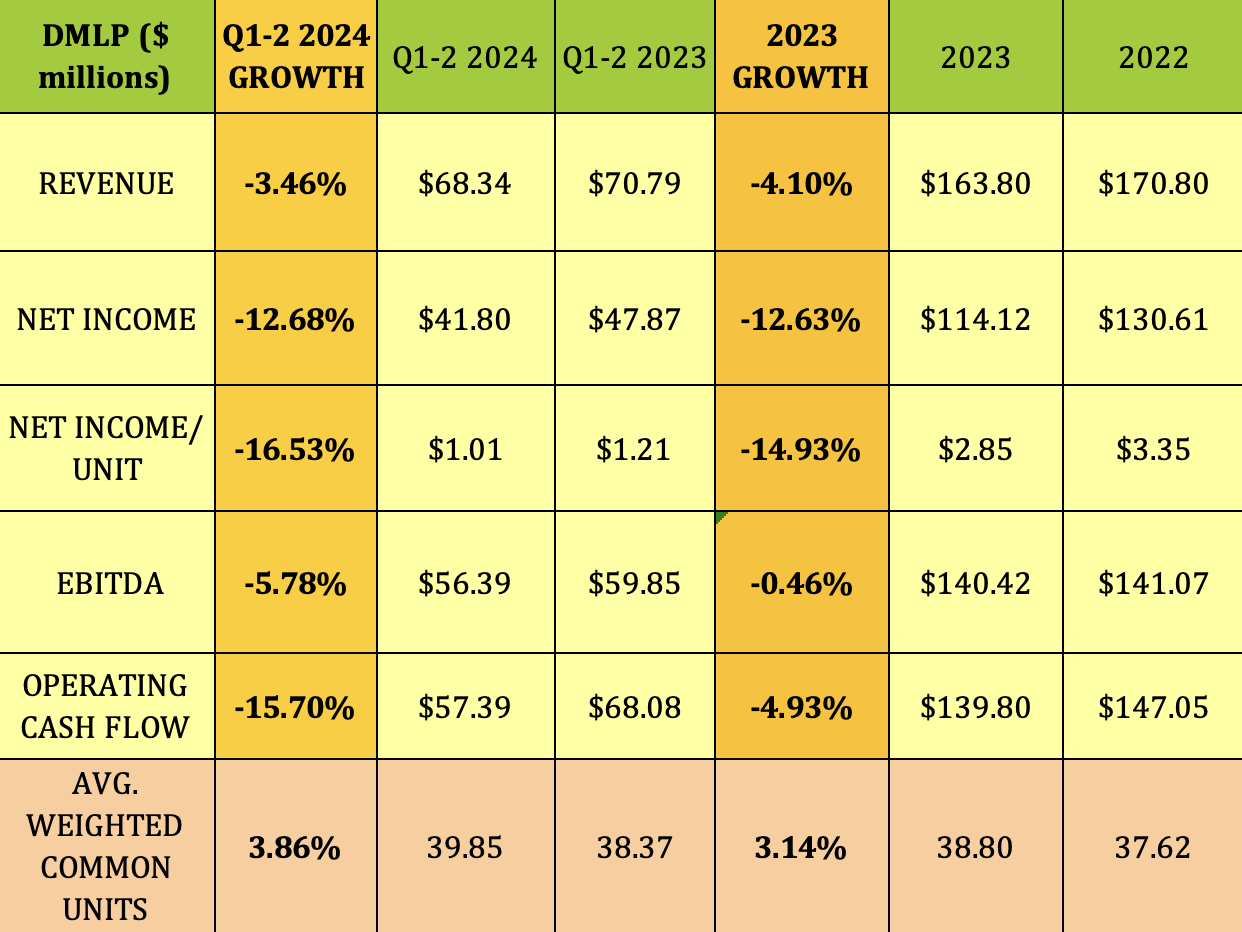

Q1-2 ’24: Overall revenue was down slightly, -3.6%, while net income fell 12.7%. Net income/unit fell 16.5% due to a higher unit count.

EBITDA was down 5.8%, while operating cash flow fell 15.7%.

Hidden Dividend Stocks Plus

Acquisition:

The bump in the share count was related to a new acquisition:

“On March 28, 2024, pursuant to a non-taxable contribution and exchange agreement with multiple unrelated third parties, the Partnership acquired mineral interests totaling approximately 1,485 net royalty acres located in two counties in Colorado in exchange for 505,369 common units representing limited partnership interests in the Partnership valued at $17.0 million.” (DMLP 10Q)

Dividends:

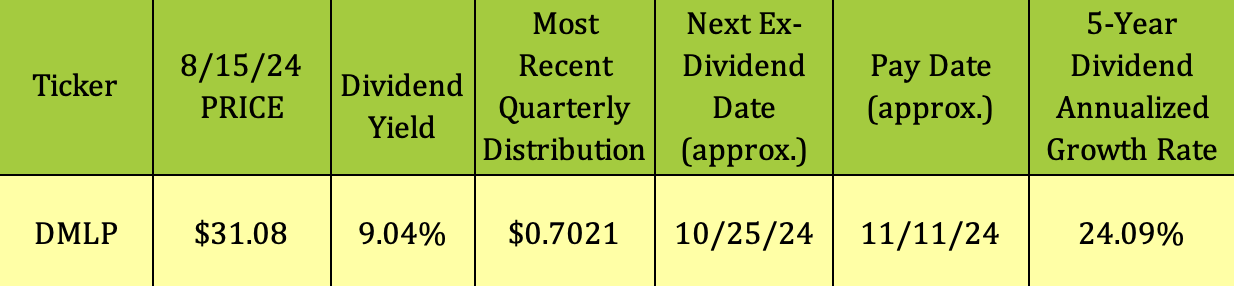

DMLP’s most recent distribution was $.7818, which gives it a forward yield of ~9%. However, since it relies on pricing and volume for its earnings, DMLP pays a variable distribution.

DMLP has a very high five-year dividend growth average of over 24% due to a 128% jump in distributions in 2022 vs. 2021.

Hidden Dividend Stocks Plus

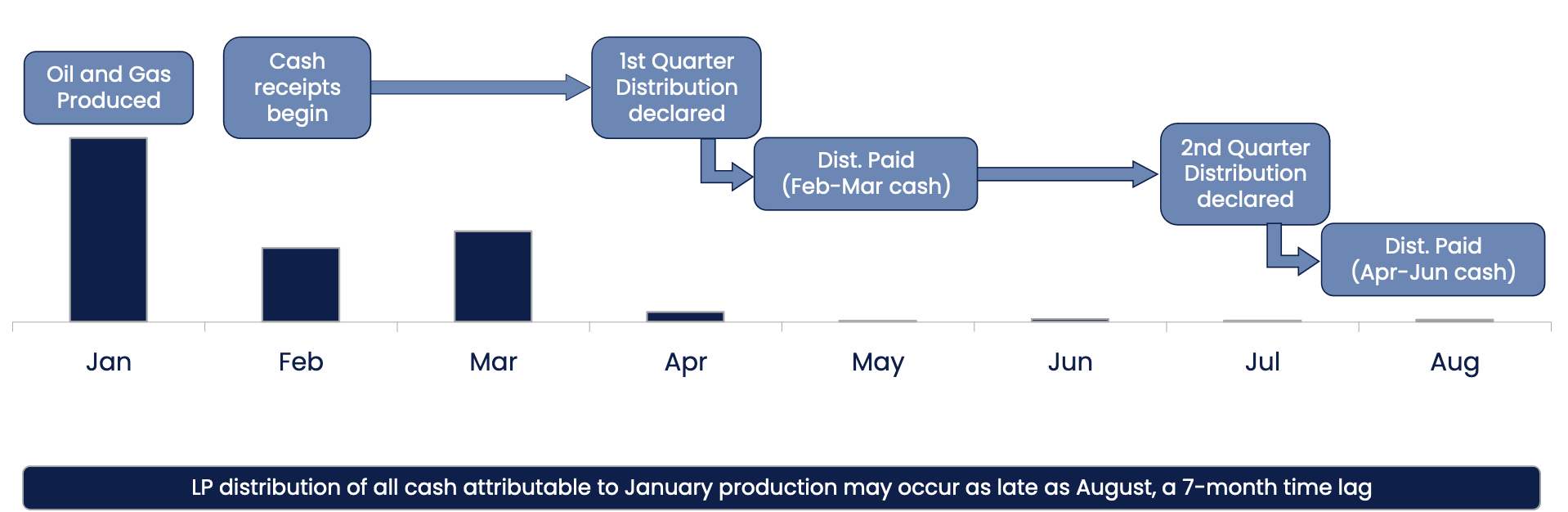

It’s very difficult, to say the least, to assess distribution coverage for DMLP, as its payouts can lag production by up to seven months:

DMLP site

Taxes:

DMLP issues a K-1 to unitholders at tax time. LP distributions may include return of capital, which offers you a tax deferral benefit, but also decreases your tax basis. Please consult your tax advisor for more details.

Insiders:

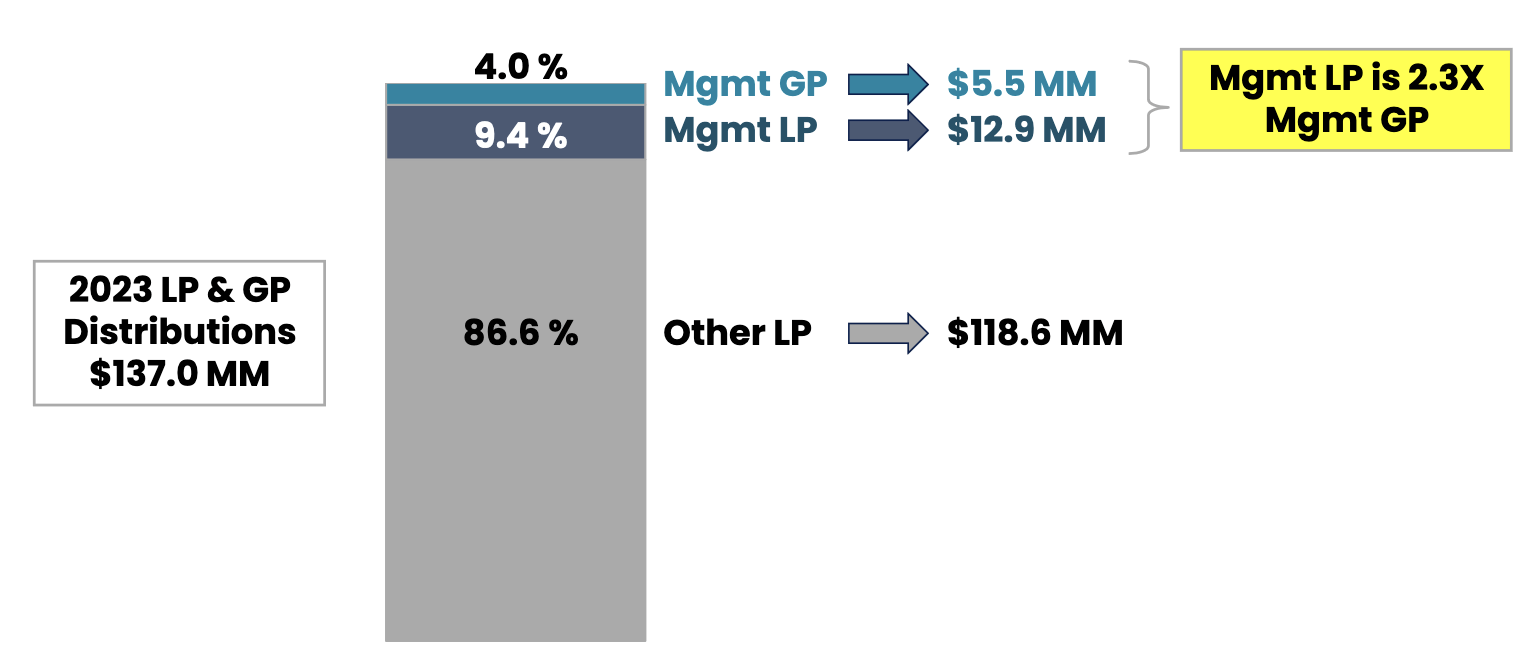

Another advantage of DMLP is that its management has no incentive to make dilutive transactions, as its limited partner interest is 2.3X its general partner interest, which also receives no incentive distribution fee.

CEO Ehrman bought 2800 units at $29.50 in mid-June ’24, bring his total unit count to over 102,000.

DMLP site

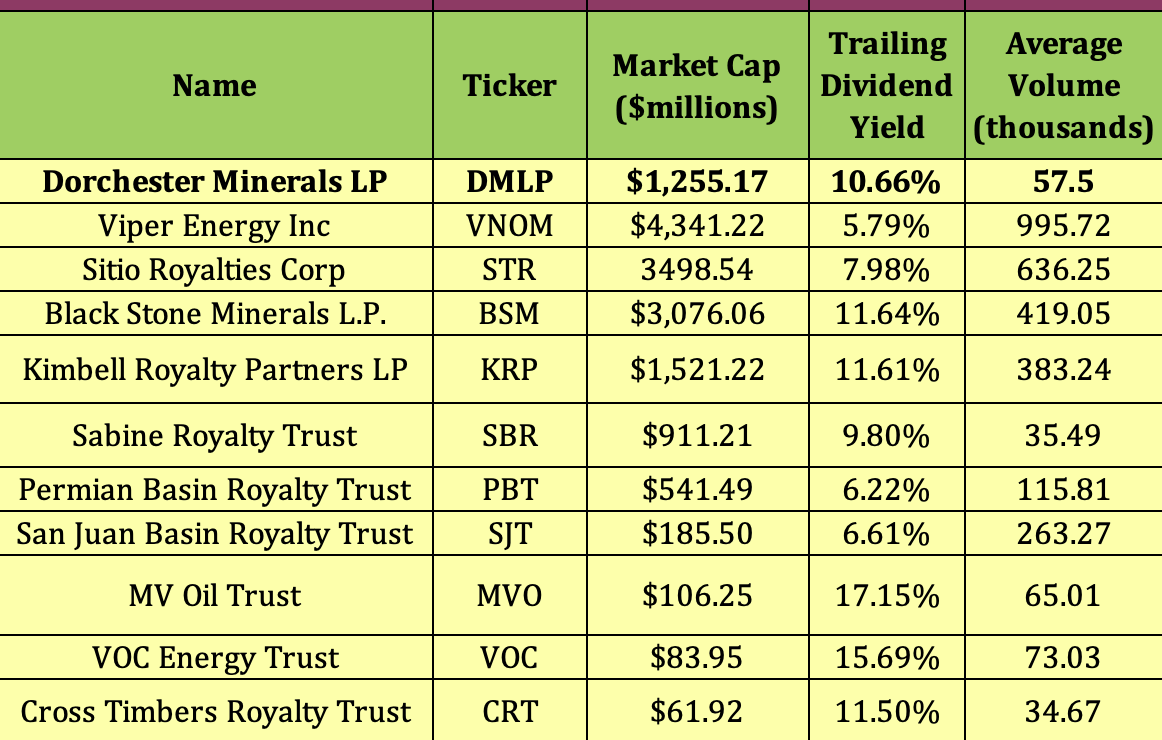

Peers:

There are several royalty trusts that offer high-yield distribution income, ranging from 5.8% to 17%.

Viper energy (VNOM) is the biggest, with a $4.3B market cap, followed by Sitio Royalties (STR), with a $3.5B cap, and Black Stone Minerals, (BSM), with a $3B cap. DMLP is in the next tier, with a $1.25B cap, below Kimbell Royalty (KRP), with a $1.5 cap. This table also includes six trusts with sub-$1B caps, with Sabine Royalty (SBR) at $911M, down to Cross Timbers, at $62M.

DMLP is in the lowest tier for daily volume, at 58K, whereas VNOM and STR have the highest volume, at 995K and 636K, respectively.

Dividend yields run all the way up to 17% for MVO, an entity which is close to its termination reserve amount.

VOC, which terminates in 2030, yields 15.7%.

DMLP. with its 10.66% yield, is in the middle group, where yields run from 9.8% for SBR, to ~11.5-11.6% for CRT, KRP, and BSM.

The lowest-yielding group includes VNOM, at 5.8%, PBT, at 6.2%, SJT, at 6.6%, and STR, at 7.8%.

Hidden Dividend Stocks Plus

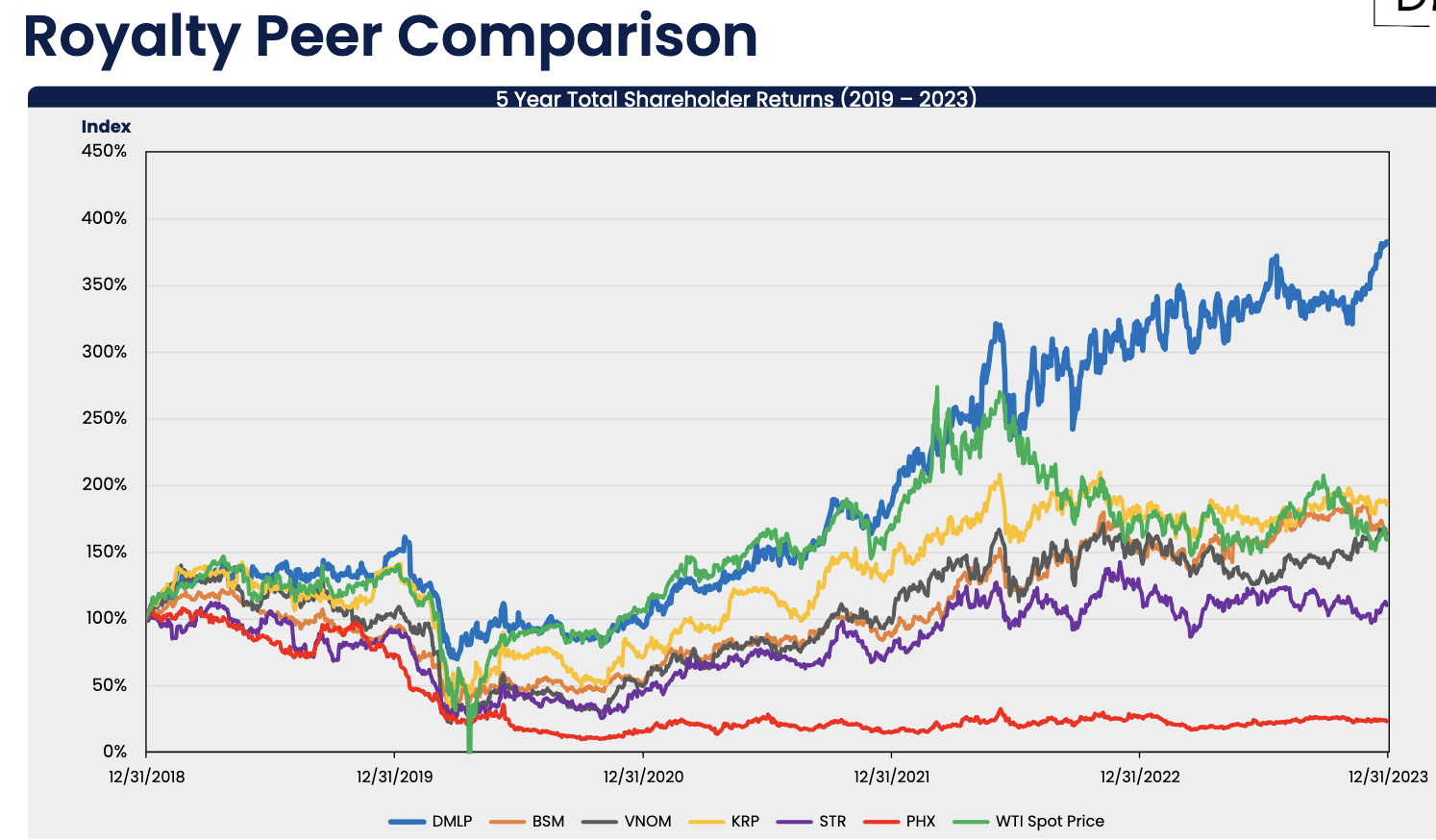

DMLP’s peer comparison chart shows a much higher five-year return of over 350% vs. its peers’ range of ~25%-175% for the period 2019-2023:

DMLP site

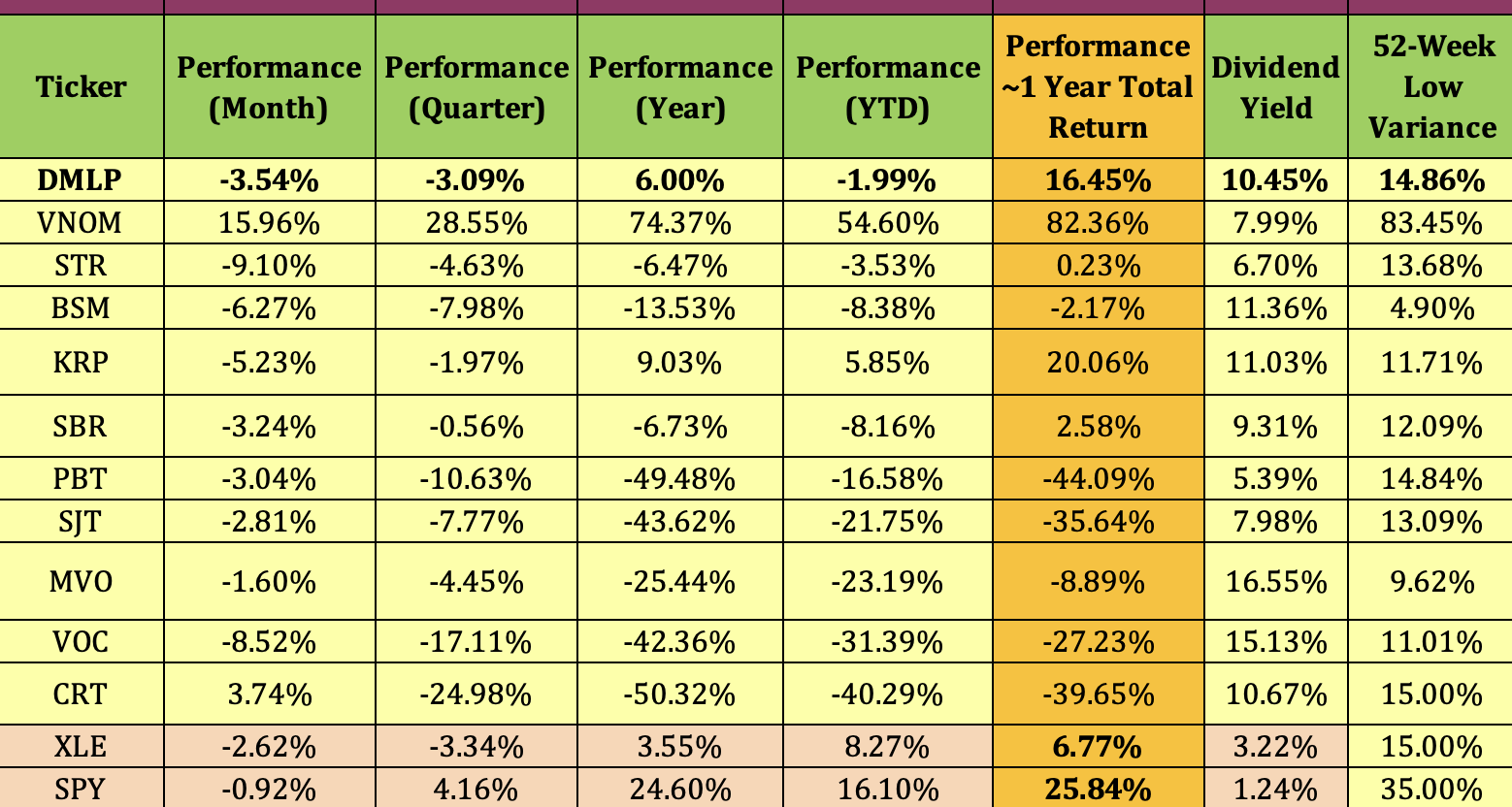

Performance:

The majority of these trusts have had a rough time of it over the past year, with analysts predicting lower crude prices.

DMLP’s total return of ~16.45% has outperformed most of them, except for VNOM and KRP. It has also outperformed the broad energy sector during the past year.

DMLP has fallen ~3.5% over the past month, lagging the energy sector and the S&P. VNOM, partially owned by rapid grower Diamondback Energy (FANG) keeps chugging away, rising ~16% in the past month.

Hidden Dividend Stocks Plus

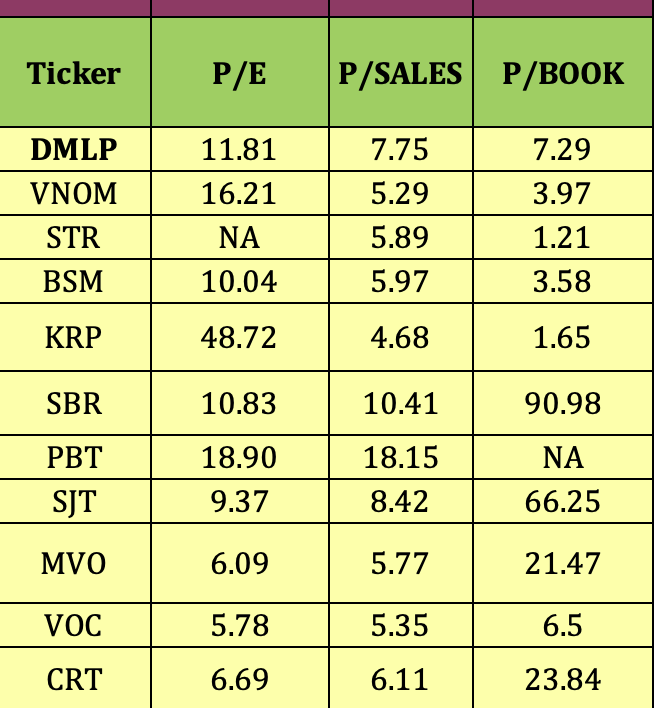

Valuations:

We don’t see DMLP having any low valuations, but this may be a case of “you get what you pay for,” in light of its positive history. Many of the laggards in this group have the lowest valuations. DMLP’s 52-week range is $27.16 – $35.74.

STR is the cheapest in this group on a P/Book basis, at 1.21X, followed by KRP, at 1.65X.

KRP also has the lowest P/Sales ratio, at 4.68X, while VOC has the lowest P/E, at 5.78X.

Hidden Dividend Stocks Plus

Parting Thoughts:

We rate DMLP a “Hold Off” for now. You may be able to pick up shares cheaper if there’s a September-October pullback. It could be a good long-term, high-yield energy asset at a lower entry price.

All tables furnished by Hidden Dividend Stocks Plus, unless otherwise noted.