Today’s clients want more than investment advice.

Research shows that consumers want comprehensive, holistic financial guidance. They understand that no single advisor can be an expert in every area of wealth management, but they want a trusted partner who can coordinate the expertise, identify the opportunities and connect the dots.

Most clients are seeking the benefits of a family office, even if they don’t know to call it that. Canadians would benefit from this. But it is increasingly difficult for financial advisors to deliver.

Tax legislation grows more complex each year. Investment planning strategies continue to evolve. Risk management options expand. Debt management decisions become increasingly sophisticated.

Not only must advisors understand these disciplines, they must also communicate them in a way that clients can grasp. That is where many advisors struggle.

Knowledge alone does not create expertise in the eyes of a client. The ability to organize, simplify and communicate that knowledge often makes the difference between being perceived as a product provider and being recognized as a trusted expert.

The late Dr. Anders Ericsson, renowned psychologist and author of Peak: How to Master Almost Anything, spent decades studying world-class performers across numerous professions. One of his most important discoveries was that experts organize information differently than novices.

“The superior organization of information is a theme that appears over and over again in the study of expert performers,” Ericsson wrote.

This principle applies just as much to financial advisors as it does to athletes, musicians and physicians. Experts develop what Ericsson called “mental representations.” These frameworks allow them to quickly recognize patterns, organize information and communicate complex ideas effectively.

Novices focus on individual facts. Experts understand how those facts fit together.

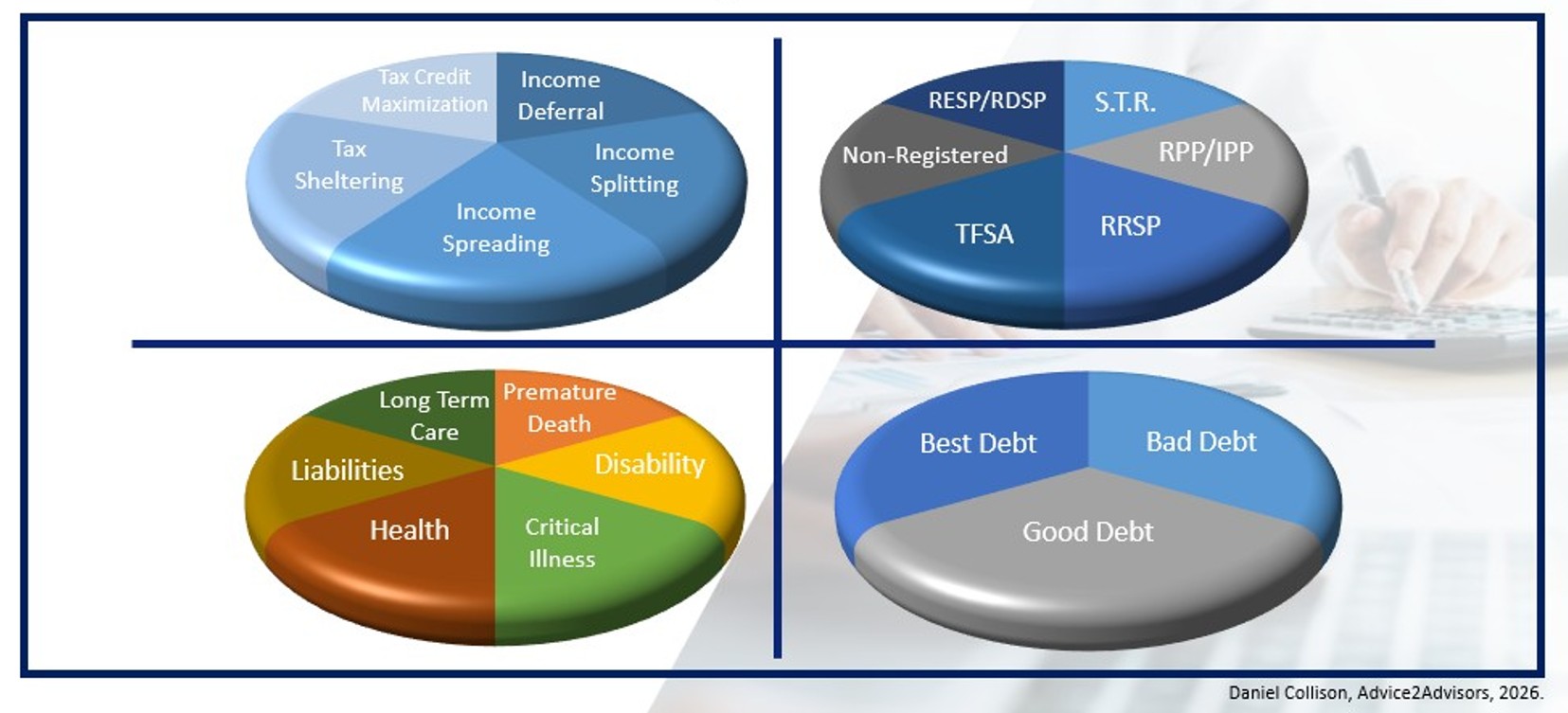

Virtually every wealth management discussion can be organized across four interconnected portfolios: tax planning, asset management, debt management and risk management.

4 portfolios

When advisors memorize these four portfolios and learn to sketch them during client conversations, they create a powerful visual mental representation for prospects and clients. Rather than discussing isolated products or planning ideas, they demonstrate a complete wealth management system.

Clients immediately begin to understand how all the pieces fit together. And they better recognize the advisor’s expertise.

Tax planning

Let’s start with the tax planning portfolio.

Consider a prospect meeting. Instead of immediately discussing investments, ask for a rundown on any tax-planning strategies currently in place. The answer is typically limited to RRSP contributions, TFSAs and perhaps some income splitting.

Next, expand the discussion to the five major categories of tax minimization:

- Income deferral: Strategies such as RRSPs, individual pension plans, capital gains deferral and corporate structures.

- Income splitting: Spousal RRSPs, prescribed-rate loans, family trusts, RESPs, estate freezes and other strategies designed to shift income to lower-taxed family members.

- Income spreading: Techniques that distribute income over multiple years, including capital gains reserve provisions, structured severance arrangements and prescribed annuities.

- Tax sheltering: Strategies such as TFSAs, first home savings accounts, investment loans, debt swaps, the lifetime capital gains exemption and other tax-efficient planning approaches.

- Tax credit maximization: Personal tax credits, age credits, dividend tax credits, charitable donation credits, disability credits and other opportunities to be used now and in the future.

As each category is discussed, ask which strategies the prospect is currently utilizing and place a checkmark beside those that apply.

Something remarkable happens during this exercise. Within minutes, the prospect gains a visual understanding of the entire tax planning landscape. They can see what they’re doing and what they’re missing.

You’re not criticizing; you’re broadening the focus. In doing so, you create a powerful comparison between the advice the prospect is currently receiving and the advice available from you.

Applying the same approach to asset management, debt management and risk management takes about 20 minutes. In less time than many advisors spend reviewing investment performance, a prospect gains a comprehensive understanding of holistic financial planning.

They see how taxes affect investments. They see how debt can influence wealth, both positively and negatively. They understand how risk management protects both human and financial capital — ultimately, financial goals. They start to recognize the interconnected nature of every major financial decision.

Most importantly, they begin to view the advisor not as an investment or insurance advisor, but as a wealth management strategist — a personal CFO.

Simplify complexity

This takes practice, of course.

Establish specific learning goals for yourself; commit to studying the framework until it is second nature; seek feedback; and challenge yourself to present to increasingly sophisticated audiences.

Clients don’t hire advisors because they have access to information. Information is everywhere.

Clients hire advisors because they can organize complexity, provide clarity and help them make better decisions.

By helping prospects visualize their finances, you can create a more meaningful planning conversation and demonstrate genuine expertise.

Source link