Urupong

Introduction

iShares S&P 500 Growth ETF (NYSEARCA:NYSEARCA:IVW) is an exchange-traded fund that invests in “large U.S. companies whose earnings are expected to grow at an above-average rate relative to the market”, as per iShares. The fund seeks to replicate its chosen benchmark index, the S&P 500 Growth Index. The methodology selects for stocks based on three factors: sales growth, the ratio of earnings change to price, and momentum (per S&P methodology):

[Sales:] Three-Year Net Change in Earnings per Share (Excluding Extra Items) over Current Price

[Growth:] Three-Year Sales per Share Growth Rate

[Momentum:] Momentum (12-Month % Price Change)

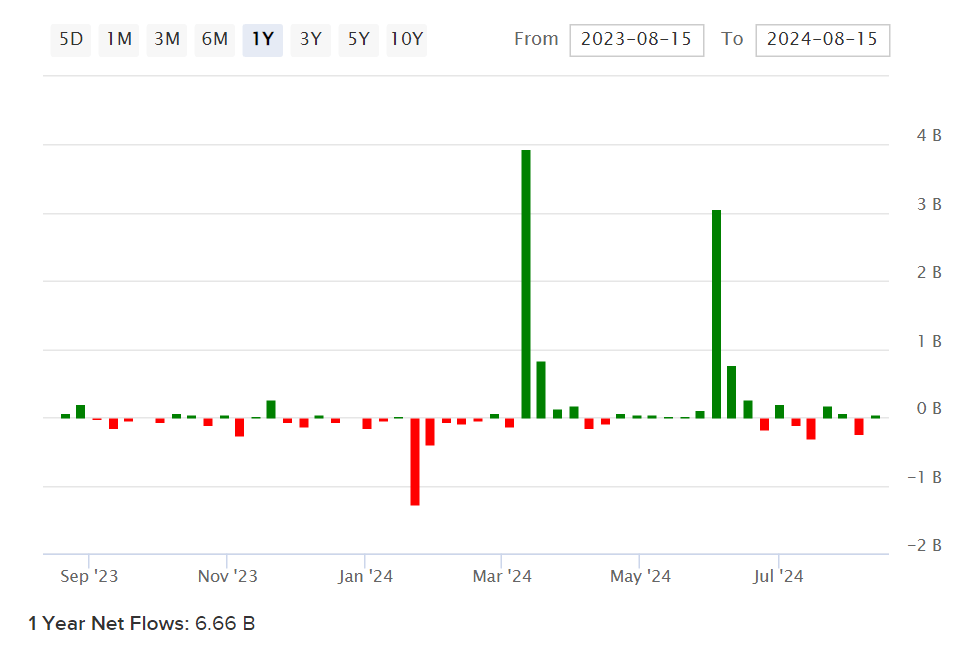

This is a simple methodology and ultimately results in a portfolio of some 231 holdings (in IVW as of August 16, 2024). The fund currently has net assets under management of $52.65 billion, making IVW relatively large in the ETF space, and this also follows a surge in popularity with net inflows of $6.7 billion over the past year or so.

ETFDB.com

We should also note early on that the expense ratio is 0.18%, which is not high, but also not extremely low; for a U.S.-only growth stock fund, I would suggest this must be quite a profitable entity for iShares to manage. Higher expense ratios rarely break theses, but we must factor this into our valuation equation. The bid/ask spread is very low, at 0.01% on a 30-day median basis.

I last covered the fund on June 6, 2022, where I took a neutral stance with an expectation that an IRR above 10% could be achievable (at the time). The reason I took a neutral stance was that I thought better or safer alternatives existed at the time, and 2022 was indeed a bad year for investing; IVW registered a low after June 6 of $55.30 on October 13, 2022, before finally ramping upward. Since my article however, I was roughly correct in my estimation of the fund’s IRR potential, at least directionally. Since my article, the price-only compound annual growth rate comes in at 16.37% by my calculations, which is even stronger than my less conservative guess.

Based on the current portfolio, I think it makes sense to revisit IVW to gauge the potential IRR on offer based on (mostly) consensus expectations of earnings growth, especially since growth stocks have powered higher in recent times.

Portfolio

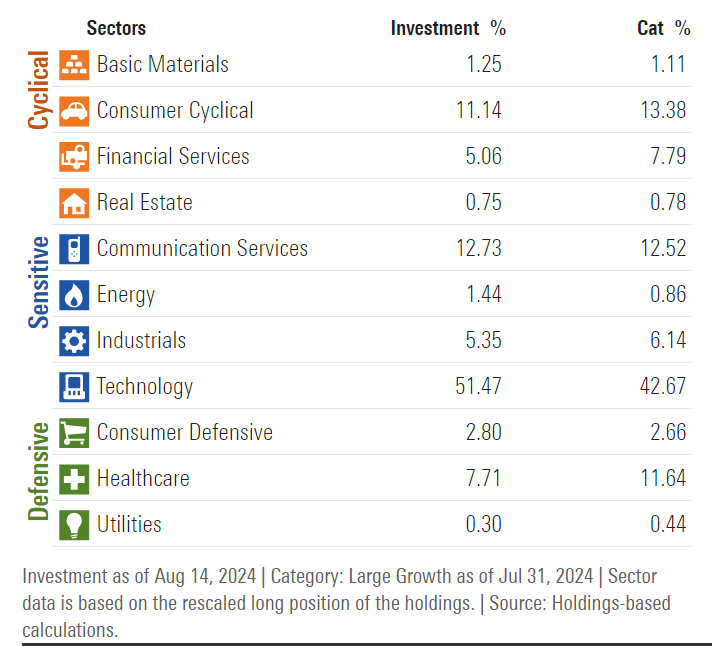

The current IVW portfolio is expectedly over-weight Technology (at 51.47%), followed by Communication Services (at 12.73%, and which contains some names often considered to be Technology stocks), followed by Consumer Cyclical (at 11.14%). Mostly, IVW is a very pro-cyclical fund which is likely to get hit in a recessionary scenario to some extent (albeit perhaps less than small-cap growth stocks), but do very well in an easy fiscal and monetary environment.

Morningstar.com

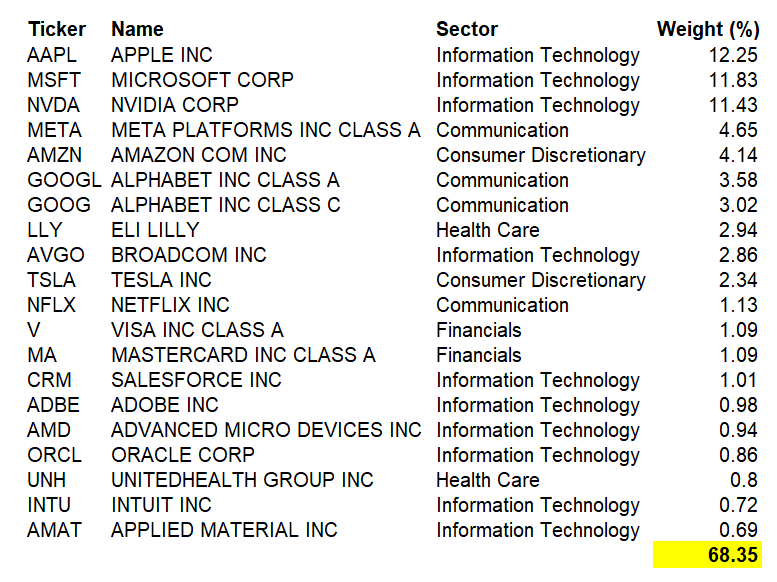

Below, you can find a list of the top 20 stocks in the IVW portfolio as of August 15, 2024, and as you can see, 68% of the fund was represented by just 20 stocks.

Data from iShares.com

This list includes some household names like Apple Inc (AAPL), Microsoft Corp (MSFT), Nvidia Corp (NVDA), Meta Platforms Inc (META), Amazon.com Inc (AMZN), and Alphabet (GOOGL) (GOOG). Indeed, these names alone represented 50.9% of the fund in isolation, making IVW very exposed to the AI sector today, and “Big Tech” in general. Nevertheless, AI is an exciting place to be, and the nature of market-cap-weighted ETFs such as IVW is such that winners and losers tend to gain and lose weights over time through quarterly rebalancings. With high historical (and high near-term/projected) returns on equity, the existing portfolio (especially among the top stock exposures) is, on average, a very strong and performant selection of U.S. companies. Nevertheless, a valuation check is always worthwhile.

Valuation

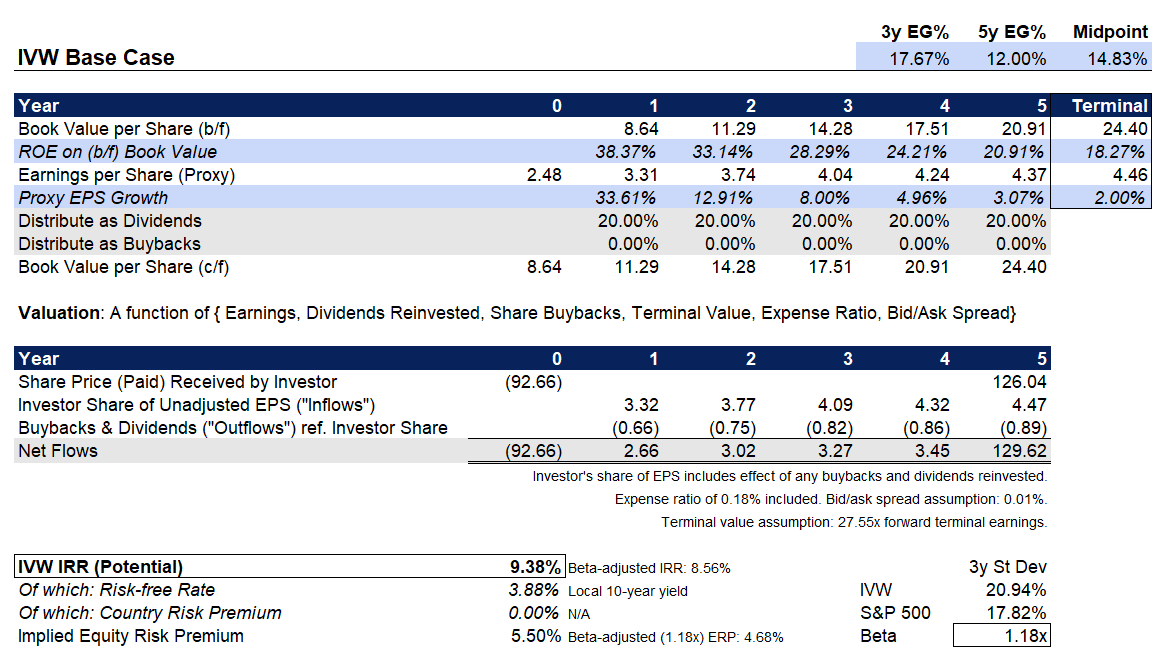

The most recent factsheet cited earlier for IVW’s benchmark is a good starting point for assessing the portfolio’s earning capacity. Unfortunately, a trailing price/earnings ratio is not available, however iShares report a trailing (albeit adjusted figure, for negative-earning companies) of 37.33x as of August 15, 2024. On this date, the share price for IVW was $92.57, so the notional trailing earnings per share was about $2.48/share. I will normalize this as of July 31, 2024 (to correspond with the factsheet I will work from, hereafter) for an adjusted trailing price/earnings ratio of 36.81x.

The factsheet for the S&P 500 Growth Index, as of July 31, 2024, reported a forward price/earnings ratio of 27.55x, with a price/book ratio of 10.57x and an indicative dividend yield of 0.68%. Together, these figures imply a roughly one-year earnings growth rate of 33.61%, and an implied forward return on equity of 38.37%. Meanwhile, Morningstar reports a consensus three- to five-year average earnings growth expectation of 15.87%. Most of this is likely to be driven by the near-term earnings forecasted, and so we can safely re-rate the annual growth rate downward to hit a figure at or below 15-16%.

In sum, I have opted for a gradual maturation of IVW’s return on equity from 38% on a forward basis to sub-19% by our terminal year six, which implies a three- to five-year earnings growth rate of 12-18%, with a midpoint of 14.83%. To be honest, if anything this might seem a little bit on the optimistic side of things. While the portfolio is essentially a laundry list of the strongest companies in “corporate America”, this does not leave a great margin for error. Nevertheless, proceeding with this slightly sub-consensus base case, the implied IRR for IVW comes to just under 10% per year.

Author’s Calculations

This is a decent-enough and healthy return profile, and factors in all the costs previously discussed. However, for a fund with a beta of 1.18x (as shown above; see bottom-right of the chart), the adjusted equity risk premium is “just” 4.68%. A healthy range is 3.2-5.5%, with the higher the better from an entry point perspective. To me, IVW actually looks roughly fairly valued, which is less attractive as compared to some of the other growth-oriented funds I have seen recently, which also have lower average earnings growth expectations and thus likely greater margins of safety. In an ordinary environment, IVW would look attractive, but I think there are other funds offering better IRRs with at least slightly less risk. Therefore, I would take a neutral stance at present (but with a generally bullish bias).

IVW is probably going to benefit from the next round of rate cuts from the Federal Reserve, even if they come belatedly (the consensus that is emerging suggests the first cut will come next month, in September 2024). So far, economic data has showed little justification for an expectation of a harsh recession. As a result, I don’t see significant risks in terms of macro headwinds for IVW. An unknown unknown, tail event (e.g., outbreak of war) could hit IVW, but at least these businesses would likely benefit from any subsequent monetary/fiscal easing, with pricing power to protect against dramatic declines.

In summary, IVW offers an IRR above 9% in a base case scenario, which is strong. However, as risks and uncertainties always persist in the real world, it makes sense to explore other funds with higher IRR potentials with less rosy average earnings expectations.