da-kuk

Key takeaways

- Strong absolute and peer- relative performance

- Class A shares at NAV had a positive return for the quarter (5.35%) and outpaced the Morningstar large-cap growth fund category average (5.10% category return) and finished ranked 695 out of 1191.

- Technology and AI drove quarterly results

- Information technology and Artificial Intelligence related stocks drove equity returns, particularly in May and June.

- We believe a slowing economy will benefit growth-oriented stocks

- We expect the US economy to continue to cool, slowed by the lagging effects of tighter financial conditions, and we believe investor sentiment will favor companies that can compound their growth over the long term.

Manager perspective and outlook

Equity results diverged in the second quarter. Stocks related to AI continued to rally; other market segments declined.

First quarter Gross Domestic Product (GDP) growth was below expectations, suggesting to us that the US economy has been finally slowing.

Corporate earnings were generally positive, but earnings growth was concentrated, as the “Magnificent 7” stocks (Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta and Tesla) accounted for most of the gains.

The US Federal Reserve’s (Fed) June meeting produced no change to the federal funds rate as inflation has remained above the Fed’s 2% target. Given the current environment, we have emphasized both higher quality companies with resilient earnings growth and companies that have been winning market share due to industry and technological shifts over cyclical goods and services companies. Rising demand for cloud computing and data management services and increased monetization for AI enablers have supported strong fundamentals for companies in these areas. We believe the greatest opportunity, which is still to come, will be in AI software and services. While economic data has been mixed, we believe slowing economic activity, receding inflation, tight financial conditions and higher debt costs boost the likelihood of Fed easing over time. In our experience, slow-growth economies have been favorable for the type of innovative, organic growth companies emphasized in the fund.

Portfolio positioning

The fund’s largest overweights include financials, industrials and communication services. We believe financials and industrials stocks are attractive given a potential interest rate peak.

Among financials, we favor capital markets and securities exchanges over payment companies and banks. Industrials exposure is focused on electrification, AI-related data center builds and infrastructure stimulus spending. We believe communication services will benefit from ecommerce penetration and streaming media services. Near term, we see AI improving the return on investment for digital advertising and entertainment, along with opportunities for new AI applications and automation. We increased the fund’s still-underweight Apple position. The fund remains underweight in IT, largely due to underweights in Apple and Microsoft. The fund’s health care weight matches the index as we seek to balance typical election year underperformance with attractive valuation and fundamental opportunities.

New Positions

Microchip Technology (MCHP): This manufacturer of microcontrollers, a basic building block of all things digital, should in our view benefit from a clearing of its inventory.

Spotify Technology (SPOT): Continued price increases across music distributors confirm to us a healthy competitive structure. Spotify can likely take advantage of strong operating leverage, while podcasts and audiobooks likely offer opportunities for incremental penetration and monetization.

Ivanhoe Mines (OTCQX:IVPAF): Multiple factors including electrification, renewable energy, electric vehicles, reshoring and AI have been driving copper demand.

Blue Owl (OBDC): We expect this alternative asset manager to benefit from increased demand for private market investments and the need for pensions to increase returns.

Notable Sales

MongoDB (MDB) and Snowflake (SNOW): Software stocks have generally been under pressure as corporate IT departments (and budgets) digest AI implications.

Shopify (SHOP): A recently announced plan to spend more on revenue growth projects extended the timeline for our investment thesis.

Veeva Systems (VEEV): We appreciate its long-term trajectory as a premier provider of health care software, but the company has been struggling with increased competition and general software weakness amid AI disruptions.

UnitedHealth (UNH): We sold the stock because the managed care weighting in the benchmark was reduced and because we are cautious about headline risk during the upcoming election season.

Top issuers (% of total net assets)

|

Fund |

Index |

|

|

Nvidia Corp (NVDA) |

11.40 |

10.34 |

|

Microsoft Corp (MSFT) |

9.96 |

11.71 |

|

Apple Inc (AAPL) |

7.24 |

10.82 |

|

Amazon.com Inc (AMZN) |

7.21 |

6.13 |

|

5.49 |

7.05 |

|

|

Meta Platforms Inc (META) |

4.05 |

3.93 |

|

Mastercard Inc (MA) |

3.10 |

1.29 |

|

Broadcom Inc (AVGO) |

2.54 |

2.44 |

|

Eli Lilly & Co (LLY) |

2.02 |

2.70 |

|

KKR & Co Inc (KKR) |

1.96 |

0.06 |

|

As of 06/30/24. Holdings are subject to change and are not buy/sell recommendations. |

||

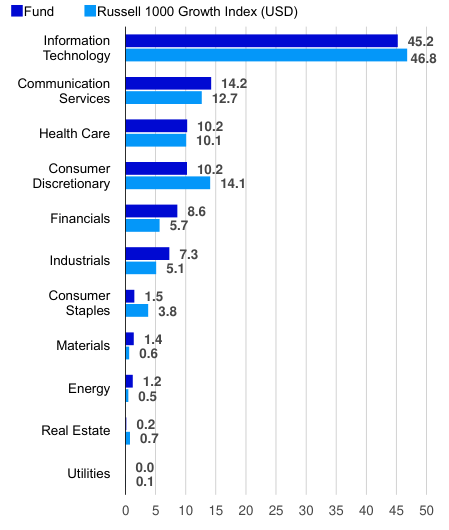

Sector breakdown (% of total net assets)

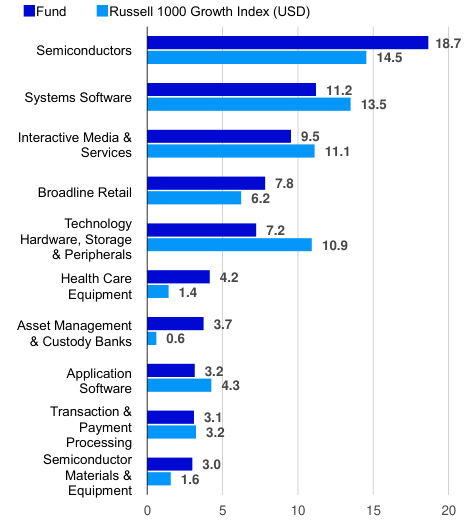

Top industries (% of total net assets)

Performance highlights

The fund had a positive return for the quarter but underperformed its benchmark, primarily due to stock selection in IT and communication services. Overweights in financials and industrials also hurt relative return, though the effects were offset by positive stock selection in these sectors.

Stock selection and an underweight in consumer discretionary added to relative return. An underweight in consumer staples and stock selection in health care were also beneficial.

Contributors to performance:

Nvidia completed a 10-for-1 stock split and surpassed $3 trillion in market cap. There is significant excitement for the launch of its Blackwell platform, which will likely power generative AI faster with less cost and energy consumption.

Apple: introduced Apple Intelligence, which is expected to transform what users can do with iPhones, iPads and Macs. Four years past the pandemic, we believe this is also a sweet spot for the handset upgrade cycle.

Alphabet issued its first ever quarterly dividend, widening its investor audience, and saw a surge in earnings and profits, resulting in a new all-time high stock price.

Microsoft unveiled a new category of Windows PCs called Copilot+ PCs, which are expected to have the most powerful Neural Processing Units (NPUs), up to 20x more powerful and up to 100x more efficient for running AI workloads.

Amazon.com reported continued strong ecommerce results that helped push its market cap over $2 trillion for the first time. Amazon’s stake in Rivian Automotive got a boost from an announced joint venture with Volkswagen.

Detractors from performance:

Mastercard was hurt by lower inflation, as its fees are a percentage of purchase amounts, and by an ongoing dispute about interchange or “swipe” fees charged between banks for processing credit card payments.

MongoDB suffered as software stocks took a backseat to AI-related stocks.

Advanced Micro Devices (AMD) issued a higher full year revenue outlook, but investors appeared to expect an even higher revision given increased demand for its Graphics Processing Units (GPUs) employed in AI data centers.

Airbus (OTCPK:EADSF) had to delay its airplane deliveries due to the inability of its supply chain to fully support increased production. We reduced the fund’s position despite a 10-year order backlog, pristine balance sheet and a wounded competitor.

DexCom (DXCM) declined as the stock of this continuous glucose monitoring device company experienced sentiment-driven moves. Investors appeared to worry the addition of sales team members would be disruptive. Additionally, we believe investors overreacted to another company’s positive results for a type 1 diabetes trial.

Top contributors (%)

|

Issuer |

Return |

Contrib. to return |

|

Nvidia Corporation |

36.74 |

3.46 |

|

Apple Inc. |

22.99 |

1.10 |

|

Alphabet Inc. |

20.60 |

0.97 |

|

Microsoft Corporation |

6.42 |

0.61 |

|

Amazon.com, Inc. |

7.13 |

0.50 |

Top detractors (%)

|

Issuer |

Return |

Contrib. to return |

|

Mastercard Incorporated |

-8.27 |

-0.34 |

|

MongoDB, Inc. |

-34.18 |

-0.33 |

|

Advanced Micro Devices, Inc. |

-10.13 |

-0.27 |

|

Airbus SE |

-24.13 |

-0.18 |

|

DexCom, Inc. |

-18.26 |

-0.16 |

Standardized performance (%) as of June 30, 2024

|

Quarter |

YTD |

1 Year |

3 Years |

5 Years |

10 Years |

Since inception |

||

|

Class P shares (MUTF:SMMIX) inception: 11/01/82 |

NAV |

6.21 |

21.70 |

30.71 |

2.91 |

14.52 |

13.47 |

10.28 |

|

Class A shares (MUTF:ASMMX) inception: 10/31/05 |

NAV |

6.15 |

21.60 |

30.50 |

2.75 |

14.35 |

13.30 |

10.37 |

|

Max. Load 5.5% |

0.30 |

14.92 |

23.35 |

0.83 |

13.06 |

12.66 |

10.03 |

|

|

Class R6 shares (MUTF:SMISX) inception: 04/04/17 |

NAV |

6.28 |

21.81 |

30.89 |

3.06 |

14.69 |

13.55 |

– |

|

Class Y shares (MUTF:ASMYX) inception: 10/03/08 |

NAV |

6.23 |

21.79 |

30.85 |

3.01 |

14.63 |

13.59 |

12.76 |

|

Russell 1000 Growth Index (‘USD’) |

8.33 |

20.70 |

33.48 |

11.28 |

19.34 |

16.33 |

– |

|

|

Total return ranking vs. Morningstar Large Growth category (Class P shares at NAV) |

– |

– |

48% (585 of 1167) |

82% (900 of 1097) |

61% (652 of 1024) |

54% (433 of 799) |

– |

|

Expense ratios per the current prospectus: Class P: Net: 0.85%, Total: 0.85%; Class A: Net: 1.00%, Total: 1.00%; Class R6: Net: 0.70%, Total: 0.70%; Class Y: Net: 0.75%, Total: 0.75%. Performance quoted is past performance and cannot guarantee comparable future results; current performance may be lower or higher. Visit Country Splash for the most recent month-end performance. Performance figures reflect reinvested distributions and changes in net asset value (NAV). Investment return and principal value will vary so that you may have a gain or a loss when you sell shares. Returns less than one year are cumulative; all others are annualized. Performance shown prior to the inception date of Class R6 shares is that of Class A shares and includes the 12b-1 fees applicable to Class A shares. Index source: RIMES Technologies Corp. Please keep in mind that high, double-digit returns are highly unusual and cannot be sustained. Had fees not been waived and/or expenses reimbursed in the past, returns would have been lower. Performance shown at NAV does not include the applicable front-end sales charge, which would have reduced the performance. Class P, Y and R6 shares have no sales charge; therefore, performance is at NAV. Class Y shares are available only to certain investors. Class R6 shares are closed to most investors. Please see the prospectus for more details. For more information, including prospectus and factsheet, please visit Invesco.com/SMMIX Not a Deposit Not FDIC Insured Not Guaranteed by the Bank May Lose Value Not Insured by any Federal Government Agency |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.