2d illustrations and photos

Key takeaways

- The fund underperformed its benchmark

- Class A shares underperformed the MSCI Emerging Markets Index. Stock selection in consumer staples, financials, real estate and industrials and overweights in consumer staples and real estate were among the largest detractors from relative performance for the quarter.

- Bottom-up stock selection focused on EQV (Earnings, Quality, Valuation) characteristics

- During the quarter, we initiated four new positions and sold two stocks based on our EQV fundamentals. Our actively managed, bottom-up stock selection drives the fund’s sector and country allocations.

- We remain focused on a long- term investment horizon

- Regardless of the macroeconomic environment, we remain focused on applying our well-established, long-term, bottom-up EQV investment process that seeks to identify attractively valued, high quality growth companies.

Manager perspective and outlook

Despite a notable decline in April, global equities had a positive return for the second quarter as investors appeared to continue anticipating central bank interest rates cuts. Some central banks, including the European Central Bank and the Bank of Canada, have started to ease monetary policy. Others have kept rates the same amid sticky inflation in the services sectors. In this environment, developed market equities performed well, primarily driven by US growth stocks, specifically stocks related to artificial intelligence (‘AI’). In contrast, value stocks led returns in the UK and Europe. French equities were weak due to apparent concerns about the outcome of the country’s snap election and this affected equity results in the European region. Emerging market equity returns were positive for the quarter, outperforming developed market equities, driven by equity gains in Taiwan and China.

Though global equities have continued to rise in some regions, we believe it is important to acknowledge that monetary policy have remained uncertain. Other potential risks include ongoing geopolitical tensions and elections around the globe, which may create market headwinds and may increase volatility. In this environment, we believe equity investors may focus on the type of high quality and traditional investment fundamentals that are central to the fund’s balanced EQV investment philosophy.

Portfolio positioning

During the quarter, we initiated the following positions:

Shenzhen Inovance Technology is a China-based leader in industrial automation products with market share gains in a structurally growing industry. The company has been a key beneficiary of domestic substitution for foreign brands. We believe its return on equity is attractive and it has a healthy balance sheet with negligible debt levels. The stock’s valuation has been appealing in part due to the automation industry’s recent weakness. However, we see signs that industry demand/growth rates are improving.

Bank Rakyat Indonesia (OTCPK:BKRKY) provides commercial banking services focused on lending and banking for micro, small and medium-sized enterprises in Indonesia. The company operates in the highly profitable and difficult to replicate micro lending. Indonesia has several structural tailwinds that we view as favorable for the banking industry, including attractive demographics and low credit penetration. In addition to a favorable macroeconomic backdrop, we believe Bank Rakyat could see significant improvement in quality. Management has been shifting its mix toward the highest return on equity/lowest non-performing micro loans.

Allegro.eu (OTCPK:ALEGF) is an ecommerce marketplace in Poland and Eastern Europe that we believe offers strong growth at an attractive valuation. The stock’s valuation has been held down by expectations that its private equity owners will continue to pressure the stock with further sell downs. We believe this pressure will eventually pass. In the meantime, Allegro’s market dominance has grown at a rapid clip.

MercadoLibre (MELI) is a leading ecommerce player in Latin America with large exposures in Brazil, Mexico and Argentina where it has continued to gain market share. We believe the company’s financial technology platform, logistics infrastructure and diversified product base are key competitive advantages. Scale improvement and growth in online advertising are potential tailwinds for profit margins. We sold the following stocks:

Yum China (YUMC) is the owner of KFC and Pizza Hut in China. We sold the position because rising competition has negatively affected sales growth and profit margin potential.

Telkom Indonesia is an Indonesian telecommunications company.

We trimmed positions in Mexico-based Kimberly-Clark de Mexico (OTCPK:KCDMF) and Bolsa Mexicana de Valores (OTCPK:BOMXF) due to increased political risk following Mexico’s election. Bolsa was also trimmed due to uncertainty regarding its new CEO.

Top issuers (% of total net assets)

|

Fund |

Index |

|

|

Taiwan Semiconductor Manufacturing Co Ltd (TSM) |

8.77 |

9.72 |

|

HDFC Bank Ltd (HDB) |

4.61 |

0.75 |

|

Samsung Electronics Co Ltd (OTCPK:SSNLF) |

4.19 |

4.25 |

|

Richter Gedeon Nyrt (OTCPK:RGEDF) |

4.00 |

0.05 |

|

Tencent Holdings Ltd (OTCPK:TCEHY) |

3.58 |

4.18 |

|

MediaTek Inc (OTCPK:MDTTF) |

3.37 |

0.87 |

|

Bank Central Asia Tbk PT (OTCPK:PBCRF) |

3.19 |

0.45 |

|

BDO Unibank Inc (OTCPK:BDOUF) |

3.13 |

0.07 |

|

Fuyao Glass Industry Group Co Ltd (OTCPK:FYGGY) |

2.97 |

0.06 |

|

Emaar Properties PJSC |

2.89 |

0.20 |

|

As of 06/30/24. Holdings are subject to change and are not buy/sell recommendations. |

||

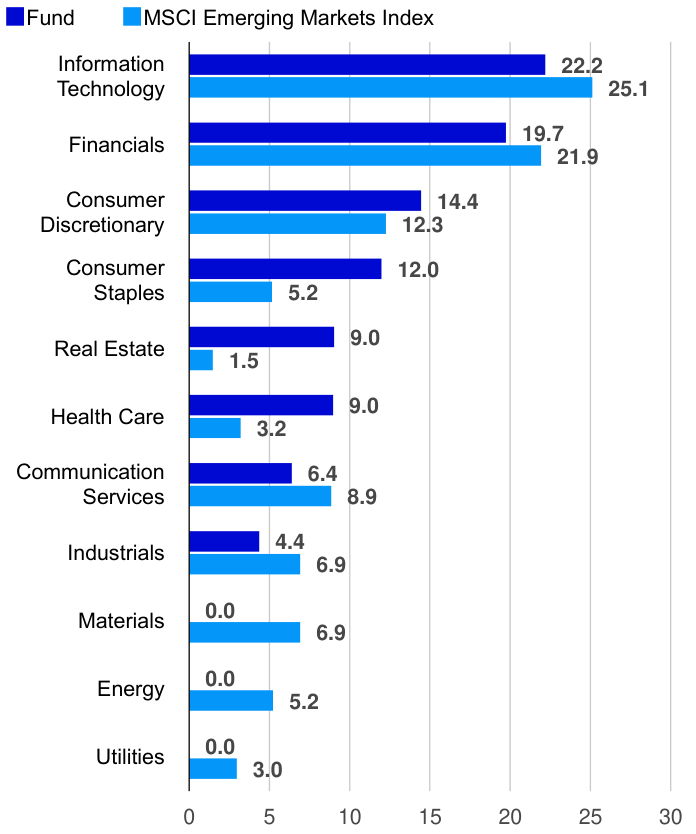

Sector breakdown(% of total net assets)

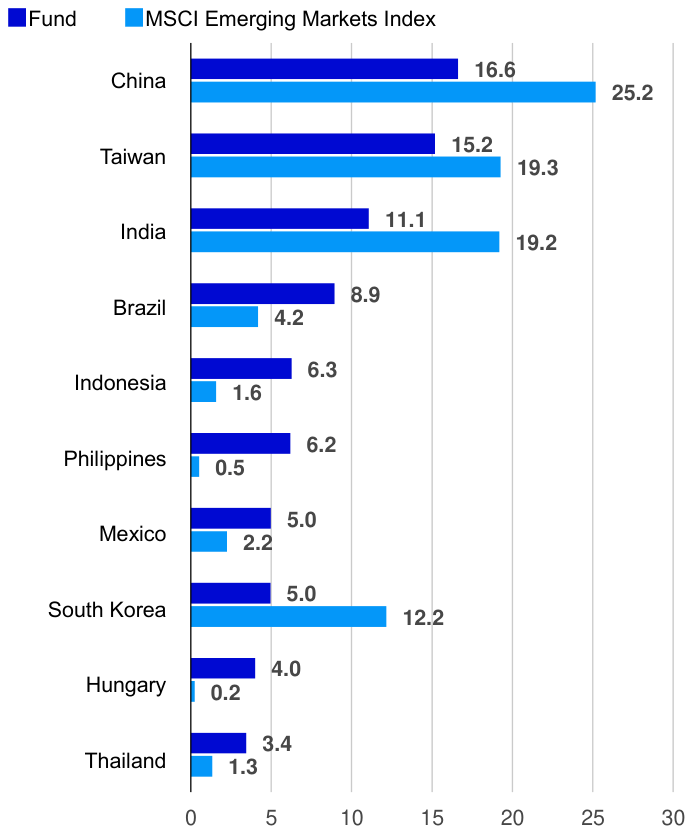

Top countries(% of total net assets)

Performance highlights

Having no exposure in materials and energy contributed to relative performance. Geographically, having no exposure in Saudi Arabia and an underweight in South Korea added to relative results. Fund holdings in India outperformed those of the benchmark index, adding to relative return.

Conversely, stock selection in consumer staples, financials, real estate and industrials were among the largest detractors from relative results. Overweights in consumer staples and real estate also hampered relative return. Geographically, stock selection in China, the Philippines and Mexico detracted from relative performance. Overweights in the Philippines, Mexico and Brazil negatively affected relative results.

Contributors to performance

Below are the largest contributors to absolute return for the quarter:

Taiwan Semiconductor’s technology roadmap and financial performance have remained strong, and the company has continued to benefit from increased AI demand and a better pricing outlook.

Emami (EQMNY) is an India-based fast-moving consumer goods (FMCG) company that focuses on Indian-centric products (e.g., cooling oil). Demand for fast moving consumer goods in rural India has started to recover and grow faster than in urban India, which helped Emami post solid volume growth in the most recent quarter after a period of disappointing results.

Tencent’s newer online advertising products have boosted growth and market share, while the outlook for online games may improve given its solid pipeline. Profit margins have risen faster than expected as the company focuses on higher value revenue streams.

Detractors from performance

Below are the largest detractors from absolute return for the quarter:

BDO Unibank (BDO) is a large Philippine bank that reported weak first quarter results with higher-than-expected costs. Additionally, BDO often trades as a proxy for the Philippines equity market, which was hampered by a weaker currency. However, we continue to like BDO for its dominant market position in the Philippines and are encouraged by its improving loan growth.

Tongcheng Travel (OTCPK:TNGCF) is an online travel agency in China that focuses on domestic and lower tier cities. The stock corrected after first quarter earnings were weaker than expected due to temporary margin pressure from investments in new business. We trimmed the fund’s holdings to control position size, but we still like the company’s long-term fundamentals.

Kimberly-Clark de Mexico (OTCPK:KCDMF) manufactures a wide array of paper-based products such as diapers, bathroom and facial tissues, napkins, etc. Overall fundamentals have remained solid with the company posting strong margin improvement in the first quarter. However, the broad sell-off in Mexico’s equity market following presidential and congressional elections in June led to a decline in the share price.

Top contributors (%)

|

Issuer |

Return |

Contrib. to return |

|

Taiwan Semiconductor Manufacturing Company Limited |

22.80 |

1.54 |

|

Emami Limited |

60.70 |

0.78 |

|

Tencent Holdings Limited |

23.94 |

0.69 |

|

HDFC Bank Ltd. |

16.16 |

0.64 |

|

Fuyao Glass Industry Group Co., Ltd. |

19.06 |

0.54 |

Top detractors (%)

|

Issuer |

Return |

Contrib. to return |

|

BDO Unibank, Inc. |

-19.84 |

-0.74 |

|

Tongcheng Travel Holdings Limited. |

-23.57 |

-0.69 |

|

Kimberly-Clark de Mexico S.A.B. de C.V. |

-24.52 |

-0.59 |

|

China Resources Beer (Holdings) Co. Ltd. (OTCPK:CRHKY) |

-25.56 |

-0.54 |

|

Multiplan Empreendimentos Imobiliarios S.A (OTCPK:MLTTY) |

-19.31 |

-0.53 |

Standardized performance (%) as of June 30, 2024

|

Quarter |

YTD |

1 Year |

3 Years |

5 Years |

10 Years |

Since inception |

||

|

Class A shares (MUTF:GTDDX) inception: 01/11/94 |

NAV |

-2.05 |

-2.40 |

-3.43 |

-7.79 |

0.98 |

1.36 |

4.60 |

|

Max. Load 5.5% |

-7.43 |

-7.77 |

-8.74 |

-9.51 |

-0.16 |

0.79 |

4.41 |

|

|

Class R6 shares (MUTF:GTDFX) inception: 09/24/12 |

NAV |

-1.97 |

-2.23 |

-3.05 |

-7.44 |

1.37 |

1.76 |

2.32 |

|

Class Y shares (MUTF:GTDYX) inception: 10/03/08 |

NAV |

-2.02 |

-2.31 |

-3.20 |

-7.56 |

1.23 |

1.61 |

5.32 |

|

MSCI Emerging Markets Index |

5.00 |

7.49 |

12.55 |

-5.07 |

3.10 |

2.79 |

– |

|

|

Total return ranking vs. Morningstar Diversified Emerging Mkts category (Class A shares at NAV) |

– |

– |

100% (797 of 803) |

77% (505 of 717) |

86% (535 of 645) |

82% (337 of 424) |

– |

|

Expense ratios per the current prospectus: Class A: Net: 1.34%, Total: 1.35%; Class R6: Net: 0.97%, Total: 0.98%; Class Y: Net: 1.09%, Total: 1.10%. Performance quoted is past performance and cannot guarantee comparable future results; current performance may be lower or higher. Visit invesco.com for the most recent month-end performance. Performance figures reflect reinvested distributions and changes in net asset value (NAV). Investment return and principal value will vary so that you may have a gain or a loss when you sell shares. Returns less than one year are cumulative; all others are annualized. On Oct. 31, 1997, the fund reorganized from a closed-end fund to an open-end fund. Returns through that date are the closed-end fund’s historical performance. Returns since that date are those of the open-end fund. Fees and expenses of the open-end fund differ from those of the closed-end fund. Index source: RIMES Technologies Corp. Had fees not been waived and/or expenses reimbursed in the past, returns would have been lower. Performance shown at NAV does not include the applicable front-end sales charge, which would have reduced the performance. Class Y and R6 shares have no sales charge; therefore performance is at NAV. Class Y shares are available only to certain investors. Class R6 shares are closed to most investors. Please see the prospectus for more details. |