Bloom Energy (BE 6.53%) is a clean energy company that has recently experienced massive, explosive growth. And by growth, I mean a 1,480% surge in stock value over the past year, with first-quarter year-over-year revenue growth of 130%.

Today’s Change

(-6.53%) $-19.82

Current Price

$283.59

Key Data Points

Market Cap

$86B

Day’s Range

$275.42 – $288.50

52wk Range

$17.01 – $310.00

Volume

261K

Avg Vol

10M

Gross Margin

31.08%

What kind of fertilizer has Bloom been using? The same kind that the most explosive chip stocks have been thriving off of: the development of artificial intelligence (AI). Indeed, if chip companies are supplying AI’s brains, then Bloom is supplying the calories those brains need to think. Due to strong demand for its solid oxide fuel cell systems, Bloom management raised its full 2026 outlook to $3.4 billion to $3.8 billion, representing an 80% jump from 2025 levels.

With a 15.8-fold gain within a year, is Bloom stock now a buy, sell, or hold?

Bloom is thriving, but its valuation is something to watch

If you haven’t bought Bloom Energy yet, I would only buy a small starter position at today’s share price of $303.

The reason isn’t that the business is weak. Far from it: The company has partnered with huge players in the AI data center arena, with an enviable $5 billion strategic partnership with Brookfield Asset Management (BAM 2.51%) to deploy its technology for AI infrastructure.

Image source: Bloom Energy.

The problem, however, is Bloom’s valuation. Today, it trades at about 128 times forward earnings and 80 times book value. Translation: A lot of the good news is already baked into the stock price. The average price target for Bloom is about $237, a nearly 22% downside from today’s $303.

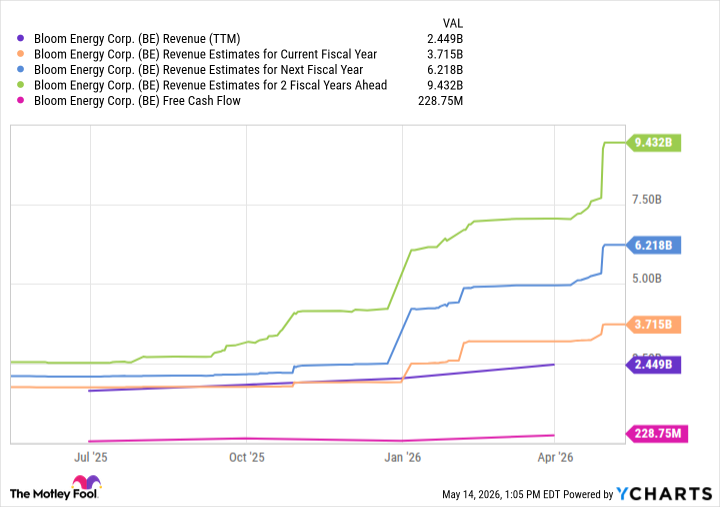

The clean energy stock already carries an $86 billion market cap, which is about 24 times the midpoint of its 2026 revenue guidance ($3.6 billion). Revenue is expected to nearly double between this year and next, but even that doesn’t justify a valuation this stretched. Indeed, at today’s valuation, Bloom currently trades at about 376 times its trailing free cash flow.

Data by YCharts.

On the contrary, if you’re currently invested in Bloom, hold on tight. AI data centers are going to need more power than the U.S. grid can deliver, and Bloom is one of the few companies that has a deployable product to help make up the difference. It trades at a premium, but over a long period, it could start to grow into its valuation.

Perhaps the best strategy right now would be to dollar-cost average. This entails gradually buying shares rather than investing a large sum all at once. The advantage is that it lets you gain exposure to Bloom’s long-term opportunity without betting too heavily at today’s valuation.