olm26250

Executive Summary

Selective Insurance Group, Inc. (NASDAQ:SIGI) operates as a super-regional property and casualty carrier, with three main segments: personal lines, commercial lines, and excess and surplus insurance business.

Q1 2024 Investor Presentation – Selective Insurance

In 2023, Selective Insurance Group maintained steady performance in its non-life insurance business, achieving post-tax earnings of $365 million, a notable increase from approximately $225 million recorded in 2022.

Despite experiencing double-digit growth in net written premiums, the underwriting performance declined due to inflationary pressures. However, this was partially offset by implemented rate changes that began to take effect.

Selective Insurance Group also benefited from favorable investment conditions, resulting in steady investment income totaling $309 million post-tax. This increase in investment income, compared to $232 million in 2022, was driven by higher interest rates, active portfolio management, and effective deployment of operating and investing cash flow.

The company recently released its second-quarter results and significantly downgraded its FY2024 guidance by lowering the underwriting margin by 5 points. The downgrade of the 2024 guidance resulted from weaker underwriting performance, fueled by adverse prior years’ claims development in the commercial lines and deterioration in the personal lines’ underwriting performance.

On the positive side, the excess and surplus lines have shown improved underwriting margins, coupled with strong double-digit growth. Following the second-quarter results release, the stock price declined by approximately 17% the day after the results were announced, as analysts and investors were disappointed by the poor underwriting performance and the downgrade of the FY2024 guidance.

Company Performance & Outlook

The insurance industry has faced significant challenges over the past five years, marked by the impact of the COVID-19 pandemic and a resurgence of claims inflation.

Following the pandemic period from 2019 to 2021, insurers grappled with increased economic and social inflation, alongside volatility in financial markets. Despite these obstacles, Selective Insurance Group has displayed resilience and stability. On average over the past six years, the company’s combined ratio stood at 94.7%.

| 2023 | 2022 | 2021 | 2020 | 2019 | 2018 | |

| E&S Lines | 86.0% | 90.9% | 94.3% | 99.9% | 95.9% | 100.3% |

| Commercial Lines | 94.9% | 94.8% | 91.9% | 92.9% | 92.9% | 94.3% |

| Personal Lines | 121.7% | 102.4% | 98.6% | 105.2% | 97.3% | 95.8% |

| Total | 96.5% | 95.1% | 92.8% | 94.9% | 93.7% | 95.0% |

Figures based on annual reports

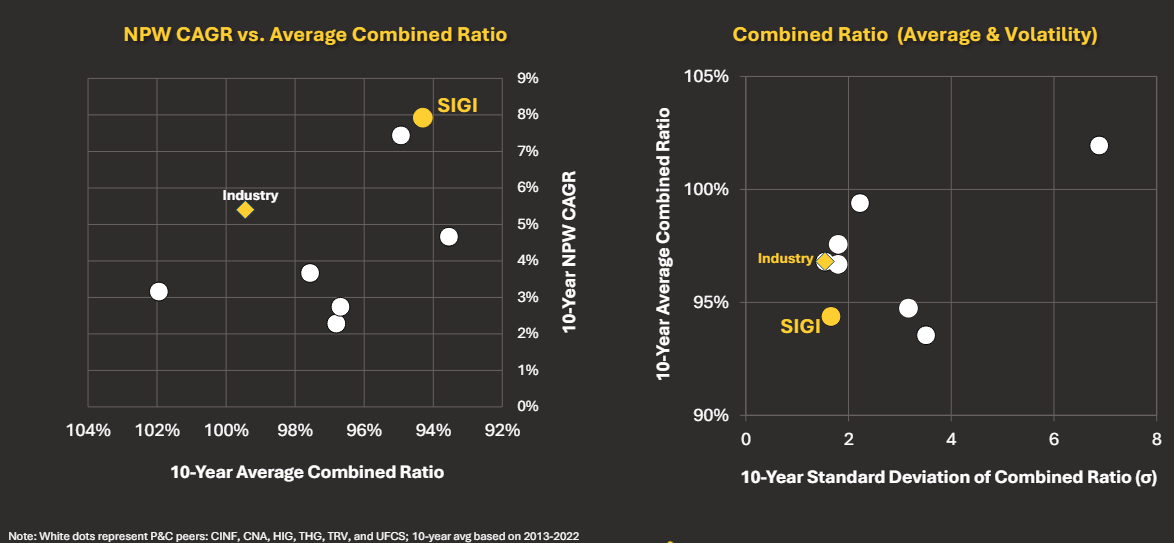

In addition, Selective Insurance Group has demonstrated superior underwriting performance compared to many of its peers over the past decade.

Q1 2024 Investor Presentation – Selective Insurance

This resilience primarily stems from the consistent performance of its commercial and Excess and Surplus (E&S) insurance segments. However, the personal segment has faced challenges due to recent inflationary pressures, intense market competition, and the impact of catastrophic events over the same period.

Nonetheless, investors seem to have overlooked the overperformance of Selective Insurance. Are they right? Potentially. First things first, people who are willing to invest in any property and casualty insurance carriers should keep in mind two interlinked factors: the underwriting performance of a non-life insurance company is linked to the underwriting and pricing processes implemented in the company.

An insurance company can underwrite “bad” risks or sell policies to “bad” profiles, but it must do so at a fair price to cover future claims and associated expenses to generate underwriting profits over the cycle. Secondly, an insurance company relies on reserving actuaries to estimate the ultimate claims costs that will be paid and, therefore, the amount of reserves that need to be carried.

An adverse run-off is not necessarily a sign of a poor underwriting process; it can be indicative of an overly aggressive reserving estimation. The amount of reserves carried by an insurance company is under the responsibility of the reserving actuaries. Hence, the adverse run-off recorded during the second quarter indicates that the reserves were insufficient to cover future claims. Does this mean that the reserving actuaries failed to perform their analysis? Not necessarily, and I don’t want to blame them. It is possible that a change in the claims trend was not observed in the prior data and has subsequently affected the prior years’ claims trend.

As mentioned during the second quarter results call, the $176 million adverse run-off was mostly related to the general liability line of business. Ninety percent of this quarter’s general liability action is related to accident years 2020 through 2023.

Consequently, the insurer decided to take further actions to improve the general liability line of business. In the second quarter, the general liability renewal pure price increased to 7.6%. This was 110 basis points higher than the first quarter of 6.5% and 220 basis points above full-year 2023’s 5.4%. The insurance carrier expects that general liability pricing will further increase in the second half of the year, although no further details were shared during the conference call.

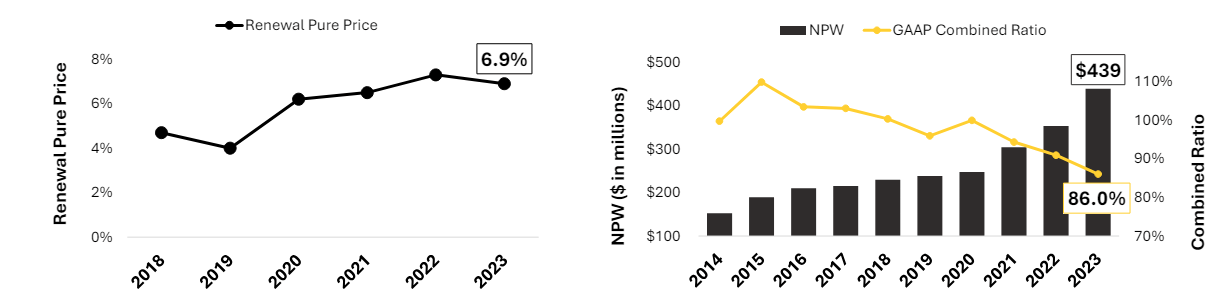

Despite the adverse performance of the commercial and personal insurance segments for the first six months of the year, the excess and surplus insurance business has continued to be a success story in terms of business growth. From 2014 to 2023, the segment’s turnover more than tripled, while its underwriting performance entered positive territory in 2019, with the combined ratio steadily decreasing over the years.

Q1 2024 Investor Presentation – Selective Insurance

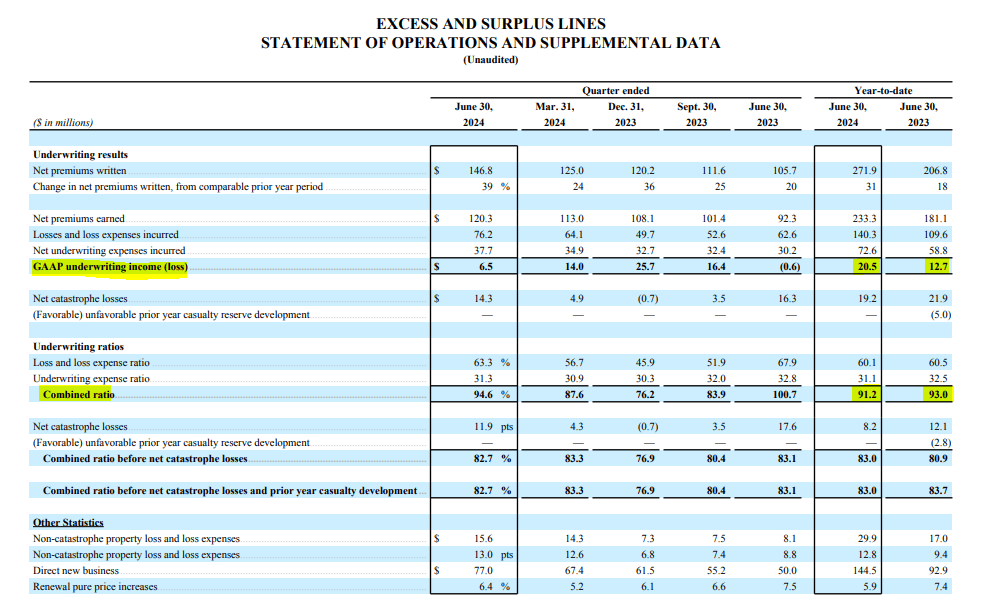

In Q2 2024, the underwriting performance of the excess and surplus line of business improved compared to the same period one year ago. The combined ratio dropped by 6.1 points to 94.6%. Consequently, the year-to-date combined ratio decreased by 1.8 points to 91.2%. Additionally, the six-month underwriting income nearly doubled, rising from $12.7 million to $20.5 million.

Q2 2024 Press Release Supplement – Selective Insurance

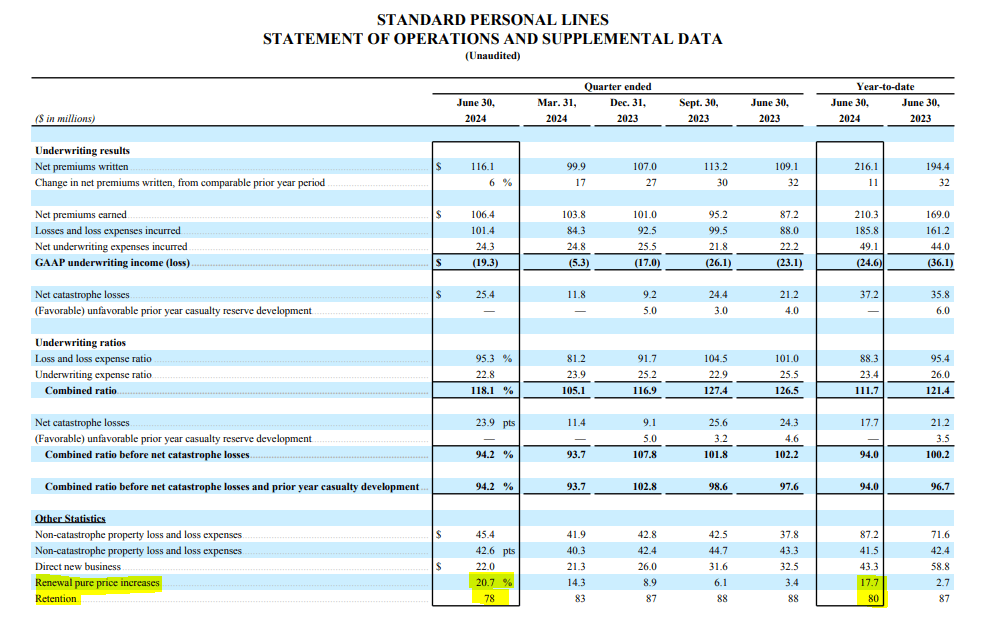

Unfortunately, the steady performance of the excess and surplus insurance business is insufficient in 2024 to offset the losses from the personal and commercial lines of business. As mentioned above, the commercial lines of business suffered from the revision of the prior year’s ultimate amount. Over the prior years, the company also encountered challenges in its personal lines segment, marked by a notable rise in claims and losses attributed to adverse weather events.

In response, the company implemented price rate changes ranging from 20 to 25% to address the underperforming portfolios. Renewal pure price increase during the second quarter of 2024 was 20.7%, while the retention rate dropped to 78%. On a year-to-date basis, the renewal pure price increase was 17.7%, with a retention rate of 80%, which is 7 points lower compared to the same period last year.

Q2 2024 Press Release Supplement – Selective Insurance

In other words, some clients decided not to accept the price increases proposed by Selective Insurance’s agents.

Although the company may have been affected by adverse selection (i.e., situations in which an applicant’s actual risk is substantially higher than the risk known by the insurance company, causing the company to offer coverage at a cost that does not accurately reflect its actual risk exposure), the underwriting and pricing measures implemented since 2023 have helped reduce underwriting losses. On a year-to-date basis, underwriting losses decreased by nearly $12 million to -$24.6 million. While Selective Insurance’s personal segment is still far from reaching the break-even point, there are hopes that losses from this segment will significantly decrease by the end of 2024.

Looking ahead, Selective Insurance Group may continue to face challenges, particularly with inflation and catastrophe losses. Although inflationary pressures might gradually ease, they are expected to persist and impact both revenues and expenses in the short term. Following the weaker-than-expected underwriting performance observed during the second quarter, the company’s management downgraded the FY2024 guidance.

Initially, the FY2024 combined ratio guidance was 95.5% and then surged to 96.5%. However, it is now expected to land at around 101.5%, indicating a negative underwriting performance. The 5-point increase from the prior guidance (96.5%) reflects the full-year impact of adverse prior-year casualty reserve development, current accident year bookings in general liability, and a 0.5-point increase in catastrophe loss assumptions, now at 5.5 points. The company’s estimate for $360 million of after-tax net investment income, including $32 million from alternative investments, remains unchanged.

Based on an expected full-year earned premium amount of $4.3 billion (adjusted from a 13% change in FY2023 Net Earned Premiums), a combined ratio of 101.5%, a 21% tax rate, and $360 million post-tax investment income, the net income available to common shareholders is estimated to be approximately $226 million, down from a prior estimation of around $409 million.

FY2024 Guidance and Author’s Calculation

The company’s net income will be significantly affected by the overall underwriting performance. A 1%-point reduction in the combined ratio would decrease the pre-tax underwriting loss by $43 million.

Company’s Valuation

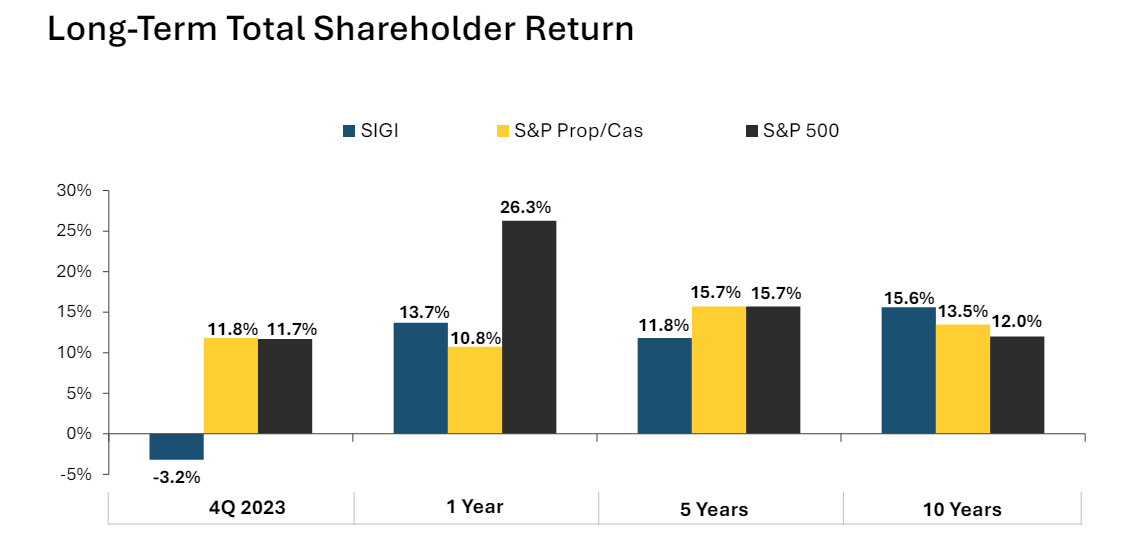

Selective Insurance Group’s stock price has enjoyed a consistent upward trajectory in recent years, reflecting the company’s strong performance in underwriting, premium volume growth, and stability in investment income.

Q1 2024 Investor Presentation – Selective Insurance

This success has translated into dividend growth over time, rewarding patient shareholders who have placed their trust in Selective Insurance’s business strategy and underwriting discipline.

Over the past five years, the market has typically valued Selective Insurance at approximately 1.9 -2.0 times its book value.

With the current book value per share standing at $44.74, this suggests a fair value for the company of around $85 to $89 per share, or an intrinsic value of $5.2 to $5.5 billion based on a weighted average share count of 61.5 million on a fully diluted basis.

Another method of valuing Selective Insurance involves considering its earnings and the multiple investors are willing to pay to acquire the insurance carrier. Based on the 5-year mean and median, investors are willing to acquire Selective Insurance for around 17.6 times its earnings.

Currently, the PE ratio is above 24, as the earnings dropped significantly due to the underwriting losses recorded during the second quarter. Assuming a valuation multiple of 17.6 times earnings is fair and using the expected FY2024 net income of $226 million as a basis, Selective Insurance could be valued at around $4.0 billion by the end of 2024. In contrast, the market value is currently around $5.5 billion.

Considering various valuation metrics, it appears that the market seems to be optimistic about the recovery of the company.

Conclusion

Selective Insurance Group, Inc. remains a resilient player in the P&C insurance industry, with stable revenue growth and a robust balance sheet. However, its underwriting performance has deteriorated due to insufficient prior-year reserves and inflationary pressures. Given the current lack of a safety margin, Selective Insurance may not be the most attractive investment option at present.

Nevertheless, I am not overly bearish on the company, as current and ongoing underwriting measures have the potential to improve performance and mitigate the losses observed in the first six months of the year. Therefore, the current recommendation for Selective Insurance Group is to maintain a “hold” position.