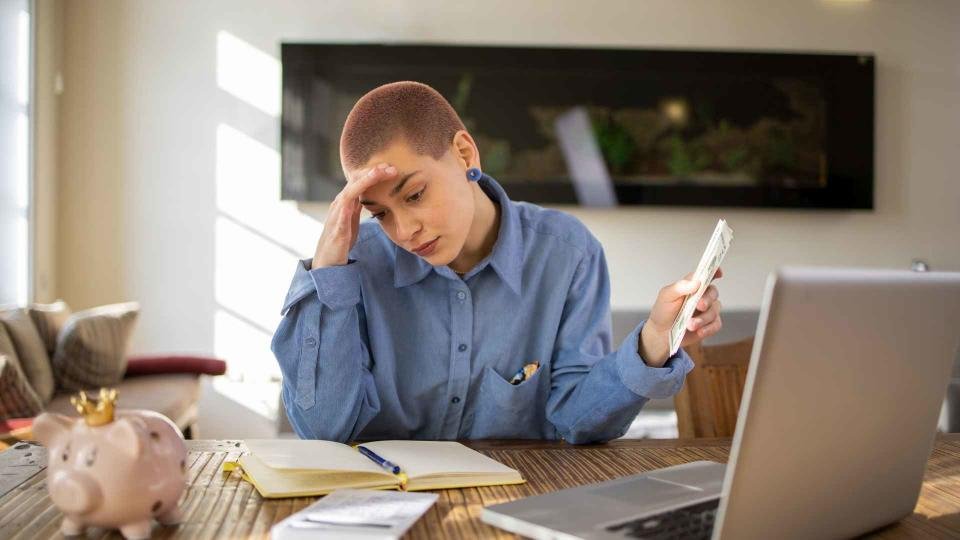

Sometimes, financial goals can appear to be at odds with each other, such as when you need to pay down high-interest debt and also save for an emergency fund. It’s easy to focus on one and not the other or try to knock them both out ineffectively.

Find Out: 9 Things the Middle Class Should Consider Downsizing To Save on Monthly Expenses

Try This: 7 Reasons You Must Speak To a Financial Advisor To Boost Your Savings in 2024

While it’s always a good idea to get out of debt, Annie Cole, money coach, founder of Money Essentials for Women and author of the book “101 Ways to Earn More, Build Wealth, and Live Rich in Your 30s,” said that it’s more than possible to do both, but it does take some intention and strategy.

She recommended the following steps.

Also, here are five debt myths no one should believe anymore.

Earning passive income doesn’t need to be difficult. You can start this week.

Start From Scratch

Cole recommended an approach she called “powerful” if you’re willing to do it.

“Instead of looking at your budget, your current income and then trying to squeeze in the debt and squeeze in the emergency savings, sometimes it’s really powerful to just start completely from scratch,” she said.

She has her clients write out all of their debts, all of the minimum payments and then on top of that, whatever they have in their savings account to do “a full audit.”

“From there we built a budget on top of that,” she said.

With one client, she said, “We actually started with those numbers and then built around it, which I think puts you in a different headspace. You’re still going to have to cut out expenses, but it makes it a little bit easier.”

Learn More: Warren Buffett: 10 Things Poor People Waste Money On

Something Over Nothing

Once you’ve listed all of your debts and their minimum payments, she said now you have some flexibility in approaching building up your emergency fund, which should be between three and six months’ worth of income, ideally. If you’re not in a position to put away something sizable, say $1,000 per month, she said, you probably can put away something like $200 per month (or whatever numbers work for you).

“Leaning into something is better than nothing. Progress is so important. And if you have $500 and then you get a flat tire, but you can fix it, well thank goodness you did that.”

Play a Mental Game

For her own part, Cole was able to fast-track some retirement savings by playing a mental game with herself.

“One day I was sitting down and I said, well, I know I could retire at this point, but I probably couldn’t retire sooner. What would it look like if I had to retire? You just come up with creative ideas.”

She encourages clients to envision how they’ll feel when they’ve met their goals as a way to motivate themselves to stay on track.

Budgeting Is Like Building a Muscle

Cole acknowledged that it can be hard to stick to a budget at first because it may feel “a little unnatural,” but the more you can stick to it the easier it will become.

“It’s just building up a new muscle to do all of those things on your list as a habit rather than having to try hard at it.”

Let Automatic Transfers Work For You

A great way to make sure you’re either saving regularly or making regular payments on your debt is to automate these transactions.

“If you set up automatic payments to go out, let’s say your paycheck hits your account and automatic payments go out to your debt first, that’s just going to become habitualized. And same with your emergency fund. If you can do that through your bank, you could set up an automatic transfer so that every time a certain amount hits your account, $25 goes off to another savings account.”

She believes it’s OK to have multiple goals.

“Think of it as one whole plan and little pieces of the puzzle are just working towards that one big goal of your finances.”

Allow a Little Wiggle Room

Though budgeting may need to be stringent for folks with a high amount of debt, Cole doesn’t tell her clients that they can’t ever budget for a want.

“I think that’s also why building the habit is so important,” she said.

A clear budget, with solid habits built in, means you can splurge every once in a while without guilt on small things.

Find Joy Without Spending

That said, Cole is a big advocate of trying to create joy in your life without spending.

“I think a lot of people sometimes spend to try to find joy. So for example, if you don’t like your job or if you’re just feeling stressed out, sometimes you spend to try to feel better.”

Instead, she recommended spending more time with friends, finding a hobby you love or doing something that brings you joy.

“I find that that can actually help reduce that need to feel like you need to go spend.”

Negotiate Some Expenses

Cole also recommended that you not take every bill or payment for granted, because many bills, such as internet, cellphone and insurance can be negotiated, or you could find other service providers who offer a better rate.

You can even find cheaper places to buy your groceries. Those fixed numbers in your head might actually be flexible or have an alternative. Even as little as $20 in savings here and there could add up to money that you can put toward your financial goals, she said.

Swap Rather Than Cut

Before you start cutting and feeling deprived, Cole suggested looking for ways to swap the pricier or paid thing for a free or lower-cost one.

“So for example, you love going to the gym, but you also want to get in more social time. Maybe you commit to walking with your partner every day. So I think there can be some creativity there so you don’t feel like you’re just getting things up,” she said.

Increase Primary Income Before Adding a Side Hustle

While side hustles can potentially be a good way to increase your income, thus having more to pay down on debt or put into savings, Cole suggested you focus on increasing your primary income stream before adding a side hustle.

“If you’re taking a bunch of surveys or driving for Uber and you’re making $10 an hour, that’s never going to really help you out versus a job pivot, going back to school, asking for that raise, getting in line from promotion and those things are really going to move the needle on your big income.”

If you do pursue a side hustle, she said, lean into things that really play up your existing talents and are worth your time and money.

There are as many ways to achieve financial goals as there are people pursuing them. Be creative but habitual, chipping away at your goals in small amounts until they add up to big wins.

More From GOBankingRates

This article originally appeared on GOBankingRates.com: Here’s How To Build an Emergency Fund and Pay Off High-Interest Debt