andyKRAKOVSKI/iStock via Getty Images

Performance Assessment

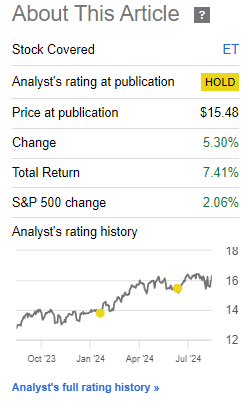

In my latest article on Energy Transfer (NYSE:ET), I had issued a ‘Neutral/Hold’ rating to reflect my views of performance in-line with the S&P 500 (SPY) (SPX):

Performance since Author’s Last Article on Energy Transfer (Seeking Alpha, Author’s Last Article on Energy Transfer)

Since then, ET has outperformed the S&P 500 by +5.35%, so one may argue that it has been a little bit of a missed opportunity. However, I am not too bothered by this omission (not buying) decision, as I still believe there would be more chances to load up at more opportune times.

Thesis Update

After Q2 FY24 results, what is becoming more clear is Energy Transfer’s increased foothold in capturing increased energy needs. I believe the key drivers of the ET stock are the following:

- Energy Transfer is well-poised to benefit from increased electricity demand

- Valuations are at a premium to its historical multiples, but at a discount vs peers

- A technical correction and a sharp rebound would provide a better entry for fresh buys

- Prediction markets’ views of the US Presidential election is a key monitorable

Energy Transfer is well-poised to benefit from increased electricity demand

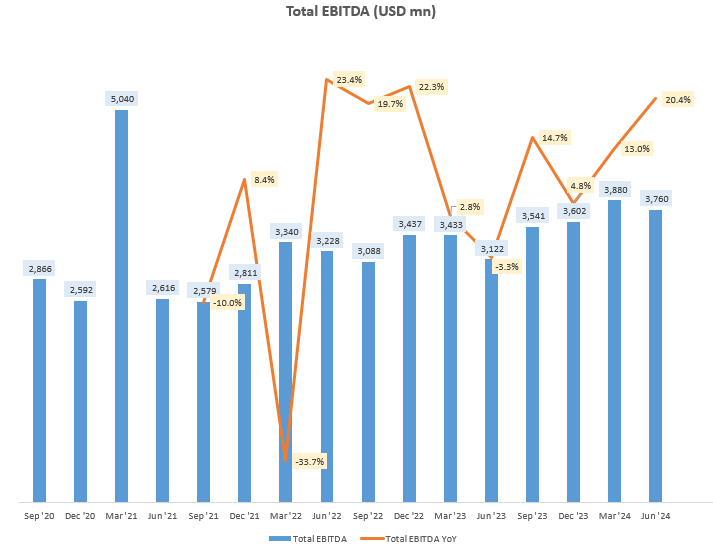

Energy Transfer’s total EBITDA is growing at a healthy clip of mid-high teens YoY:

Total EBITDA (USD mn) (Company Filings, Author’s Analysis)

Now, not all of this growth is organic as the company has completed some bolt-on acquisitions such as Crestwood, WTG Midstream and Lotus Midstream. In my last article, I made a case for why I believe these M&A deals are quite prudent since the transaction multiples paid are below sectoral median transaction multiples. In other words, the management of Energy Transfer have my vote of confidence in capital allocation decisions. This is important because according to the latest earnings call, further M&A is still expected, particularly in midstream O&G. I view this as a positive sign that is in-line with Energy Transfer’s strategy to steadily expand their transportation footprint in natural gas in response to growing energy needs:

With forecast for electricity demand growth becoming increasingly bullish and the need for grid reliability becoming progressively more important, it is clear that natural gas will play a significant role in helping meet this demand… Given Energy Transfer’s extensive interstate and intrastate natural gas pipeline footprint, we believe we are extremely well positioned to benefit from the anticipated rise in natural gas needs.

– Co-CEO Thomas Long in the Q2 FY24 earnings call

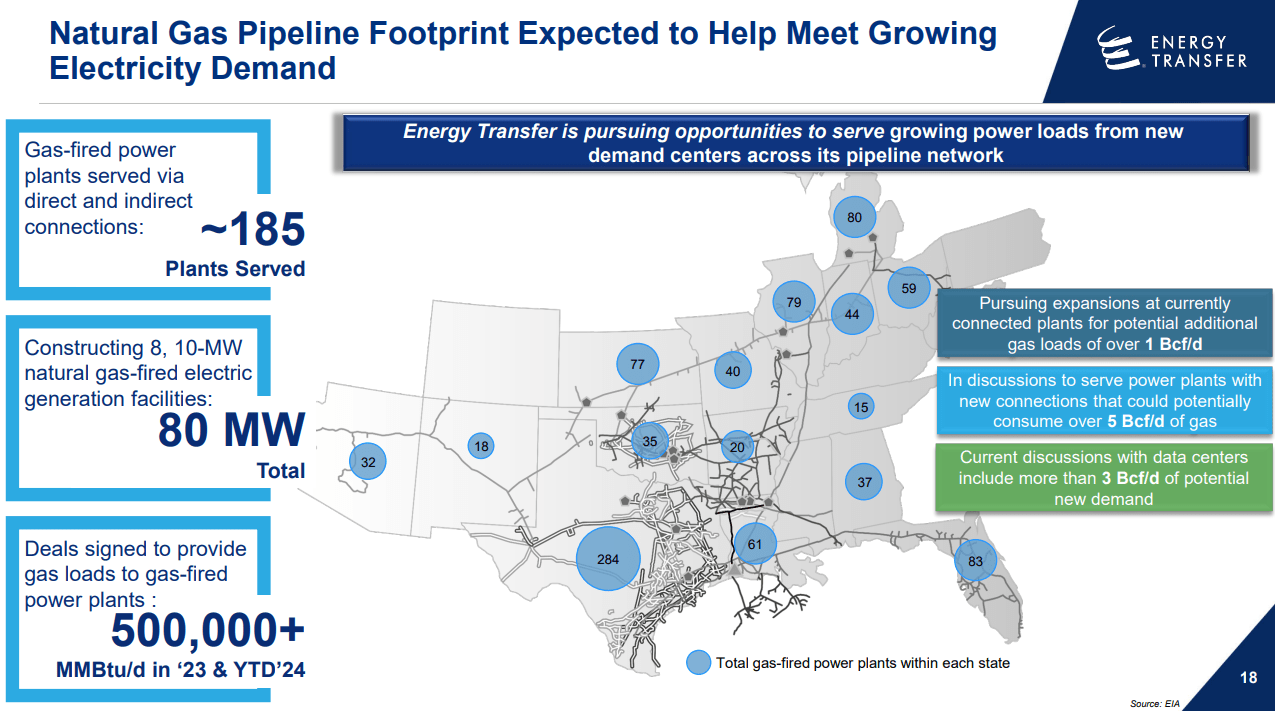

Energy Transfer’s Positioning To Meet Growing Electricity Demand (Energy Transfer Q2 FY24 Investor Presentation)

Much of the increased electricity generation and transmission demand is coming from data centers in response to a need for more computing resources. Energy Transfer is currently well-poised to capture this opportunity:

Yes, we’re in 4 or 5 different states, in discussions with multiple data centers of different sizes…it’s an enormous opportunity for us.

– Co-CEO Thomas Long in the Q2 FY24 earnings call

Valuations are at a premium to its historical multiples, but at a discount vs peers

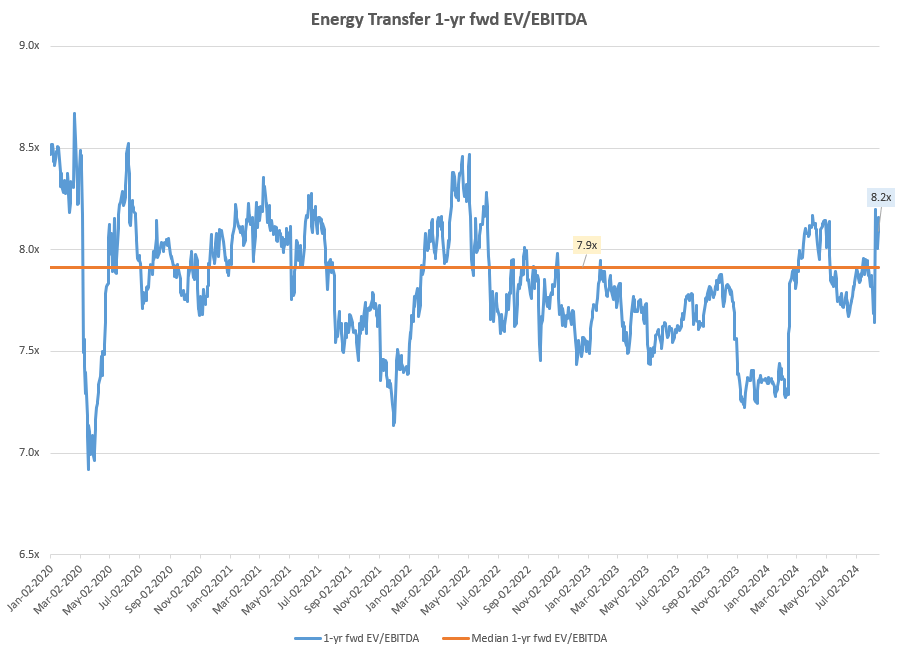

Energy Transfer stock has generally traded in a well-defined 1-yr fwd EV/EBITDA trading range from around 7.25x to 8.5x, making it easier to more clearly identify compelling attractive entry points from a valuation perspective.

Energy Transfer 1-yr fwd EV/EBITDA (Capital IQ, Author’s Analysis)

Currently, ET trades at a 1-yr fwd EV/EBITDA of 8.2x, which corresponds to a small 3.1% premium to the longer term median level of 7.9x. Of course, some premium vs historical levels may be warranted due to the growth drivers outlined in the previous section. However, I think there may be a chance for a better valuation for entries once the technicals picture is considered later below.

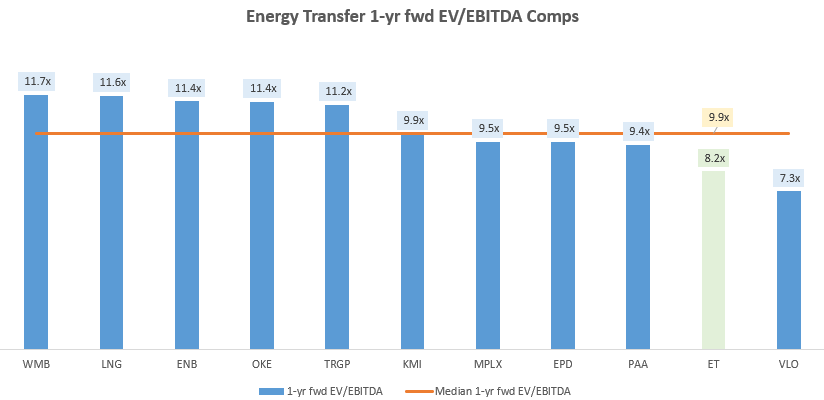

On a comparable valuations basis, ET’s valuation looks more attractive as it trades at a modest 17.5% discount to the median 9.9x among its peers:

Energy Transfer 1-yr fwd EV/EBITDA Comps (Capital IQ, Author’s Analysis)

Besides ET, the peerset includes Cheniere Energy (LNG), Enbridge (ENB), ONEOK (OKE), Targa Resources (TRGP), Kinder Morgan (KMI), MPLX LP (MPLX), Enterprise Products Partners (EPD), Plains All American Pipeline (PAA) and Valero Energy (VLO).

Overall, I prefer to weigh the absolute historical range multiples more in this case as I expect some mean reversion to occur there, which may well lead to a sectoral mean reversion as well.

A technical correction and sharp rebound would provide a better entry for fresh buys

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do. All my charts reflect total shareholder return as they are adjusted for dividends/distributions.

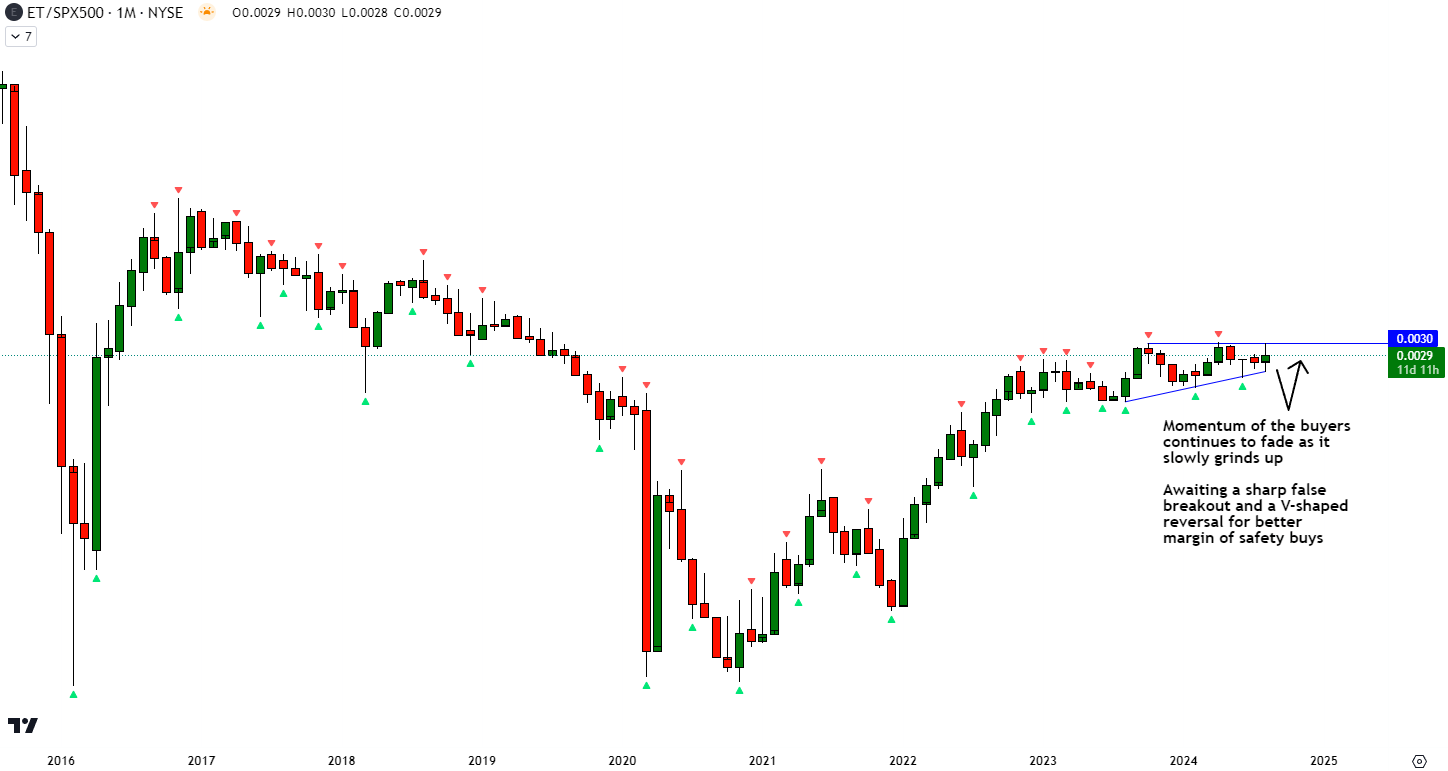

Relative Read of ET vs SPX 500

ET vs SPX 500 Technical Analysis (TradingView, Author’s Analysis)

For multiple months now, the relative chart of ET vs S&P 500 has been in an ascending triangle formation, with decreasing volatility. In such situations, I think it is prudent to wait for an initial false break and sharp rebound, as that often signals the direction of the formation’s breakout. In this case, as I lean bullish fundamentally, I am ideally awaiting a sharp, false breakout to the downside followed by V-shaped reversal to initiate fresh buys. This would give me the best chance for capturing a sustained outperformance leg vs the S&P 500.

Prediction markets’ views of the US Presidential election is a key monitorable

It may be possible that the lower volatility seen in the price-action of ET vs the S&P 500 is due to the market waiting for further clarity on the US Presidential election’s likely outcome. The current leading candidates, Kamala Harris and Donald Trump, have very different energy policies. For example, a Trump presidency is likely to lead to increased O&G output (and hence higher volumes for transportation, which is where ET primarily comes in) given his policy stances that favor drilling. On the other hand, a Harris presidency is a bit more ambiguous in this regard.

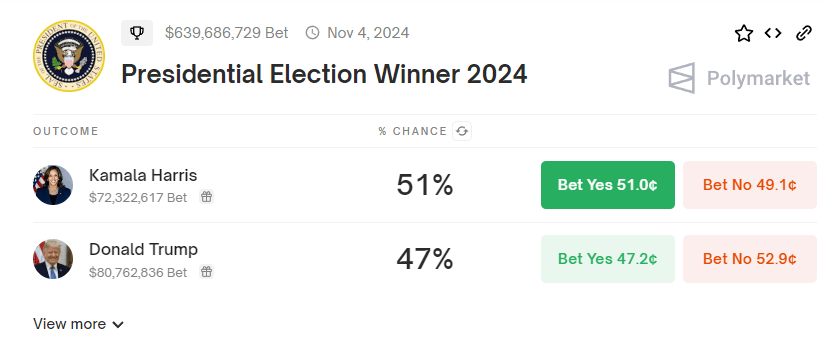

Currently, the prediction markets show a rather tight race, pricing in a mere 400bps probability difference for the winner, with Kamala Harris leading Donald Trump:

US Presidential Election Winner Odds In Prediction Markets (Polymarket)

I prefer relying on the prediction markets as opposed to the polls as I believe the wisdom of the crowd – the same phenomenon that gives Seeking Alpha its value – is better expressed in the prediction markets wherein there is real monetary stake betting on the outcomes (more than $153 million in this case on Polymarket, which is the world’s largest prediction market).

Takeaway & Positioning

All in all, I think Energy Transfer is growing its earnings at a healthy clip, with consistent organic and inorganic footprint and capacity expansions. This is placing the midstream O&G player favorably to capture the opportunities arising from increased energy demand, particularly from data centers.

From a valuation perspective, Energy Transfer is trading at a discount vs its peers, but at a small premium vs its rather well-defined historical 1-yr fwd EV/EBITDA trading range. Whilst it could be argued that such a premium may be well-deserved given the growth catalysts ahead, the technicals vs the S&P 500 suggest to me that it may be prudent to wait a bit longer for a better opportunity to trigger fresh buys. I suspect the market awaiting more clarity on the likely winner of the US Presidential election. I believe the two leading candidates’ stances on energy policy would translate to material implications for Energy Transfer’s volumes.

Rating: ‘Neutral/Hold’

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis, with higher than usual confidence. I also have a net long position in the security in my personal portfolio.

Buy: Expect the company to outperform the S&P 500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P 500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P 500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.