Thinking of maximizing your charitable gifts? Think like a billionaire.

getty

’Tis the season! Chances are that your inbox is pretty full of emails asking you to consider making charitable gifts. Since many charitable organizations count on year-end donations to get them into the black—not unlike for-profit businesses—requests for charitable contributions ramp up in December.

Shrinking donor participation has been a problem since the 2017 Tax Cuts and Jobs Act (TCJA). By nearly doubling the standard deduction and limiting some itemized deductions, that law dramatically reduced the number of taxpayers who itemize—and itemization is still required to deduct charitable contributions on Schedule A in 2025 (that will change in 2026)..

With fewer taxpayers itemizing today than a decade ago, the tax benefits of charitable giving have become increasingly concentrated among those using tax and charitable planning strategies. But no matter whether you’re hoping for a tax break on your gift, or just feeling generous, the details matter. Choose carefully when making your gift, get a receipt (even for cash) and pay attention to donor incentives.

If you’re sitting on a big capital gain, you can kill two birds with one stone by using some of the appreciated stock to fund an account at a donor-advised fund offered by your stockbroker. The donated shares are immediately sold, with the proceeds reinvested in something safer and then dribbled out to charity over an indefinite period. The charitable deduction is calculated from the value of the stock, the gain never taxed.

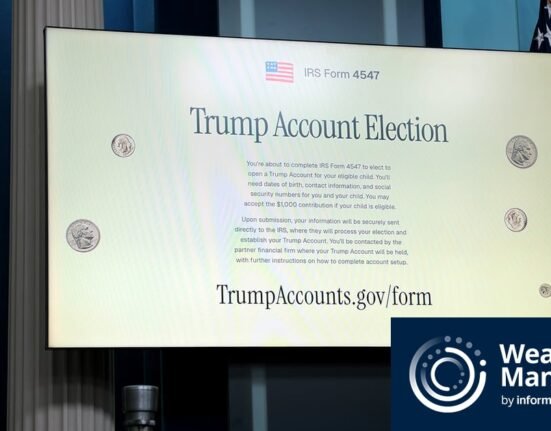

Even the most generous charitable donations won’t come close to one making headlines this month. Michael and Susan Dell made one of the largest philanthropic commitments in modern U.S. history, pledging $6.25 billion to support “Trump Accounts”–those new accounts for children created by the One Big Beautiful Bill Act (OBBBA). As part of that law, Congress committed to seeding accounts for babies born between 2025 and 2028 with an initial $1,000 deposit. The Dells’ billions will seed with $250 each the accounts of roughly 25 million children under age 10, who were born before 2025, and thus aren’t eligible for the $1,000.

The money for the gift is being contributed through the Dells’ own charitable funds, and not through the Dell Foundation—but there’s still a lot you can learn about gifts to and through private foundations and whether you can donate directly to the federal government (spoiler alert: you can). You can find out more here.

The Dells’ money is intended to be used for Trump accounts, a new kind of retirement savings account created by Congress as part of OBBBA. Under OBBBA, a Trump account can be opened for any qualifying child under 18 at the end of that calendar year (but no contributions can be made before July 4, 2026).

There is a $5,000 cap on contributions per year, adjusted for inflation. Contributions can be made by almost anyone, including parents and grandparents—those contributions will count toward the $5,000 annual limit. Employers may also make annual contributions of up to $2,500 to an employee’s or the employee’s dependent’s Trump Account. An employer contribution counts toward the $5,000 limit each year and is not considered taxable income to the employee.

Neither the $1,000 pilot program contribution nor the $250 from the Dells will count towards the annual limit.

Speaking of President Trump, he originally signalled that he might drop his opposition to extending soon-to-expire enhanced Affordable Care Act subsidies. Preserving the subsidies and the Affordable Care Act (ACA) marketplace itself would be especially important to people ages 55-65 and those with pre-existing medical conditions.

(That news was welcome in the markets—health insurance company stocks jumped on the news.)

However, under apparent pressure from fellow Republicans, he seemed to recant the day after Thanksgiving, saying he does not want to prolong the subsidies.

Trump also signed the IRS MATH Act into law. That law requires the IRS to change the format of millions of “math error” notices. Although these notices are meant to handle simple errors quickly, they have often been characterized as vague and confusing. The new law fixes those problems by requiring the IRS to explain exactly what it believes is wrong, why it made the adjustment, and what rights the taxpayer has to challenge that action. Math errors are considered simple, obvious mistakes. A quick rule of thumb: If the issue requires interpretation, investigation, or document review, it is not a math error. Those matters must follow the standard audit and deficiency procedures.

If all of these changes are enough to drive you to drink, consider your location: in many offices, wine at work would get you a call from HR. But in France’s National Assembly, it’s been routine for over a century.

A member of Parliament has proposed ending alcohol sales inside the National Assembly. While the bar isn’t open to the public, it extends a welcome beyond current MPs—the bar is also open to ministers, staff, and former MPs. Drinks at the bar aren’t free, but the prices are considered cheap compared to other bars and restaurants in Paris (and there’s a generous allowance for MPs).

But France is a little bit of an outlier when it comes to allowing booze on the taxpayer’s dime. In many other countries, including the U.S., legislators pay out of pocket: their official allowances explicitly forbid spending federal money on booze.

(Not a legislator? In the U.S., taxpayers can’t deduct alcohol as a personal expense like a non-business related lunch, but alcohol can be deducted as a part of a business meal, marketing or promotional event, or an employee event, like a holiday party—more on that in a moment.)

And with that, I’ll say cheers (but there’s more good stuff below, keep reading) and enjoy your weekend!

Kelly Phillips Erb (Senior Writer, Tax)

This is a published version of the Tax Breaks newsletter, you can sign-up to get Tax Breaks in your inbox here.

Questions

The holiday office party is likely fully deductible.

getty

This week, a reader asks:

I’m throwing a holiday party for my employees. Is all of it deductible?

Most likely, but the details matter. A company holiday party is generally 100% deductible so long as the event is primarily for the benefit of your employees. If that’s the case, the full cost of food, drinks (including alcohol), entertainment, decorations, venue rental, and similar expenses can be deducted.

As with all things tax, there are a few caveats. The party must be for all your employees, not a cherry-picked group of owners or executives. Spouses and family members can join the festivities, too, but the employees should be the primary audience. As always, the key is to keep excellent records, including that it was an employee party, so there’s no confusion later. Other than that, you can relax and enjoy the celebration.

—

Do you have a tax question that you think we should cover in the next newsletter? We’d love to help if we can. Check out our guidelines and submit a question here.

Statistics, Charts, and Graphs

The U.S. generally allows dual citizenships with 63 countries.

Kelly Phillips Erb

Senator Bernie Moreno (R-Ohio) has introduced the Exclusive Citizenship Act of 2025, which would eliminate dual citizenship in the United States. Currently, the U.S. allows its citizens to hold dual citizenship in 63 countries.

Under the bill, Americans who also hold a foreign citizenship would have to choose: either renounce their foreign citizenship or lose their U.S. citizenship. Likewise, anyone who acquires foreign citizenship in the future would automatically be excluded from U.S. citizenship eligibility.

The move is motivated by Moreno’s belief that U.S. citizens should owe “sole and exclusive allegiance” to America. He claims dual citizenship can lead to “conflicts of interest and divided loyalties,” although critics argue the idea might face legal challenges and raise concerns about fairness and the impact on many immigrant families.

The Exclusive Citizenship Act’s automatic or deemed expatriation could cause harsh U.S. tax penalties for many affected individuals under the “covered expatriate” rules of the tax code. Anyone who loses U.S. citizenship and has a net worth of $2 million or more, an average annual income-tax liability over $206,000 for a five-year period (adjusted for 2025 inflation), or who has not been fully compliant with U.S. tax filings for the past five years can be classified as a “covered expatriate.” Upon expatriation, they face an immediate mark-to-market exit tax on their worldwide assets, treated as sold the day before losing citizenship, with a potential 23.8% capital gains tax on unrealized gains. Many could be caught off guard by these tax consequences without intending to expatriate for tax reasons or having time to plan or adjust their assets beforehand.

A Deeper Dive

The IRS has a backlog of ERC files.

getty

Nearly five years after its creation, the Employee Retention Credit (ERC) program is still in the news.

The program was intended to help businesses keep the lights on during the pandemic. Under the ERC program, eligible employers included those that paid qualified wages to some or all employees after March 12, 2020, and before January 1, 2022. The credit amount was significant: 50% of up to $10,000 in wages, meaning it could be as high as $5,000 per employee in 2020 and $21,000 per employee in 2021.

Since the program began, Congress has changed the applicable law four times and thousands of taxpayers have been embroiled in IRS examinations, appeals, and litigation over their ERC claims. Questions remain about who qualifies, what counts as “qualified wages,” and how to properly claim or amend a claim—or withdraw it if eligibility is uncertain.

And, sadly, persistent scams are still out there. Promoters aggressively marketed the ERC as if “every business qualifies,” often charging large filing fees and sometimes misleading or omitting key eligibility details. The result was that some businesses still don’t know whether they qualified (even after submitting claims).

You can find the answers to many of your questions here.

At the same time, the National Taxpayer Advocate (NTA) is calling on the IRS to finish processing all outstanding ERC claims by the end of 2025, noting that tens of thousands of businesses are still waiting, many for over a year. The NTA warns that prolonged delays are harming legitimate businesses that are counting on these refunds to cover operating costs and urges the IRS to prioritize fairness and timely resolution.

The backlog stems from the complexity of the ERC program, including those questionable or fraudulent claims, which forced the IRS to pause and carefully sort through applications. The NTA emphasizes that while the IRS has made some progress, there’s still more work to do.

Tax Filings And Deadlines

📅 December 31, 2025. Deadline for required minimum distributions (RMD) for most individuals subject to RMDs. (If you turned 73 in 2024, you should have taken your first RMD (for 2024) by April 1, 2025, and you also need to take your 2025 RMD by the end of the year.)

📅 January 15, 2026. Fourth quarter 2025 estimated tax payment due for individuals.

📅 January 31, 2026. Deadline for employers to provide employees with wage statements (like W-2s), and for certain information returns to be issued.

Tax Conferences And Events

📅 December 8-9, 2025. NYU Law School. Institute on State and Local Taxation. The Westin New York at Times Square, New York, NY. Registration required.

📅 December 11-13, 2025. American Bar Association Section of Taxation. 2025 Criminal Tax Fraud and Tax Controversy Conference, Wynn, Las Vegas. Registration required.

Trivia

Before the income tax existed, up to 40% of federal revenue came from excise taxes on alcohol. What product basically bankrolled the U.S. government in the 1800s?

(A) Beer

(B) Rum

(C) Whiskey

(D) Wine

Find the answer at the bottom of this newsletter.

Positions And Guidance

The American Bar Association Section of Tax submitted comments to the IRS regarding Notice 2025-45, which generally seeks to ease the application of certain rules governing the re-domiciliation of publicly traded foreign corporations into the United States and stock dispositions occurring close in time to an F Reorganization (an F reorg is a corporate restructuring where a company changes its legal form or structure but stays the same business—an example would include converting from a C-corporation to an S-corporation).

Noteworthy

EisnerAmper has announced leadership transitions at its Minneapolis and San Diego offices, effective January 1, 2026. Matthew T. Brown, a tax partner in the private client services group, has been named partner-in-charge (PIC) of the Minneapolis office, overseeing day-to-day operations and long-term growth strategy for a team of more than 175 professionals. Michelle A. Myhra, also a tax partner in the private client services group, has been appointed PIC of the San Diego office.

Vertex Inc., a global provider of indirect tax solutions, and CPA.com announced an expansion of their partnership to include an AI-driven solution in collaboration with Kintsugi. The application helps accounting firms of all sizes deliver automated, accurate, and scalable sales tax compliance for clients.

–

If you have tax and accounting career or industry news, submit it for consideration here or email me directly.

In Case You Missed It

Here’s what readers clicked through most often in the last newsletter:

You can find the entire newsletter here.

Trivia Answer

The answer is (C) Whiskey.

Taxes from whiskey used to account for a lot of the revenue used to run the federal government.

getty

Before the federal income tax existed, the U.S. government relied heavily on tariffs and excise taxes. The most important was a tax on distilled spirits, especially whiskey, which at times provided up to 40% of all federal revenue. At one point, the federal excise tax on whiskey rose to $2.00 per gallon, an enormous amount (about $78 in today’s money). Whiskey’s use as a revenue source faded after the income tax was introduced in 1913 and Prohibition eliminated legal alcohol sales in 1920—ending the era when the nation was, quite literally, run on whiskey.

Feedback

How did we do? We’d love your feedback. If you have a suggestion for making the newsletter better, submit it here or email me directly.