The company’s set for steady long-term double-digit growth, but it will never likely see enormous growth.

DigitalOcean Holdings (DOCN 0.91%) isn’t exactly a household name. However, neither were Amazon and Apple in their infancy. Both grew to be trillion-dollar companies anyway, richly rewarding investors with the foresight to see what each name would eventually become.

Is DigitalOcean going to follow in their footsteps, turning relatively small stakes in the company now into million-dollar positions later? Keep reading.

What’s DigitalOcean Holdings?

If you’re not familiar with the company — and most people aren’t — DigitalOcean offers a range of cloud computing services. It obviously competes with Microsoft, Alphabet‘s Google, and the aforementioned Amazon on this front.

It’s different from those other players, however. Whereas Alphabet and Amazon are big companies serving big cloud computing clients, DigitalOcean is a small company serving small and medium-sized cloud computing customers, offering smaller companies a means of scaling up their usage of its platform only as necessary and only charging for services that are utilized as they’re utilized. Its smaller customers appreciate not being forced to make a major financial commitment to a cloud service that ends up costing more than it’s worth at the time.

And this market is bigger than you might think. DigitalOcean boasts more than 600,000 paying customers, while market research outfit Imarc Group predicts the small and medium-sized enterprise sliver of the cloud computing market will grow at an annualized pace of 14.9% through 2032.

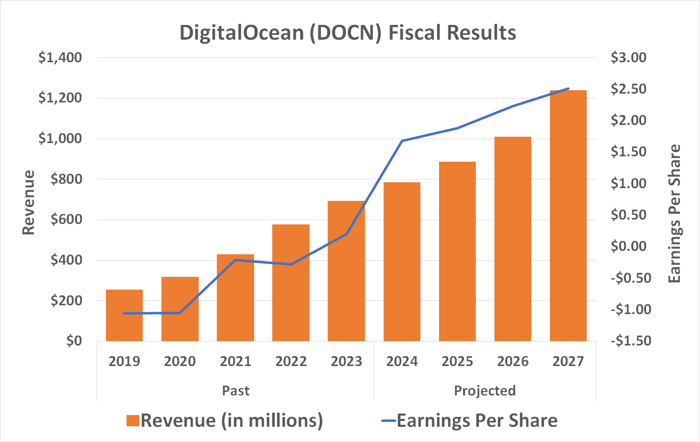

The company is clearly cashing in on this growth, too. Through the first two quarters of this year, DigitalOcean’s revenue grew nearly 13% despite fresh economic headwinds, following last year’s 20% improvement. Earnings are growing at an even faster clip. Both the top and bottom lines are expected to continue improving at a comparable pace.

Data source: StockAnalysis.com.

But is it a millionaire-making kind of stock?

Built to last and compete

Veteran investors have heard plenty of “surefire winner” stories before. But many of them don’t pan out. Names like Groupon, Blue Apron, and GoPro come to mind. Each of these names created lots of hype when they were new. Their results, however, didn’t exactly live up to lofty expectations. Mega-successful companies like Apple and Amazon are seemingly an exception to the norm.

So where does DigitalOcean lie on the spectrum ranging from likely devastating disappointment to smashing success? Probably somewhere in the middle, or perhaps slightly closer to the “success” side of the scale.

The cloud computing market is crowded. As the bigger names in the business. like Microsoft and Alphabet, evolve, they’re becoming at least a little more like DigitalOcean by offering more self-service, a la carte features, and smaller-scale options. None of these major service providers are simply going to let DigitalOcean operate unchecked when a small cloud customer could eventually become a bigger one.

DigitalOcean enjoys an edge on its bigger competitors though. That’s its small size, and the fact that it’s built from the ground up specifically to meet the unique, cost-minded needs of small and mid-sized businesses. That’s most businesses these days. And, that’s apt to be the case into the distant future too. Amazon Web Services, Microsoft, and Google are each capable of addressing the small-enterprise market, but they must remain focused on the industry’s large-scale customers to satisfy their shareholders.

Not every investment has to be a grand slam

The question remains, however — could a $10,000 investment in the stock eventually be worth $1 million?

Assuming this stock logs gains at an average rate of return mirroring its recent and projected top-line growth of 13% — which isn’t unreasonable, given the recurring-revenue nature of its business — it would take you nearly 40 years for a $10,000 investment in DigitalOcean Holdings now to reach the seven-figure mark. That’s less than a lifetime, but by that point in time, $1 million won’t exactly be the massive amount of money it is today. Much could happen during that time to derail the company’s current and expected growth, too.

Still, this doesn’t mean DigitalOcean Holdings isn’t a great investment to consider owning for the foreseeable future.

There’s little doubt that the advent of artificial intelligence is driving growth in demand for cloud computing services, at least for the next several years. That’s particularly true for smaller enterprises that are just now recognizing that AI is here to stay. Around two-thirds of small and medium-sized companies operating in the U.S. intend to spend more on such technology this year despite fresh economic headwinds. They’ll have to invest in artificial intelligence just to remain competitive.

And that’s just AI. Never mind the growing need for more basic cloud computing solutions like customer service apps or simple data storage, the need for both of which also continues to swell (and will likely continue to for many more years).

Yes, this stock surged late last week in response to its second-quarter growth and forward-looking guidance, making it a little uncomfortable to step into here and now.

Take a step back and look at the bigger picture, though. This stock is also still down more than 70% below 2021’s post-IPO peak and, for that matter, is still under last July’s high. It’s priced at less than 20 times next year’s expected per-share profits as well, which is an outright bargain in this environment. It’s also a company meeting the needs of an underserved market.

If you’re tolerant of its inevitable volatility, don’t overthink taking on a stake in this company.

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. James Brumley has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, DigitalOcean, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.