gerenme/iStock via Getty Images

Overview

I previously covered Starwood Property Trust (NYSE:STWD) back in November 2023 and since my initial coverage, STWD has provided a total return of 10%. Despite this undercutting the performance of the general S&P, I am quite happy with that performance when you consider the fact that real estate was one of the worst performing asset classes over the last three years because of interest rate fluctuations. Even though the total return of STWD is down over 3%, it outperforms the general real estate sector (XLRE).

Just for some context, Starwood Property Trust operates as an mREIT that generates their earnings through different forms of lending through commercial and residential properties. The company has a market cap of about $6B and has a public inception dating back to 2009. The company was actually founded as a way to offer a solution to the 2009 crisis as they saw a need for alternative commercial mortgage financings. STWD’s current dividend yield of 10% makes it an attractive option for investors looking to capture a reliable source of dividend income. While the dividend hasn’t been increased, it also hasn’t been cut in over a decade. I want to also discuss how STWD can be used as a tool to grow your dividend income, despite there being a lack of raises.

The share price has also remained relatively flat and consistent throughout the company’s history. This makes it less difficult to determine what valuation looks like and whether or not it would make for a good entry price. The price of STWD is only up 20% since its inception, and commonly floated around the $20 to $25 per share range for the majority of its history. However, I believe that the impending interest rate cuts may serve as a catalyst for a bit of a price boost going forward. Before discussing valuation, I would like to first start by reviewing their portfolio strategy and what makes STWD a continued buy.

Portfolio & Risk Profile

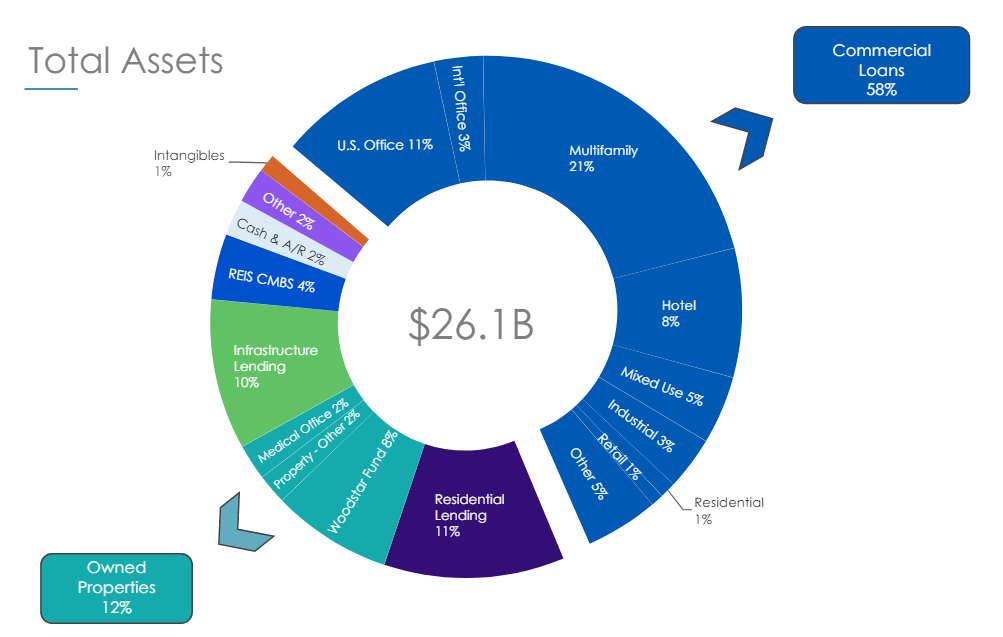

STWD has about $26.1B in total assets, and we can see that this spans across many different areas of real estate. This wide reach enables investors to gain instant diversity within the real estate sector, which mitigates the risk from any sector-specific concentration. Speaking of risk, something that I do not like is the US Office exposure, but thankfully this only accounts for 11% of their portfolio. US Offices were a large source of weakness in the real estate market during and after the pandemic era as many companies started to embrace a remote or hybrid working model.

As a result, there was a much lower demand for these sorts of properties and vacancies began to rise. While conditions may be improving now that the pandemic has ended, I still prefer to limit my exposure to this space as someone that personally prefers a remote or hybrid working environment. The data surrounded worker preferences clearly tells us that people value remote work, and I am sure this will continue to have some sort of negative impact on the office space sector. As a result, I would like to see SWTD’s exposure here decrease a bit.

STWD Q1 Presentation

About 63% of their earnings are generated from the commercial lending space which is primarily US focused but also includes international exposure across Europe, Asia, and Australia. The commercial lending segment also focuses on maintaining a level of diversity, with 154 different individual loans that carry a total value of $15.1B. In my opinion, the most important aspect of this segment right now is the fact that their lending has a 98% exposure to floating rate loans.

The emphasis on floating rate loans can be beneficial but can also add risks, depending on the environment. For instance, the Federal Funds rate now sits at a decade high, which is great for income generation through higher interest payments that borrowers have to pay to STWD. However, a prolonged period of these higher rates could also put some strain on a borrower’s ability to continue maintaining their debt if the business is also underperforming.

To better visualize this, we can see the clear inverse relationship that STWD’s price has with the Federal Funds rate. When interest rates were cut to near zero levels in 2020, we see the price of STWD rapidly move upward as it was a more attractive environment for borrowers. As a result, STWD likely had access to more deals and opportunities to help them grow their portfolio and earnings. Conversely, when interest rates started to get hiked throughout 2022, we saw the price of STWD consistently decline and has only recently stabilized.

As a result of these higher rates, we’ve seen some loans go into default status. Higher interest rates directly translates to a higher monthly payment for borrowers on a floating rate basis. STWD using an internal number rating system that grades the quality of tenant. A rating of 1 represents the most secure borrower, whereas a rating of 5 represents the lowest quality borrower. We’ve seen a few different loans shift to lower quality ratings. From the last earnings call, we received the following insights.

We downgraded two smaller loans to five in the quarter, an $82 million mezzanine loan on an office building in Los Angeles where the borrower has remained current and we are working to extend term allowing time to complete accretive leasing and a $52 million multifamily loan in Nashville that is in payment default and we expect to foreclose on. We will decide in the coming quarters whether to maximize value by holding and stabilizing this asset as we have in the past or sell it at or near our basis depending on the short-term direction of cap rates. We also downgraded three loans in the quarter from a three to a four risk rating. – Jeff DiModica, President

However, the tide may be turning as conditions indicate that a higher possibility of interest rate cuts happening. Interest rate cuts may ultimately provide relief to these troubled loans, as well as make conditions more ideal for new potential borrowers. The Fed has left rates unchanged over the last several meetings as they awaited more economic data to roll in around inflation, consumer spending, and the labor market. However, the inflation rate has ticked down over the last two months and the unemployment rate has now crossed over the 4% mark. These two indicators may indicate that interest rate cuts are getting closer on the horizon.

Financials

STWD released their Q1 earnings at the beginning of May and the results were solid. Distributable earnings per share landed at $0.59 while revenue increased by 6.7% year over year, amounting to $523M. During the quarter, STWD made some moves that enable the possibility of additional portfolio growth going forward. For instance, they were able to generate net proceeds of $188M through the sale of their Master Lease Portfolio. This helped reinforce the success that STWD had in growing the value of their owned properties, as well as provided the business with cash that could be further reinvested towards new opportunities.

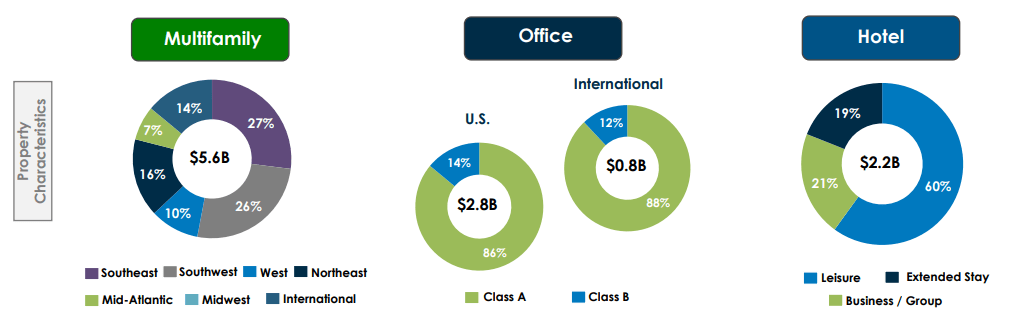

An example of this growth would be how STWD was able to originate about $413M of assets across all business lines over the quarter, which can help grow revenue as conditions for the sector improve. Looking at STWD’s top ten loans by largest property type reveals that the multifamily space is where the bulk of their exposure lies, totaling $5.6B. As previously mentioned, they do have some exposure to office-based properties, which account for about $2.96B throughout the US and international markets. Lastly, hotels account for $2.2B of their top ten loans.

SWTD Q1 Presentation

STWD still prioritizes growing their portfolio where possible through new investments. For Q1, they have total new commitments totaling $120M, $96M of which is already funded. They also received $210M in repayments, which can be allocated to different growth initiatives in the portfolio.

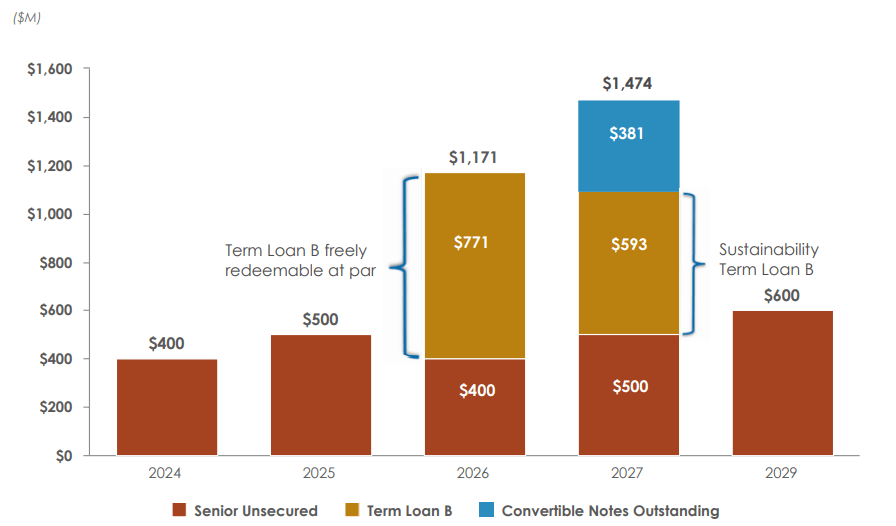

Despite the challenging conditions for the real estate sector as a whole, STWD maintains a strong liquidity profile, with cash and equivalents totaling $327.4M at the end of the quarter. Net debt sits at about $18.1B, but there seems to be no worries here as the business maintains a solid debt maturity schedule. They do have debt of $400M due this year, but this can be covered with the available credit capacity of $9.7B across all their existing financial lines. The largest amount of their debt due is in 2027, but this gives STWD ample time to accumulate the needed cash in advance.

STWD Q1 Presentation

STWD has remained a pretty consistent performer as well. Looking at the earnings history, STWD frequently reported EPS between $0.49 to $0.59. This consistency translates to the consistent dividend income that investors have come to expect over the last decade.

Dividend

As of the latest declared quarterly dividend of $0.48 per share, the current dividend yield sits at about 10%. This double-digit yield makes STWD a highly attractive offering for investors looking to create an instant, sizeable stream of dividend income. As mentioned, the last earnings reported distributable EPS at $0.58 which means the dividend is fully covered with a large enough margin of safety to instill investor confidence.

The dividend has been ultra stable over the last decade, having never cut or reduced the dividend since its inception. However, STWD has provided absolutely zero growth in the dividend over the last decade. The lack of raises here do not mean STWD is unable to raise the dividend, but instead reinforces the company’s defensive stance. This stance has now built a reputation for its consistency and has grown as an attractive choice for investors that are looking to add a stable source of dividend income to their portfolio. Even though STWD hasn’t increased their dividend rate, this doesn’t mean you can’t grow your income over time.

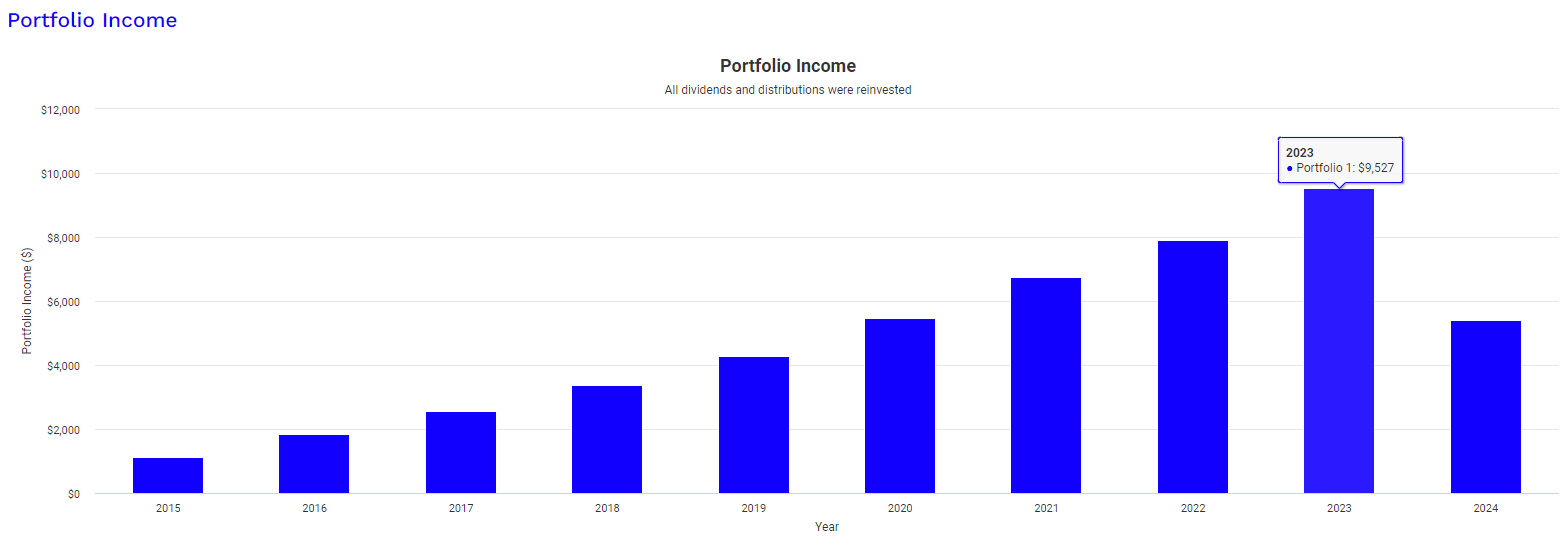

You can essentially create your own growth through continued reinvestment of dividends as well as adding more capital to your position over time. To better display this, I ran a back test using Portfolio Visualizer to show what a $10,000 starting investment would look like. This graph assumes that all dividends received were reinvested, as well as a consistent monthly contribution of $500 to your position throughout the entire holding period. Through a long-term outlook and consistency, investors could have grown their income to a sizeable amount that certainly packs enough of a punch to pay some bills throughout the year.

Portfolio Visualizer

In 2015, your dividend income would have totaled $1,132 for the year. Fast forwarding to the full year of 2023, your dividend income would now total $9,527. So even with the absence of formal dividend raises from STWD, we can see that the stability provides a foundation that can enable dividend income growth through continued investment. Something worth mentioning is that the dividends received from STWD are classified as ordinary dividends and are taxed at less favorable rates compared to the qualified dividends you would receive from traditional dividend growth stocks.

Valuation

As previously mentioned, the price of STWD has consistently traded at a relatively stable range between $20 and $25 per share over the last decade. However, the rise of interest rates has now dropped the price to more attractive levels. I do believe that as interest rates get cut, we have a strong possibility of seeing a price movement upward. Interest rate cuts would provide relief to current borrowers while simultaneously creating a more attractive environment for new borrowers as the cost of acquiring new debt is cheaper.

In addition, STWD now sits at a slightly discounted price to book value, which may indicate an attractive point for entry. We’ve historically seen STWD’s price to book value rest between the 1.0 to 1.5 range, which is more aligned with the average. The general rule of thumb is that anything below a price to book value of 1.0 is believed to be trading at a discount.

Wall St. also seems to agree that now would be a solid time for entry, based on the average price target of $21.36 per share. This represents a potential upside of 10.7% from the current price level. The highest price target sits at $24 per share and the lower sits at $19.50 per share, which means that Wall St. also estimates there to be a greater upside potential than downside risk since even the lowest price target sits above the current price.

Takeaway

In conclusion, STWD’s reliable performance and stability in distributions makes it an attractive company for investors that want some exposure to real estate while also building a reliable stream of dividend income. Future interest rates can serve as a catalyst for future growth as it provides relief to the current borrowers while simultaneously making the debt environment more attractive for new borrowers. Interest rate cuts could cause higher volumes of potential borrowers, which may open the door for more deals that STWD can capitalize on through continued investment in their portfolio. The stock also sits at a discounted price to book ratio, which may indicate that it’s an attractive time for entry. As a result, I maintain my buy rating on STWD stock.