AGNC currently yields almost 14%, but income investors should consider the following before piling into the stock.

If you want to generate passive income from your portfolio, AGNC Investment Corporation (AGNC -0.68%) is one stock that has likely grabbed your attention with its dividend yield of almost 14%.

In addition to its juicy yield, the mortgage real estate investment trust cuts investors a monthly check. It seems like an attractive option for those looking for a steady stream of passive income. But is AGNC the best dividend stock for your portfolio? Let’s dive into the business and its risks to answer that question.

The engine powering AGNC’s lofty dividend

As a mortgage real estate investment trust (mREIT), AGNC has a business model different from your typical REIT. Rather than investing in physical properties like apartments, office buildings, or data centers, it invests in residential mortgage-backed securities (MBS).

These are pools of residential mortgages bundled together and sold to investors. Specifically, AGNC focuses on agency MBS, which are mortgages where government-sponsored entities like the Federal National Mortgage Association (Fannie Mae) and the Federal Home Loan Mortgage Corporation (Freddie Mac) guarantee principal and interest payments.

Investing in government-backed mortgages is less risky because the government backs these loans, even if a homeowner defaults. This government backing helps attract more investors, ultimately expanding the pool of funding available for housing.

Image source: Getty Images.

However, MBS don’t have tremendous yields on their own. AGNC’s portfolio has a weighted average yield of 4.52%, so the company uses leverage — meaning debt — to boost returns for investors. The company expects leverage to be around 6 to 12 times its tangible stockholders’ equity.

It gains leverage by borrowing against its assets, which helps boost returns during good times. However, leverage also exposes it to more risks if borrowing costs rise, underlying asset values fluctuate, or mortgage spreads change. As a result, the company is vulnerable to significant losses during times of high volatility or reduced market liquidity.

This risk of mortgage real estate investment trusts

Interest rates can have a sizable effect on a company like AGNC. For example, rising interest rates have boosted its portfolio yield from 2.6% to 4.5% in the past couple of years.

On the flip side, rising rates have resulted in a higher spread between its asset yield and the yield on benchmark interest rates linked to its interest rate hedges, making it more costly for the company to hedge its portfolio. On top of that, higher interest rates reduce the value of its investment portfolio because of the inverse relationship between interest rates and price.

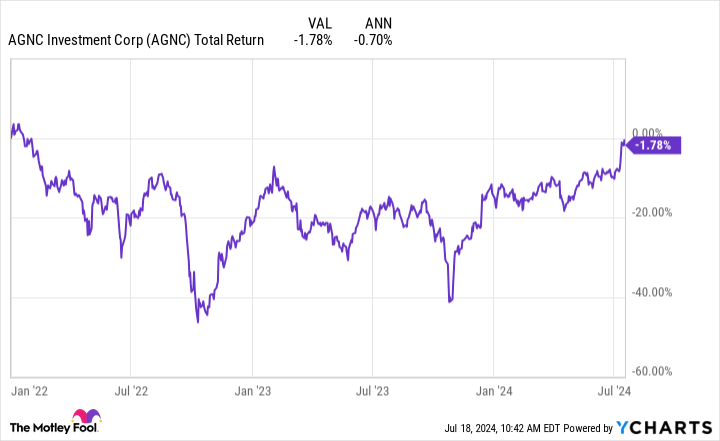

This relationship becomes evident when you look at AGNC’s stock performance over time. From 2009 to 2021, the 30-year mortgage rate gradually declined without too much volatility. AGNC stock plus dividends returned investors 329% over this time, or about 11.9% annually.

It’s been a different story since then. In 2022, the Federal Reserve began aggressively raising interest rates as it looked to put a lid on inflation. During this time, the company’s total return is a negative 1.8%, while its tangible book value per share has fallen 43%, from $15.75 to $8.84.

AGNC total return level; data by YCharts.

Is AGNC for you?

AGNC has struggled to perform well during the past several years amid rising rates. Although it has delivered a hefty dividend payout, it has displayed lackluster performance and disappointed investors looking for a blend of dividend income and growth.

The good news for investors is that falling interest rates could be a tailwind. In recent years, the company has invested in securities with higher yields, and falling rates could boost its book value. Less interest rate volatility and a steepening yield curve could benefit the mREIT, resulting in a rising net interest margin. You might find it suitable if you want a juicy yield and don’t mind the volatility.

However, the company lacks a robust economic moat and is vulnerable to fluctuations in interest rates, and you can’t necessarily expect rates to drop to the low levels of a few years ago. JPMorgan Chase Chief Executive Officer Jamie Dimon recently told investors, “Interest rates may stay higher than the market expects.” Therefore, I think most investors are better off looking elsewhere for reliable income stocks that can provide solid returns in the long term.

Courtney Carlsen has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.