sommart/iStock via Getty Images![]()

Global markets were mixed over the June quarter, with divergent themes impacting key markets.

In the U.S., the S&P 500 (SP500, SPX) and Nasdaq continued to move higher. Contrary to last quarter where there were signs of a broadening in the market rally across sectors, U.S. returns this quarter were concentrated in mega-cap technology stocks – most notably Nvidia (NVDA), Apple (AAPL) and Microsoft (MSFT). The top 5 holdings in the S&P 500 now make up ~29% of the index, the highest concentration in 50 years.

European markets were generally negative, as French elections and their impact on the country’s future fiscal sustainability weighed on the broader region.

The Australian market was also marginally negative (ASX200AI -1.1%) with continuing signs of a softening macroeconomic environment. The rate of real GDP growth has declined further and lower household disposable incomes have driven a prolonged benign rate of retail sales growth, despite record levels of inbound migration.

However, inflation in Australia remains stubbornly high. Very high levels of federal and state government expenditure, in addition to recent income tax cuts, have increased the risk that the RBA may increase interest rates further in order to return inflation to its target range (2-3%) within a reasonable timeframe.

The strongest sectors in the ASX 200 for the June quarter were Utilities (+13.3%), Financials (+4.0%) and Information Technology (+2.9%), while Energy (-6.8%), Materials (-5.9%) and Property (-5.6%) lagged.

Returns (‘net’) (%)1

|

Catalyst Fund |

S&P/ ASX 200 AI |

Outperformance |

|

|

3 months |

(6.8) |

(1.1) |

(5.7) |

|

6 months |

0.8 |

4.2 |

(3.4) |

|

1 year |

1.7 |

12.1 |

(10.4) |

|

2 years p.a. |

9.5 |

13.4 |

(3.9) |

|

3 years p.a. |

9.9 |

6.4 |

+3.6 |

|

Since inception p.a. |

9.9 |

6.4 |

+3.6 |

|

Since inception cumulative |

32.8 |

20.3 |

+12.5 |

|

1All performance numbers are quoted net of fees. Figures may not sum exactly due to rounding. Inception date: 1 July 2021. Past performance should not be taken as an indicator of future performance. Note: Fund returns and Australian indices are shown in A$. Returns of U.S. indices are shown in US$. Index returns are on a total return (accumulation) basis unless otherwise specified. |

The L1 Capital Catalyst Fund continues to find value in low P/E stocks with undergeared balance sheets, strong cash flow generation and realisable near-term catalysts. We remain confident in our portfolio and are focused on identifying and enacting catalysts through active engagement with company management and Boards.

Portfolio commentary

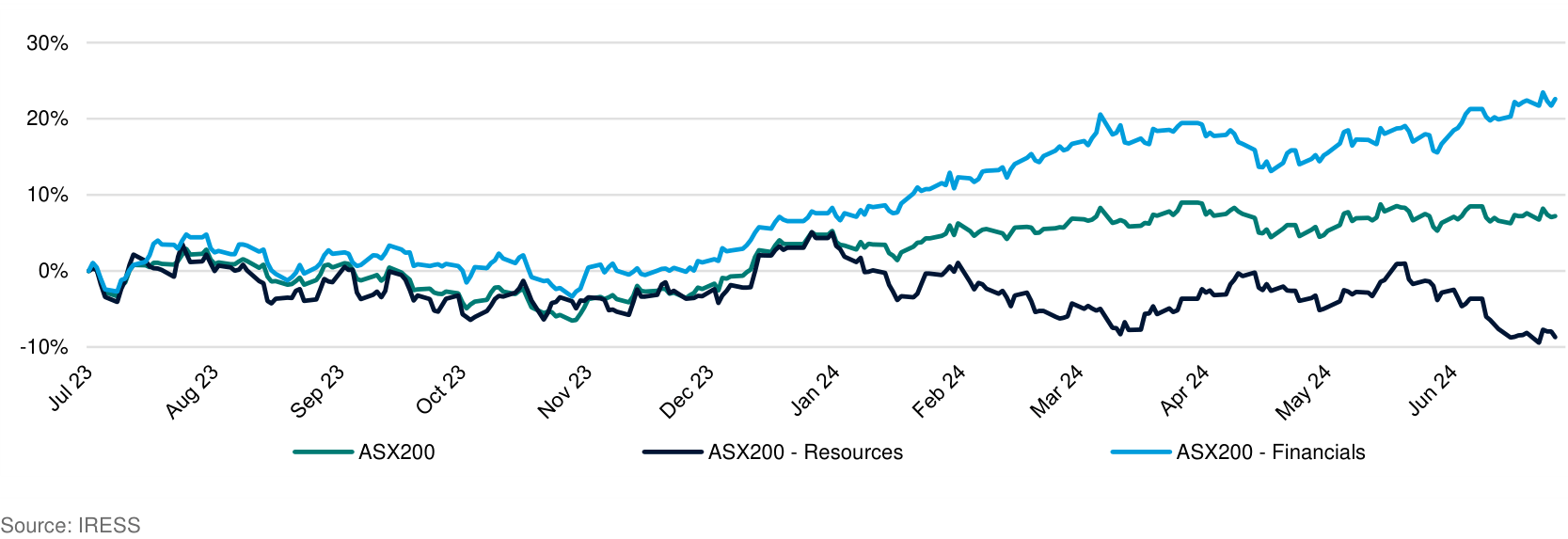

The performance of the Catalyst Fund during the June quarter has been disappointing compared with its strong performance in the three years since inception. During the June quarter, the Fund has intentionally had a relatively high weighting to the Resources sector and no exposure to Australian banks (as will nearly always be the case). However, as shown in Figure 1, this has coincided with a period of significant underperformance of the ASX 200 Resources sector and relative outperformance of domestic Financials (especially the “Big 4” banks).

We constantly monitor and review the portfolio composition and we remain confident that, in particular, the Resources companies we have selected are high-quality commodity producers with long-term structural tailwinds that are now trading at even more compelling valuations.

This outperformance of Australian Financials over the past 12 months has been a significant headwind for the Catalyst Fund. In our view their valuations have become extremely difficult to justify. For example, CBA has the highest valuation of any bank globally (nearly double that of J.P. Morgan), despite a weak earnings growth outlook (EPS expected to be relatively flat over the next two years), a weakening Australian economy and dividend yield below the current Australian cash rate.

Figure 1: Relative performance of ASX 200 Resources and Financials sectors

During the June quarter, the Catalyst Fund’s performance relative to the ASX 200 was positively impacted by:

- Improved execution and market recognition: Qantas’ (OTCPK:QABSY) shares performed well after outlining plans to improve its Loyalty offer to enable easier access for Frequent Flyer members to use their points through the launch of Classic Plus. This revision had a smaller impact on earnings than the market expected and the company clearly articulated the strong medium-term benefits of investing in the program. We believe Qantas remains very well placed given it has Australia’s best loyalty business (expected to double earnings over the next 5-7 years), a raft of brand new, more fuel-efficient aircraft to be delivered over the next few years along with Project Sunrise, which will enable direct flights from Melbourne/Sydney to London and New York from 2026. It also has sufficient balance sheet capacity to continue buying back shares and to recommence fully franked dividends in FY25. The new CEO, Vanessa Hudson, is rapidly and methodically addressing customer ‘pain points’ which should improve sentiment from both customers and potential investors. Qantas trades on a FY25 P/E of only 6.3x, despite a dominant industry position and a high growth, capital-light loyalty division that remains incredibly underappreciated by the market.

During the June quarter, the Catalyst Fund’s performance relative to the ASX 200 was negatively impacted by:

- Weaker commodity prices: Certain commodity prices weakened over the period, including lithium spodumene (-15%) which was adversely impacted by significant, fast evolving new supply out of China and Africa. During the June quarter, this negatively impacted the share price of our holding in Mineral Resources (MALRF, -24%). We continue to remain constructive on Mineral Resources moving forward, noting its valuation remains attractive, being underpinned by the value of the long life and infrastructure-like Mining Services division’s earnings, and we see numerous catalysts over the next 12 months to drive outperformance of the sector. These include the successful ramp-up of the company’s Onslow Iron ore project, which will significantly increase its scale and cost competitiveness, and de-leveraging following the closing of its A$1.1b (net proceeds) sale of 49% of the Onslow Haul Road.

- Increase in long-term bond yields: Long-term interest rates moved higher during the June quarter following the release of persistently high inflation data and the deferral of rate cut expectations. One of the Catalyst Fund’s yield-based portfolio companies was negatively impacted by this increase in long-term bond yields and the broad sentiment that interest rates may stay higher for longer.

Stock spotlight: QBE Insurance

QBE Insurance Group (OTCPK:QBEIF) has been one of the leading contributors to the Catalyst Fund over the past few years. We believe it offers a good case study on how our contrarian based investment philosophy, medium term investment horizon and focus on Value, Quality and Catalysts can deliver strong performance.

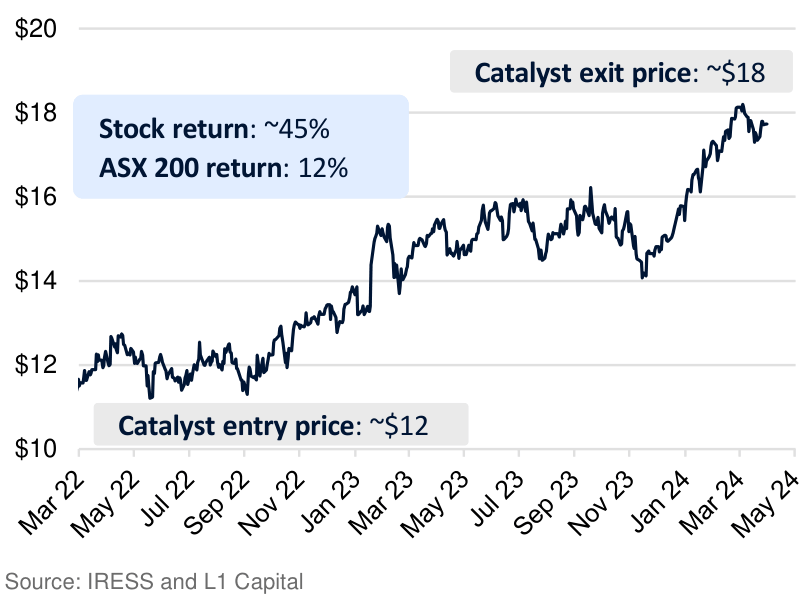

In our March 2023 Quarterly Report, we outlined why we viewed QBE as an undervalued business. While we had been cautious on the company for many years given the industry headwinds it was facing, our view was that the market underappreciated the improvement in the operating backdrop and the strong catalysts for the company to deliver improving margins, dividends and return on equity (‘ROE’) going forward.

Since that time, several of the catalysts we identified have been realised. We therefore elected to exit the position, achieving a ~45% stock return over our holding period vs. 12% for the ASX.

Figure 2: QBE Insurance share price

We have outlined some of the key areas on which we focused our investment analysis and how this may have differed to market expectations at the time of our investment.

1. Stronger underwriting profits

During 2021 and 2022, our analysis of QBE’s work to improve its operational performance, together with our work on premium rate trends, led us to conclude that underwriting profits should continue to improve ahead of market expectations.

We reviewed previous insurance cycles (early 2000s and 2010s), analysed competitor company results, spoke to industry experts and studied insurance broker performance.

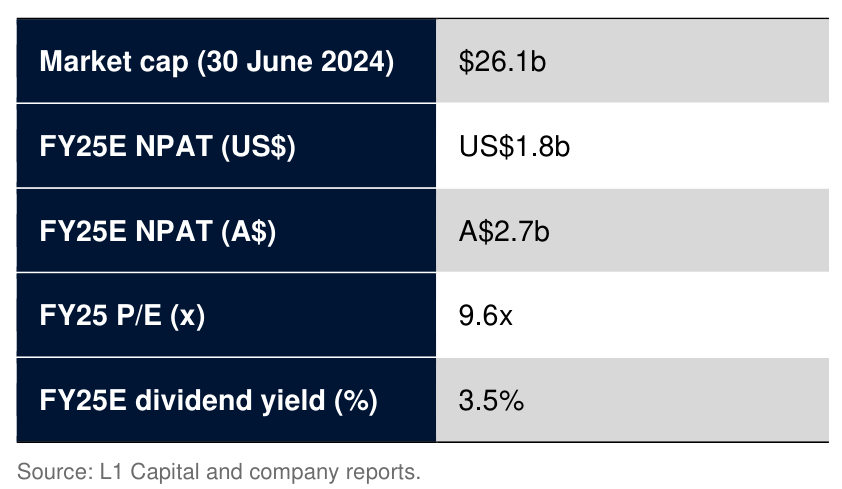

Figure 3: QBE Insurance key ratios

The evidence suggested the premium rate cycle at the time would be significant and prolonged, especially owing to the unique combination of multiple drivers of premium rate rises (higher natural catastrophe claims costs, underwriting losses from prior low premium rates, higher reinsurance costs, COVID-19 insurance claims losses, high inflation and lower availability of insurer capital) compared to historical cycles which were typically preceded by only a few main factors.

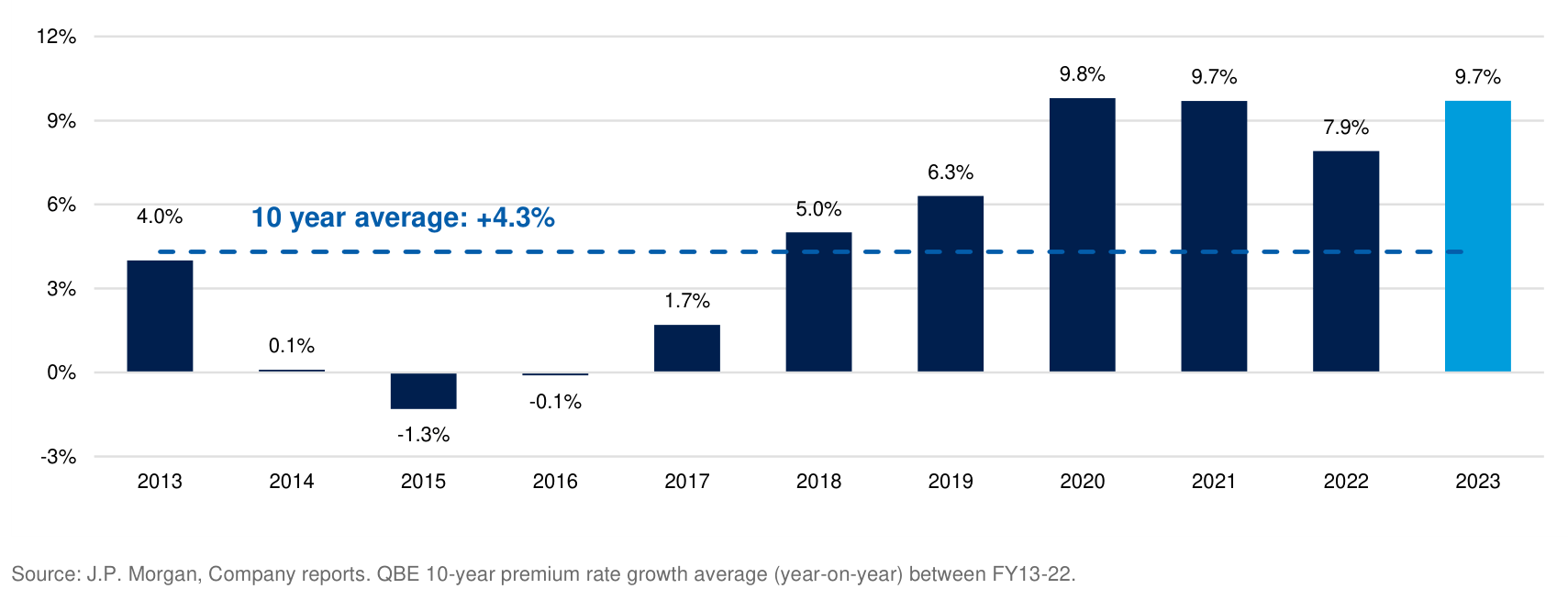

The company managed to achieve a premium increase of 9.7% in 2023, vs. the ~8.0% expected by the market. This supported strong revenue growth as well as higher future margin potential as higher rates on new business flow into future earnings. For FY23, these premium increases, combined with organic volume growth and management actions to reduce risk exposure (discussed further below), drove a 30% increase in underwriting profits.

Figure 4: QBE premium rate movements (year-on-year, %)

2. Higher investment income optionality

With interest rates remaining low for an extended period, we believed the market had discounted QBE’s potential to earn significant investment income from its ~US$26b fixed income asset portfolio. Given the risks of inflation remaining more persistent, we liked the strong operating leverage of the company to a higher interest rate environment. QBE’s FY23 investment earnings ended up rising ~70%, as its fixed income yield increased from 2.6% in FY22 to 4.4% in FY23.

3. Improved earnings stability

QBE delivered FY23 earnings growth of 100% and demonstrated solid earnings stability by meeting management guidance. FY24 guidance, which was recently reiterated, also points to further earnings growth and margin expansion. This is a notable achievement compared to history where QBE missed guidance on numerous occasions. In our view, the improvement in consistency was assisted by the following key factors:

- Renewed senior leadership: Andrew Horton’s appointment as QBE CEO was announced in May 2021, after 30 years’ experience across insurance and banking, most recently as CEO of UK insurer Beazley (since 2008). Under Andrew’s leadership, Beazley’s business grew profitably by ~10% p.a.. During our investment due diligence we reviewed the track record of Mr Horton, spoke to executives who had worked with him, as well as to equity analysts in the U.K. market, and found he had a consistent record of setting conservative targets and outperforming. This increased our confidence that under his leadership QBE would head in the right direction in terms of “under promising” and “over delivering”.

- Stronger reserves: QBE considerably strengthened its reserving from 2019 to 2022. Our work studying the company’s reserve requirements over time supported the view that a very conservative set of assumptions had been applied to the company’s forecasts. Given this set up, we expected the company to have significant flexibility to deliver consistent earnings growth going forward by releasing reserves in the event of any softening in the operating environment, effectively increasing its margin of safety to meet or beat guidance. On top of this, QBE reinsured large parts of its portfolio, therefore removing the reserving risk from many volatile segments of its portfolio. In FY23, QBE decreased its estimate of longer dated claims (the key driver of previous volatility) reserves for the first time in many years, implying reserve strength is now above requirements. So far in FY24, QBE does not expect any adverse movements in reserving relating to longer dated claims.

- Reduced exposure to more volatile parts of the business: QBE undertook initiatives to lower its exposure to large annual movements in claims from weather events. Specifically, management reduced the size of its property insurance segment, the key source of weather claims. QBE also increased the conservatism of its annual weather claims budget (i.e. the expected annual weather claims guidance). The risk of negative surprises from actual weather claims being above expectations was thus greatly reduced. This was evidenced earlier this financial year where year-to-date catastrophe costs tracked within budget, despite large losses from severe storms in the U.S. and floods in Dubai.

- U.S. turnaround: We have been encouraging QBE to exit its underperforming U.S. middle market segment for many years. The company has recently taken the decision to exit this business. It has been structurally challenged for an extended period, and we view management’s actions here as key to improving returns in North America.

In summary, while we believe that QBE remains a quality business that is well positioned and well managed, with many of our earlier views now reflected in the market outlook, we recently exited the position to fund alternative investment opportunities.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.