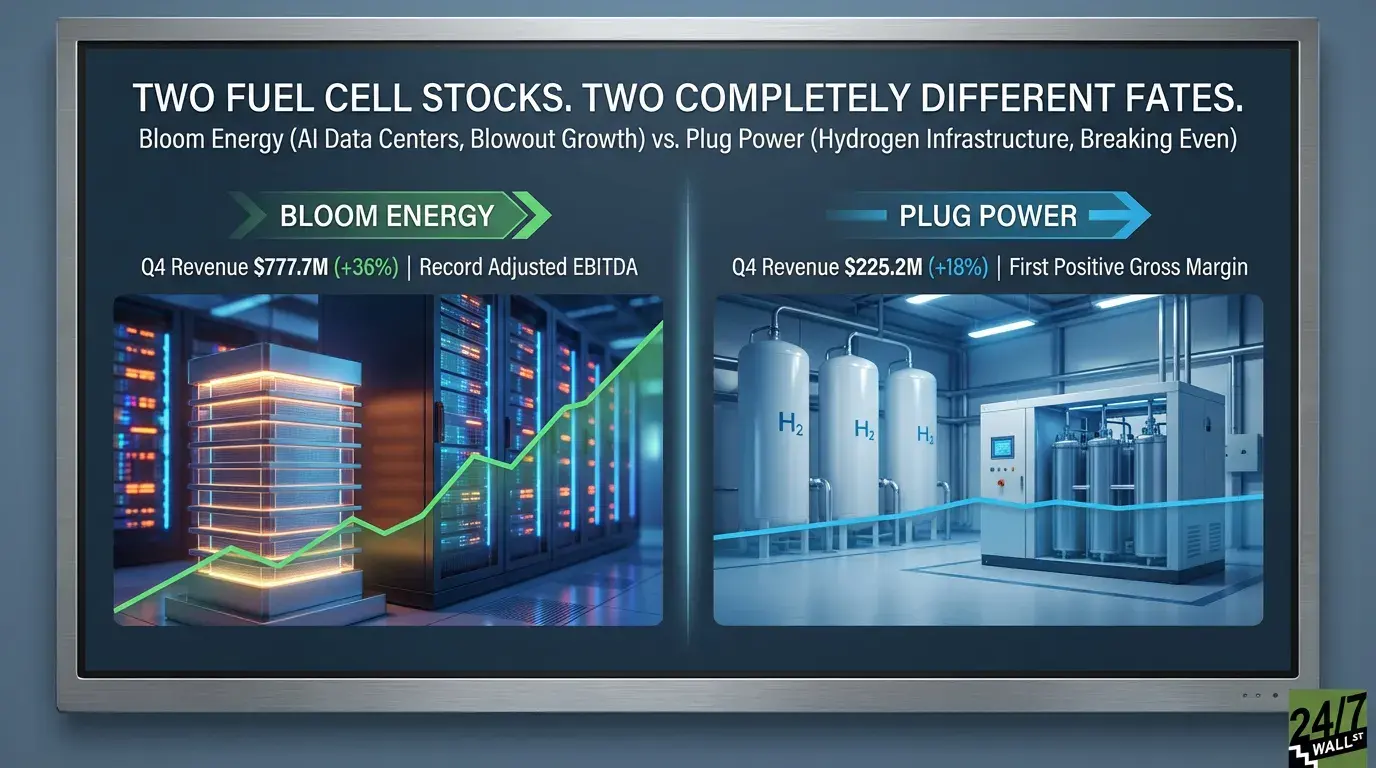

Bloom Energy (NYSE: BE) and Plug Power (NASDAQ: PLUG) have both reported Q4 2025 earnings, and the contrast is stark. Bloom delivered a blowout quarter powered by AI data center demand and a profitable service business. Plug Power achieved something far more modest: its first positive gross margin in years. These two fuel cell companies are operating in entirely different financial realities.

Bloom Fires on All Cylinders. Plug Power Celebrates Breaking Even.

Bloom’s Q4 results were exceptional. Revenue hit $777.7 million, up 35.9% year-over-year, beating estimates of $671.7 million. Non-GAAP EPS came in at $0.45, ahead of the $0.32 consensus. Full-year revenue reached $2.0 billion, up 37.3%, with record adjusted EBITDA of $271.6 million. CEO KR Sridhar called it “our best year yet.”

Plug Power’s story is different. Q4 revenue totaled $225.2 million, up 17.6% year-over-year, with its first positive gross margin at 2.4%, versus negative 122.5% in Q4 2024. Adjusted EPS was −$0.06. Incoming CEO Jose Luis Crespo noted the company achieved $710 million in revenues and Q4 margin positive as projected—a milestone that most profitable businesses crossed years ago.

| Metric | Bloom Energy (Q4 2025) | Plug Power (Q4 2025) |

|---|---|---|

| Revenue | $777.7M | $225.2M |

| Gross Margin | 31.9% | 2.4% |

| Adjusted EPS | $0.45 | −$0.06 |

| Full-Year Revenue | $2.0B | ~$710M |

| Stock Price | $166 | $1.81 |

AI Data Centers vs. Hydrogen Infrastructure

Bloom has repositioned as critical AI infrastructure. Its solid oxide fuel cells produce 800-volt DC power natively, exactly what next-generation AI compute racks require. The product backlog reached approximately $6 billion, up 140% year-over-year, with half a dozen hyperscale and neo-cloud customers versus just one a year ago. The service business now delivers eight consecutive quarters of profitability, with Q4 service gross margin hitting 20% for the first time.

Plug Power’s strategy centers on hydrogen infrastructure. Electrolyzer revenue reached a record $188 million in 2025, including 25 megawatts for Iberdrola and BP and 100 megawatts for GALP in Portugal. But the company spent years burning cash: cumulative operating cash burn from 2020 through 2024 exceeded $3 billion. Its turnaround program, Project Quantum Leap, involved workforce cuts, facility consolidations, and pricing increases.

What Comes Next

Bloom guided for $3.1 billion to $3.3 billion in 2026 revenue, with non-GAAP gross margin near 32%. The operating income guidance range of $125 million to $475 million is unusually wide, signaling real execution risk even in a strong demand environment.

Plug Power must sustain and grow that 2.4% gross margin. Management targeted positive EBITDA by Q4 2026. The analyst consensus price target sits at $2.75 against a current price of $1.81.

Bloom’s valuation is rich at a forward P/E of roughly 112x, reflecting a genuine business inflection tied to AI infrastructure spending. Plug Power still carries a trailing EPS of −$2.38 and an operating margin of negative 139%. The stock has lost 96% of its value over five years. If Project Quantum Leap delivers sustained profitability through 2026, there is upside. However, that remains a significant conditional. These are two fuel cell stocks, but they no longer share a destiny.