April has brought a dense cluster of tax adjustments that businesses will feel immediately, so it’s vital that employers understand the changes and what they mean for their bottom line.

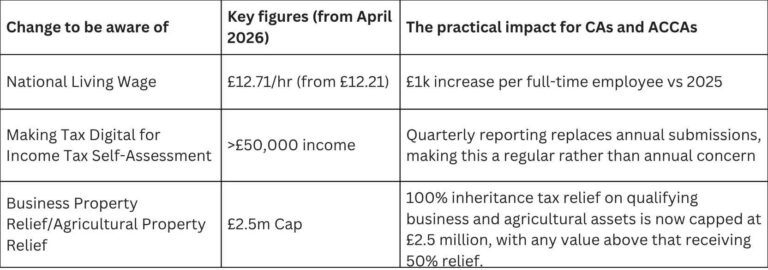

The National Living Wage (NLW) increase for workers aged 21 and over will put further financial pressure on employers, now it has risen to £12.71. The National Minimum Wage (NMW) has also increased to £8 for apprentices and under 18s, and £10.85 for workers aged 18 to 20.

At the same time as this increased cost liability, ‘Making Tax Digital’ for Income Tax is here – meaning that sole traders and landlords with a qualifying income over £50,000 must adapt their practices to fit into the new framework.

Taken together, these changes will materially increase both employment costs and the administrative burden of running a business. In effect, businesses are dealing with a compressed timeline of change, in which immediate cost pressures, new reporting requirements and longer-term planning reforms are all taking effect simultaneously.

What do rising employment costs mean in practice?

The most immediate pressure for many businesses will come from rising wage costs, which have pushed up payroll expenses across multiple sectors, particularly those that rely more heavily on lower-paid roles.

On paper, this may appear to be incremental, but in practice, the impact is much more tangible. For example, for an SME employing five full-time workers on the NLW, the change will add around £4,800 a year to the wage bill. Scaled across larger teams, that pressure quickly builds at scale – and will need to be something employers account for.

Far from a marginal adjustment, this change represents a structural shift in employment costs that businesses will need to adjust for carefully. For labour-intensive operations in particular, margins will come under increasing strain, so businesses will need to look beyond simply absorbing the additional cost.

That may involve reassessing their price points, reviewing workforce structures or tactfully examining productivity and efficiency across their entire operations. For some, this may mean making difficult decisions around recruitment or short-term investment.

The key takeaway is that these changes need to be structural and firmly embedded in business operations to be of any benefit; they cannot be a temporary, reactive measure.

Making Tax Digital: A shift in how businesses report

Alongside rising costs, many businesses will now see a considerable change in how they report their income. The introduction of Making Tax Digital for Income Tax brings with it a move towards more frequent and structured reporting – the bulk of which is entirely digitised (as the name implies).

For sole traders and landlords with a qualifying income over £50,000, this means maintaining digital records and submitting quarterly updates to HMRC, rather than relying on a single annual return. While the intention is to improve accuracy and reduce errors, the practical impact is a sharp increase in administrative responsibility and frequency.

Businesses already operating with robust systems will not necessarily feel the brunt of this transition, but those that still rely on largely manual processes will face a more significant adjustment, ensuring records are maintained consistently and responsibilities are clearly defined. It’s important to note that this is not a one-off adjustment; with the threshold set to fall further to £30,000 from April 2027, businesses and advisers should be preparing now for a multi-year transition rather than a single point of change.

Changes to BPR and APR: Planning for the longer term

While cost and compliance changes will be felt almost immediately, changes to Business Property Relief (BPR) and Agricultural Property Relief (APR) do provide a more favourable position for many business owners, while also bringing longer-term planning into sharper focus.

The threshold for 100% relief has actively increased from £1 million to £2.5 million on combined BPR and APR qualifying assets, allowing a greater proportion of qualifying business assets to be passed on without inheritance tax. For spouses and civil partners, this can extend to £5 million when these allowances are combined. Any relief above that level will apply at 50%. While the framework remains more generous than initially proposed, relief is no longer unlimited. This makes planning more important for those with significant business assets.

It is also critical to highlight that AIM-listed shares will no longer qualify for 100% relief under the revised rules. Instead, they will be capped at 50%, regardless of the £2.5 million allowance. This is likely to particularly impact wealth management firms and should be carefully considered.

For many businesses, this may reduce potential inheritance tax liability and provide greater flexibility when planning for succession. However, it does also fundamentally reinforce the importance of reviewing all your existing structures to ensure that they still operate exactly as intended under the revised limits.

Now is a sensible point to revisit succession plans to ensure that you comprehensively understand how these changes interact with the wider estate and business structure; this will help to confirm that any opportunities for relief or revisions are fully realised, while avoiding unintended outcomes.

Managing the cost of compliance

The response to these tax changes does not need to be particularly complex, but it does need to be deliberate. Now is the time to review cost structures, ensure that all compliance processes are robust and fit for purpose, and revisit longer-term plans.

Beyond the headline changes, there is also a cumulative effect to consider. Incremental increases across wages, reporting requirements and planning obligations rarely occur in isolation, and together they can create sustained pressure that quietly reshapes cash flow, decision-making and operational flexibility over time.

With the right planning, businesses can effectively mitigate rising costs with confidence, meet new compliance requirements without concern and maintain clear control over both day-to-day operations and longer-term decisions.