Looking back on oilfield services stocks’ Q4 earnings, we examine this quarter’s best and worst performers, including Atlas Energy Solutions (NYSE:AESI) and its peers.

Oilfield services companies provide equipment, technology, and services enabling exploration and production activities, including drilling, completion, well intervention, and reservoir evaluation. Their fortunes closely track upstream capital spending cycles. Tailwinds include increased drilling activity during favorable commodity environments, demand for efficiency-enhancing technologies, and growing offshore and unconventional resource development. Headwinds include significant revenue volatility tied to oil and gas price swings and producer spending discipline. Intense competition pressures pricing and margins, while the energy transition may structurally reduce long-term demand. Workforce availability and technological disruption require continuous adaptation.

The 26 oilfield services stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 3.7%.

Thankfully, share prices of the companies have been resilient as they are up 5.4% on average since the latest earnings results.

Building the world’s first long-haul proppant conveyor system to reduce truck traffic, Atlas Energy Solutions (NYSE:AESI) mines and processes sand used as proppant to prop open fractures in oil and gas wells during hydraulic fracturing.

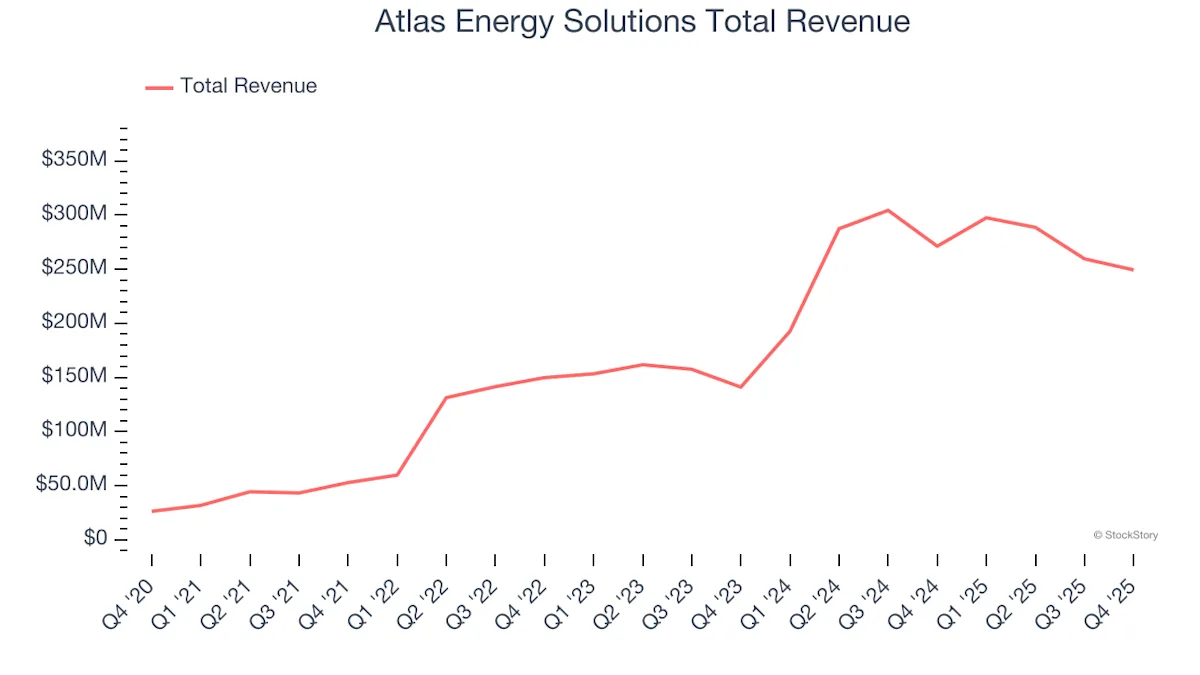

Atlas Energy Solutions reported revenues of $249.4 million, down 8.1% year on year. This print exceeded analysts’ expectations by 3.9%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ EBITDA estimates.

John Turner, President & CEO, commented, “Our fourth quarter results exceeded our initial expectations primarily driven by stronger volumes relative to what we anticipated going into the holiday season. The seasonality we typically see at the end of the year was particularly muted as customers took minimal time off around the holidays. Despite challenging market conditions, we believe the team’s commercial efforts should allow Atlas to grow volumes in 2026. Leaning on our cost-advantaged mines and logistics network, we were able to increase our share of current customers’ sand procurement spend while also adding some key new customers relationships that we expect to grow in scale over the course of 2026 and beyond.

Interestingly, the stock is up 12.1% since reporting and currently trades at $12.33.

Is now the time to buy Atlas Energy Solutions? Access our full analysis of the earnings results here, it’s free.