Matteo Colombo

Investment Update

Following my last publication on Clearway Energy Inc. (NYSE:CWEN) (NYSE:CWEN.A) in May, the stock is +5% and the business has posted its Q2 numbers, which I’ll dissect here today. In the prior report, titled “Turnover on capital unable to pick up exceptional operating margins“, I performed an extensive deep dive into the company, its business drivers, how it is unlocking value, its CapEx runway, returns on capital, prospects of underlying asset recovery, and valuation. At the time, my view was the business was worth ~$23/share.

Key points to the investment debate, which remain relevant to this day (and thus must be reinforced) include the following:

- The energy transition could see differentiated utilities businesses as beneficiaries of investment into global energy infrastructure initiatives. Two problems exist – redundant infrastructure + grid congestion. Renewables can either exacerbate or alleviate this problem – we won’t know until sometime.

- Until then, there are critical metals shortages to consider (in particular, copper).

- CWEN presents as a potentially unique play in the renewable energy value chain being that it is a renewable energy investment company. It’s worth noting the business is sponsored by two separate entities, GIP and TotalEnergies, respectively.

- This is a capital-intensive business whereby to produce $1 of sales from FY’21 to Q1 FY’24 required ~$78 and this squares off with the economics of the business where upfront capital costs are high with accelerated depreciation schedules that require mammoth CapEx to maintain their operative standing. As such, whilst margins are exquisitely high for the business, capital turnover is not – a hallmark of what I’d like to see in a business requiring large sums of cash reinvestment.

Management has a new goal of a “path to $2.15 of cash available for distribution (“CAFD”) per share” (equal ~$435mm grossed up) which is notable but my view is the intrinsic worth of the business is roughly ~$23/share today given what’s required to sustain its operations, let alone grow. Net-net, reiterate hold.

Figure 1. CWEN 12-month price evolution ($28.15 at the time of publication).

Seeking Alpha

Q2 FY’24 earnings insights

CWEN put up $336mm of quarterly revenues on adj. EBITDA of $353mm in Q2. On its quest to ~$435mm pro forma CAFD, it printed $187mm during the quarter bringing the YTD CAFD to $239mm (~53% fulfilled). This new estimate comes as management recycled proceeds from the thermal business divestment, providing a broader capital base + longer runway for earnings.

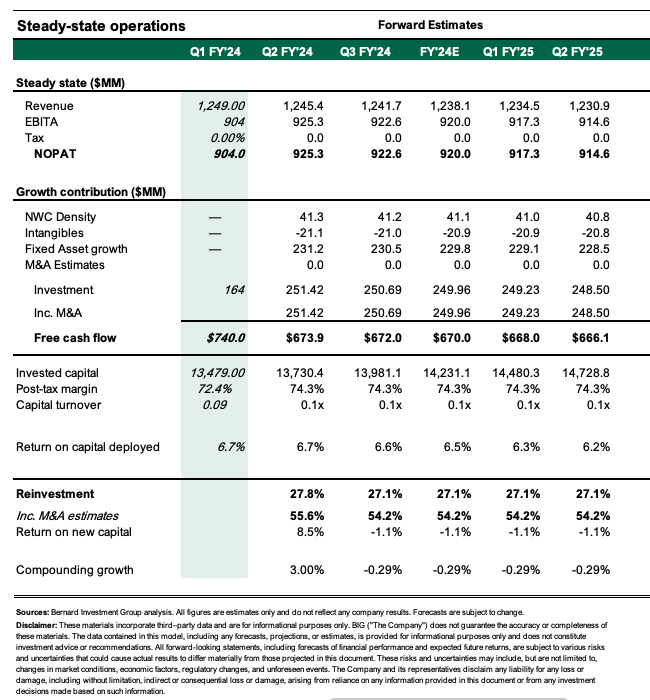

Whilst I’m acutely aware of the capital costs in the industry (notwithstanding current borrowing costs on debt) management says it can fund this growth route internally, according to management: “To fund these offers, we expect to be able to utilize retained CAFD as well as excess corporate debt capacity. Our revolving credit facility remains a key source of liquidity…to support various collateral requirements up to $200mm”. This is notable and I’d be benchmarking the company against this each quarter going forward. More so given the cyclicality of earnings produced on the capital base (Figure 2).

Figure 2.

Company filings, author

Critically, management views the following steps as “building blocks” to hit the CAFD targets:

- ~$240mm of capital funded via existing liquidity to bring CAFD >$2.15/share;

- Investments are made at “CAFD yields that would make investments accretive at [its] present cost of capital”;

- Higher gas fleet revenues from pricing advantages embedded in its 2026/’27 contracts is set to be another key lever, driving ~5-8% growth in CAFD.

Again, I’d urge investors to benchmark management against these assumptions moving forward.

Strategic investments during the quarter:

-

Luna Valley and Daggett I Projects: Committed ~$143mm to these projects expected to yield a 10% CAFD + grants CWEN ownership of 100% of the cash equity interest in each. On the upside, it initially expected 50%. These projects are backed by LT contracts with investment-grade entities adding to FCF predictability.

-

Pine Forest Solar Plus Storage Complex: It received an offer to invest in the Pine Forest Solar Plus Storage complex in Texas. This project includes 300Mw of fully contracted solar generation + 200Mw of battery capacity. It will be used to complement solar revenues. CWEN will accelerate the depreciation on these assets creating tax advantages with the charge against earnings. Management projects ~10.5% CAFD yield on the ~$155mm capital outlay.

-

Honeycomb Battery Hybridization Program: Management expects potential investment commitments for this program by yearend.

My view of the company’s quarter was that it was largely in line with expectations, however, the revised deal at the Luna Valley project was an upside surprise, along with the revised CAFD targets. The question is now on management on how it will execute this plan moving forward. These are notably ambitious targets that could catch the attention of investors chasing yield or income growth in the current climate.

My concern is that investors are unlikely to pay higher multiples for a renewable energy company that is set to grow distributions rather than retaining and reinvesting cash flows for surplus earnings power. The business trades around par to invested capital, as discussed later, as it is not earning rates on this capital above what investors could reasonably expect to achieve elsewhere in this industry – albeit with higher quality offerings and higher distributions. Consequently, the execution risk is high and we should get a risk premium or embedded discount to accommodate for this. I do not see evidence for this at the current Market pricing as discussed, below.

Fairly valued with risk/reward calculus balanced

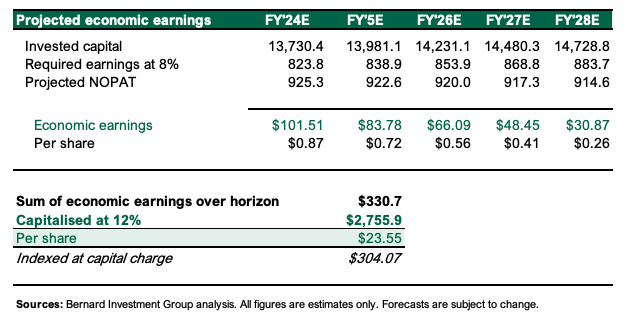

Based on 1) management’s + my own revised targets [see: Appendix 1], 2) its renewed investment capacity, and 3) its steady state of operations, my view is the business is worth ~$23/share today, in line with previous estimates. This is critical, as numerous updates to my modelling have been baked in, yet no change to the discounted value of cash that could be stripped out by a private owner over above a comparable rate in the coming years is produced.

- Aggressive forward assumptions are needed to meaningfully deviate from this estimate, namely 1) sales growth +6%, 2) 80% pre-tax margins, and 3) 12% ROICs. We’d also need investors to pay a high multiple of this estimate of discounted cash flow (which is completed with a 12% hurdle rate). The business also trades ~1x EV/IC which squares off – a business earning ~cost of capital shouldn’t trade at a premium.

Figure 3.

Author’s estimates

- I mentioned this last time in the recovery of our underlying asset value seems impaired under CWEN’s present economics – my view is here opportunity cost of owning the company vs. more selective opportunities will result in an improper recovery of our underlying, including capital and return on capital. I’m not sure $1 of CWEN’s incremental capital will be valued >$1 by the market under these assumptions. This supports a reiterated hold rating.

Figure 4.

Author

Risks to investment thesis

Upside risks to the thesis include 1) management growing pre-tax margins >75%, 2) FCFs >$500mm with reinvestment >50% (as this sees the valuation climb higher, but this is a huge ask from management), and 3) a change in rates which could be a tailwind for equity valuations.

On the downside, the risk is further compression of ROICs, and a pullback in operating margin below industry peers. This substantially reduces implied valuations and could see the business trade <1x EV/IC.

Investors should know these risks in full before proceeding any further.

In short

CWEN remains a hold in at this point in the cycle as 1) capital requirements to grow the business are tremendously high at 1x EV/IC as 2) earnings produced on operating capital are low due to their inefficiency, and 3) valuations support ~$23 per share, implying it could pull back to this range. Management has bold ambitions for cash distributions to shareholders and this may fulfil a certain investment profile, just not ours at this point. I look forward to providing ongoing coverage.

Appendix 1.

Author